WEX Inc. Sustains Growth Momentum While Adjusting Capital Allocation in Q1 2026

WEX demonstrates steady revenue growth and operational stability in Q1 2026 as it navigates the expiration of its share repurchase program and manages significant leverage.

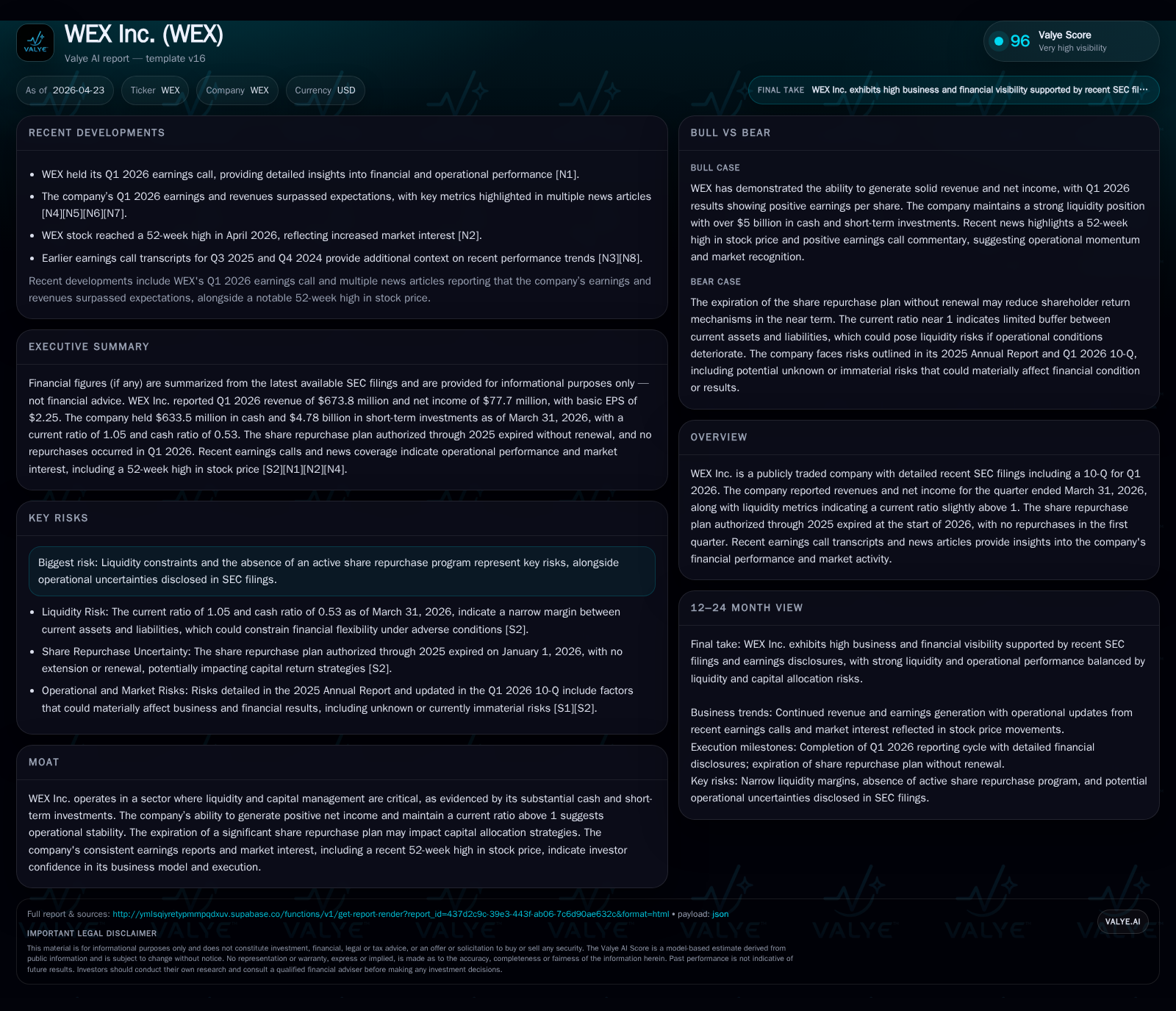

In Q1 2026, WEX Inc. maintained modest revenue growth with a top-line increase of approximately 1.2% year-over-year annualized, alongside stable net income metrics. The quarter was marked by the expiration of its $2.05 billion share repurchase plan, leading to no buybacks during the period and signaling a shift in capital allocation strategy. Despite considerable net debt exceeding $3 billion, WEX’s current ratio slightly above 1 underscores balanced short-term liquidity. The company’s embedded payment processing platform and suite of finance-related services reinforce recurring customer engagement amid competitive fintech dynamics.

Q1 2026 Operating Update and Its Strategic Implications

WEX Inc.’s first quarter ending March 31, 2026, detailed in its latest 10-Q filing [S2], reflects a company sustaining steady revenue growth amid evolving capital strategies. Revenues continued to inch upward at an annualized pace approximating +1.2% year-over-year based on trailing twelve-month comparisons from fiscal year-end data [F1]. The net income performance remained relatively stable compared to prior periods though operating income registered a modest decline.

Liquidity stood on solid footing with current assets tallying approximately $10.7 billion against nearly $10.2 billion in current liabilities for a current ratio around 1.05 [F1]. This marginally above one ratio signals a balanced short-term liquidity position, critical given WEX’s sizable gross debt burden exceeding $3.6 billion and net debt nearing $3.06 billion after offsetting cash reserves [F1]. Significantly, the company’s sizable cash & equivalents balance of $633 million at quarter-end provides near-term operational flexibility.

A pivotal recent development is the expiration of WEX’s previously authorized $2.05 billion share repurchase program as of December 31, 2025 [S2][S4]. No common stock buybacks were executed during Q1 2026 following the cessation of this program—a material shift that recalibrates how excess capital will be allocated going forward. This absence removes one traditional mechanism for shareholder return enhancement but may redirect funds toward reinvestment or debt management.

Additionally, during Q1 2026 no new Rule 10b5-1 insider trading arrangements were adopted or modified among senior executives aside from a limited arrangement by the COO intended for modest sales scheduled later in the year [S2]. Together these details portray WEX as maintaining operational stability while strategically adjusting its approach to capital stewardship.

Understanding WEX’s Business Model and Core Offerings

WEX generates revenue via a multi-segment model primarily composed of payment processing fees, account servicing fees, finance fee income, and other ancillary services as described in its latest annual report [S1]. Payment processing remains the cornerstone segment where fees accrue from facilitating transactional flows across corporate clients’ fuel cards, expense management solutions, virtual payments, and fleet management offerings.

Account servicing fees arise largely from ongoing administration of existing contract relationships encompassing card program management and customer support functions—these create recurring revenue streams supported by strong switching costs inherent in customized platform integrations and data analytics capabilities.

Finance fee revenues are tied to financing activities around purchase volumes facilitated through credit extensions or installment payment plans linked to client usage patterns [S1]. This blend allows WEX to capture diverse value pools from transaction volume acceleration to interest income.

Underlying these revenue components is an investment in digital infrastructure enabling real-time transaction processing with embedded compliance and risk controls essential given the complex regulatory environment governing payments globally. Such technological sophistication supports customer retention via differentiated experience and value-added analytics.

Competitive Dynamics and Industry Positioning

Within the fintech payments ecosystem, WEX occupies a vital niche providing B2B payment solution infrastructure tailored chiefly toward fleet management, travel & corporate expense sectors [S1][N12]. Competition arises from both legacy financial institutions offering commercial card products and emerging fintech players innovating via API-centric platforms with enhanced data integration capabilities.

WEX’s strategic moat crystallizes around network effects: its platforms gain incremental value as client adoption scales transaction volumes generating deeper data insights—thus raising switching costs for customers due to integration complexity and the proprietary nature of spend management tools deployed [N12]. Pricing power manifests modestly since contract terms typically involve negotiated fee structures balancing market competitiveness with service differentiation.

Regulatory compliance emerges as both a barrier to entry and an ongoing cost center; operating globally obliges adherence to multiple jurisdictional mandates affecting payments settlement times, anti-fraud protocols, data privacy laws (e.g., GDPR), and AML requirements [S1]. Continuous platform modernization is requisite not only for compliance but also for countering headwinds posed by merchant acceptance challenges and evolving buyer preferences driven by mobile payments innovation.

Key Drivers Catalyzing Growth and Potential Constraints

Growth catalysts for WEX stem from steady expansion initiatives into adjacent verticals such as healthcare payments automation and cross-border virtual card offerings highlighted in recent earnings commentary [N1]. Incremental revenue uplift can be triggered by increasing penetration rates within existing clients’ spend categories bolstered through enhanced analytics-led product upsell strategies.

New product rollouts including AI-driven fraud detection modules or integrated invoicing solutions represent further upside paths enabling margin improvement through scale economies on fixed platform investments [N1][S2]. Demand drivers also reflect structural trends toward digital transformation among enterprise customers seeking cost-efficient cash flow optimizations amid macroeconomic uncertainty.

On the flip side growth constraints entail deleveraging pressure given net debt exceeding $3 billion potentially impeding aggressive reinvestment or shareholder return scaling absent refinancing actions [F1]. Additionally, inflationary impacts on staffing or technology costs could compress margins over time if pricing adjustments do not fully offset expense inflation [S6][S7]. Regulatory shifts imposing tighter controls on commercial card usage or credit extensions could also crimp allowable product scope without adaptation.

Collectively these dynamics suggest that while demand exhibits structural characteristics favoring ongoing platform utilization growth, margin progression may face cyclical noise factors tied closely to capital availability and regulatory environments.

Capital Allocation Evolution: Share Repurchases and Liquidity Status

The expiration without renewal of the $2.05 billion share repurchase plan at end-2025 marks a watershed moment in WEX’s capital deployment philosophy [S4]. During Q1 2026 no buyback activity was undertaken highlighting an inflection point possibly signaling a strategic pause pending assessment of broader operational priorities or external market conditions.

Despite this pause in repurchases, WEX holds substantial liquidity reflected by cash & equivalents of roughly $633 million alongside current assets near $10.7 billion against $10.2 billion in current liabilities yielding a current ratio of about 1.05—a tight but adequate buffer demonstrating careful liquidity stewardship [F1]. This indebtedness level contextualizes decisions surrounding dividend policies or potential renewed capital returns post-expiration window; management has not signaled imminent reauthorization plans but this remains an area warranting scrutiny given investor appetite for returns versus funding reinvestments or deleveraging ambitions [S4][S13].

Upcoming Catalysts and Monitoring Points

Attention ought to focus on upcoming quarterly earnings releases where updated guidance figures or segment-specific throughput metrics reveal whether growth momentum materializes beyond modest Q1 gains [N1][S2]. Monitoring key client segment expansions—especially in newly targeted verticals like healthcare—or new product adoption rates could affirm sustainable trajectory shifts.

Regulatory developments impacting cross-border transactions or credit underwriting standards must also be tracked closely given their potential impact on margins or addressable market size [S7]. Additionally insider Rule 10b5-1 trading arrangements adopted indicate executive confidence timing but should be viewed alongside broader macroeconomic conditions potentially influencing strategic recalibration [S2].

Finally any announcements concerning refinancing activity or renewed capital return plans will materially influence perceptions around financial flexibility.

Financial Overview Supporting Operational Analysis

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 2.7 | 304 | 454 | 664 | +1.2% | -1.8% |

| 2024 | 2.6 | 310 | 481 | 686 | +3.1% | +16.1% |

| 2023 | 2.5 | 267 | 908 | 647 | +8.4% | +59.5% |

| 2022 | 2.4 | 167 | 679 | 470 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 800 | 314 | 24.6 |

| 2024 | 652 | 334 | 20.8 |

| 2023 | 303 | 764 | 14.6 |

| 2022 | 283 | 567 | 10.1 |

Source: SEC companyfacts cache [F1]. | The fiscal year ended December 31, 2025 figures taken from annual filings [F1] reinforce the narrative seen in quarterly snapshots: revenue growth remains positive albeit decelerated; operating income slipped somewhat likely due to expense pressures; net income followed suit but remains near prior levels evidencing operational resilience.

These financial contours provide quantitative backing for qualitative observations regarding business steadiness amidst strategic transition points highlighted earlier.

This analysis synthesizes publicly available SEC filings including the recent Q1 2026 Form 10-Q alongside associated event disclosures plus financial databook snapshots without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments