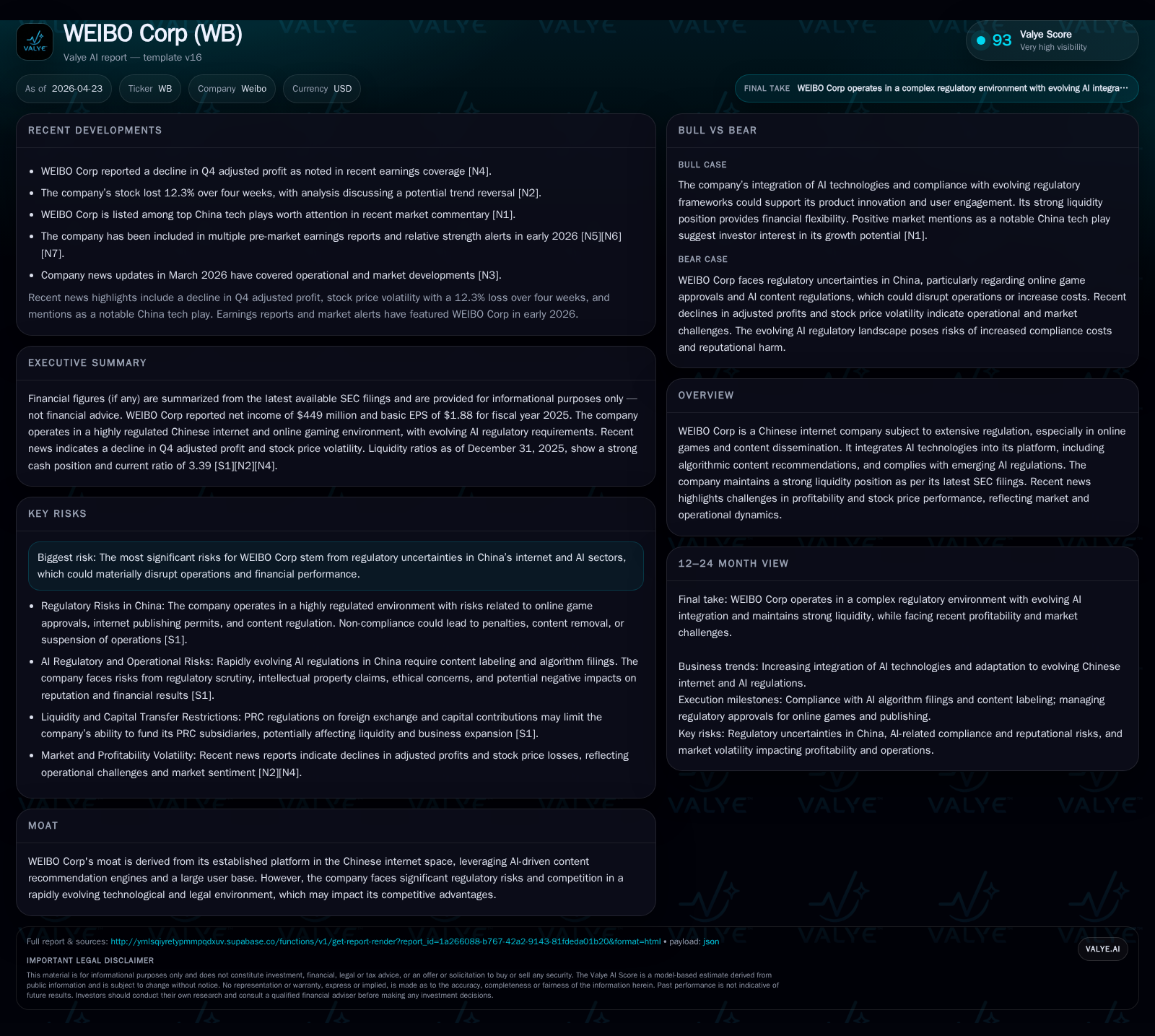

WEIBO Corp Leverages AI Integration Amid Regulatory Challenges and User Engagement Shift

Latest filings reveal stable yet filtered user growth alongside sustained AI-powered monetization amidst complex regulatory environment.

WEIBO Corp's most recent annual and quarterly filings underscore its strategy of enhancing user quality over volume, stabilizing engagement metrics while deploying AI-driven content recommendation to sustain advertising revenue streams. The company operates under heightened regulatory scrutiny particularly around online games and content dissemination, adding complexity to its growth trajectory. Despite these headwinds, WEIBO maintains a strong liquidity position supported by robust operating cash flow and conservative capital management, positioning it for measured expansion in China’s evolving social media landscape.

Recent Operating Update

WEIBO Corp filed its latest Form 20-F and complementary 6-K updates in April 2026 covering fiscal year ending December 31, 2025 [S1][S2][S3]. The filings disclose a deliberate focus shift to cultivating a higher quality user base instead of maximizing gross user counts. Monthly active users (MAUs) decreased slightly from 590 million at the end of 2024 to 567 million at the end of 2025. Concurrently, daily active users (DAUs) fell moderately from 260 million to 252 million [S1]. Importantly, the ratio of DAUs to MAUs stabilized near 45%, signaling consistent engagement levels among remaining users.

The company's revenue generation remains heavily skewed toward advertising and marketing services leveraging the Weibo platform's extensive reach [S1]. This is supported by continual refinement of an interest-based AI recommendation engine that enables precise targeting based on user demographics, interests, and social connections. Though WEIBO's overall MAU count shows modest contraction, these high-intent users are likely more valuable advertisers’ targets [S1][S16].

From a financial perspective, the company reports net income of $449 million in FY2025 with operating income standing at approximately $465 million. Operating cash flow remains strong at $519 million against capital expenditures around $42 million—highlighting solid free cash flow generation sufficient to support operational needs, acquisitions, and shareholder returns [F1].

Business Model

WEIBO Corp monetizes through two principal channels: advertising and marketing services forming the majority of revenue, complemented by value-added services such as memberships and game-related offerings. Advertising products include social display ads and promoted feeds sold directly or through agencies, designed with advanced targeting capabilities powered by AI algorithms [S1][S5].

Crucial to this ecosystem are the platform partners comprising influencers (key opinion leaders), media outlets with rights content, multi-channel networks managing influencer portfolios, self-media entities, and app developers. This partner network contributes significant volumes of original content that enhance user engagement via virality mechanisms intrinsic to Weibo's microblogging model [S16][S21]. There exist revenue-sharing arrangements with certain partners involved in live streaming and gaming sectors.

The hybrid platform integrates multiple content formats — textual posts, photos, videos including short formats, live streams, and audio — responding to evolving media consumption trends. Investments in cloud infrastructure enable rapid scalability during peak events, maintaining a smooth user experience even under viral load spikes [S10][S22]. The introduction of machine learning models facilitates semantic understanding of video content for efficient distribution and review.

Strategically, WEIBO pursues refined advertising load management balancing monetization efficacy against potential user experience fatigue. It continuously innovates ad product formats intended to address brand awareness as well as direct conversion campaign needs [S21]. Membership upgrades and interactive entertainment apps augment monetization diversity.

Industry Structure and Competitive Position

WEIBO operates in China's highly competitive social media segment where market share battles center not only on attracting large user bases but also on depth of engagement and advertiser relevance [S6]. Major competitors include other social networking platforms offering comprehensive digital ecosystems combining e-commerce, messaging, multimedia content creation/distribution plus O2O solutions tailored for specific verticals.

Regulatory oversight intensifies complexity: licensing requirements for online games managed on the platform mandate National Press approvals; failure risks suspension or penalties. Also impending internet publishing permits loom—draft regulations prescribe mandatory licensing before engaging in game publication or virtual currency transactions within the ecosystem [S15].

Additionally, China’s evolving AI regulatory landscape imposes compliance burdens relating to algorithmic transparency and content governance—a sector-wide challenge. WEIBO integrates AI extensively into its recommendation engines but faces risk exposure if future regulations restrict algorithmic operations or require costly adaptations [S15].

Despite this environment, WEIBO’s moat lies in its established brand recognition within China’s internet ecosystem fostered by a vast content creator network combined with advanced technological infrastructure optimizing viral distribution and ad targeting . Its strategic alliance with SINA enhances sales capabilities though larger tech conglomerates offer broader cross-platform synergy threatening wallet share.

Growth Drivers and Constraints

Growth is driven structurally by China’s continued digital transformation wherein social media engrains deeper into daily life. Video adoption accelerates as multi-format consumption preferences increase user time spent on platforms favoring interactive and immersive experiences. WEIBO’s investments in video encoding innovations and live streaming technology respond directly to this trend [S10][S22].

AI advancements present incremental opportunities for granular customer insights enabling precision marketing which could command premium CPMs (cost per mille). Expansion of value-added services including membership tiers or gaming partnerships offer ancillary revenue streams reducing sole dependence on advertising cycles.

Conversely, growth constraints include regulatory uncertainties particularly around online games approval processes where delays or denials limit offering scope. Monetization depends critically on maintaining an attractive ecosystem for content creators; dissatisfaction over monetization terms could lead creators migrating away reducing content richness impacting user engagement negatively [S16][S21]. Furthermore, competition from global platforms introducing localized strategies adds pressure requiring constant innovation.

Economic cyclicality impacts advertising budgets although modest diversification towards SMEs may buffer downturn effects since smaller advertisers often maintain digital presence for cost-efficiency.

What to Watch Next

Key operational milestones include monitoring expansion or contraction trends in daily active users alongside engagement ratios as early indicators of community health post-regulatory adaptation. Performance evolution of new advertisement formats especially those leveraging AI capabilities will provide insight into monetization trajectory.

Regulatory developments concerning official adoption of revised gaming laws or internet publishing permits remain critical catalysts potentially altering compliance costs or business scope.

Capital allocation moves such as execution pace of authorized $200 million share repurchase plan (initiated late 2025) signal management priorities toward shareholder returns versus reinvestment strategies [S13][S17].

Finally, technological enhancements particularly in video/live streaming quality metrics are pivotal due to their direct influence on user retention amid shifting consumption patterns.

Financial Profile

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 449 | 519 | 465 | 42 | +49.3% |

| 2024 | 301 | 640 | 494 | 61 | -12.2% |

| 2023 | 343 | 673 | 473 | 37 | +300.4% |

| 2022 | 86 | 564 | 480 | 43 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 477 | ||

| 2024 | 194 | 58 | 578 |

| 2023 | 200 | 58 | 636 |

| 2022 | 58 | 521 |

Source: SEC companyfacts cache [F1].

WEIBO exhibits a robust financial foundation backed by diversified revenue from advertising (approximate steady revenue near historically reported USD ~1.75 billion range per year across recent periods) supported by refined offering mix centered on quality audience targeting rather than sheer scale expansion [F1],[S1].

Net income improved sharply from $301 million in FY2024 to $449 million in FY2025 reflecting operational efficiencies or potential lower expenses on scaling efforts despite slight top-line stability [F1]. Operating income showed mild contraction year-over-year (-6%) yet stays strong near $465 million level.

Operating cash flows remain healthy though reduced approximately 19% YoY at $519 million partly due to fluctuating working capital changes while capex declined around 31% YOY consistent with platform maturation stage [F1]. Capital expenditures focused on upgrading server infrastructure supporting cloud scalability for dynamic content delivery.

Liquidity is ample with current assets outstripping liabilities more than threefold (current ratio ~3.4), facilitating ambitious purchase commitments including ~$612 million earmarked largely for marketing campaigns supporting demand stimulation [F1],[S8],[S14].

Debt structure includes long-term notes maturing mid-to-late decade bearing moderate fixed/variable rates; no significant covenant restrictions are indicated implying operational flexibility with planned refinancings deferred beyond near term [F1],[S4],[S7],[S18],[S24]. Dividends remain an active part of capital return policy complemented by authorized but not yet deployed share repurchase program.

Disclaimer

This analysis is provided solely for informational purposes drawn strictly from disclosed regulatory filings and related public data without any investment recommendation or price forecast. Investors should consider all risks detailed herein along with their own research before considering any involvement with WEIBO Corp securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments