WTW’s 2025 Earnings Rebound Driven by Acquisition and AI-Driven Solutions Amid Risk Challenges

Willis Towers Watson PLC posted a strong turnaround in 2025 revenue and profitability, boosted by its Newfront acquisition and technology innovation.

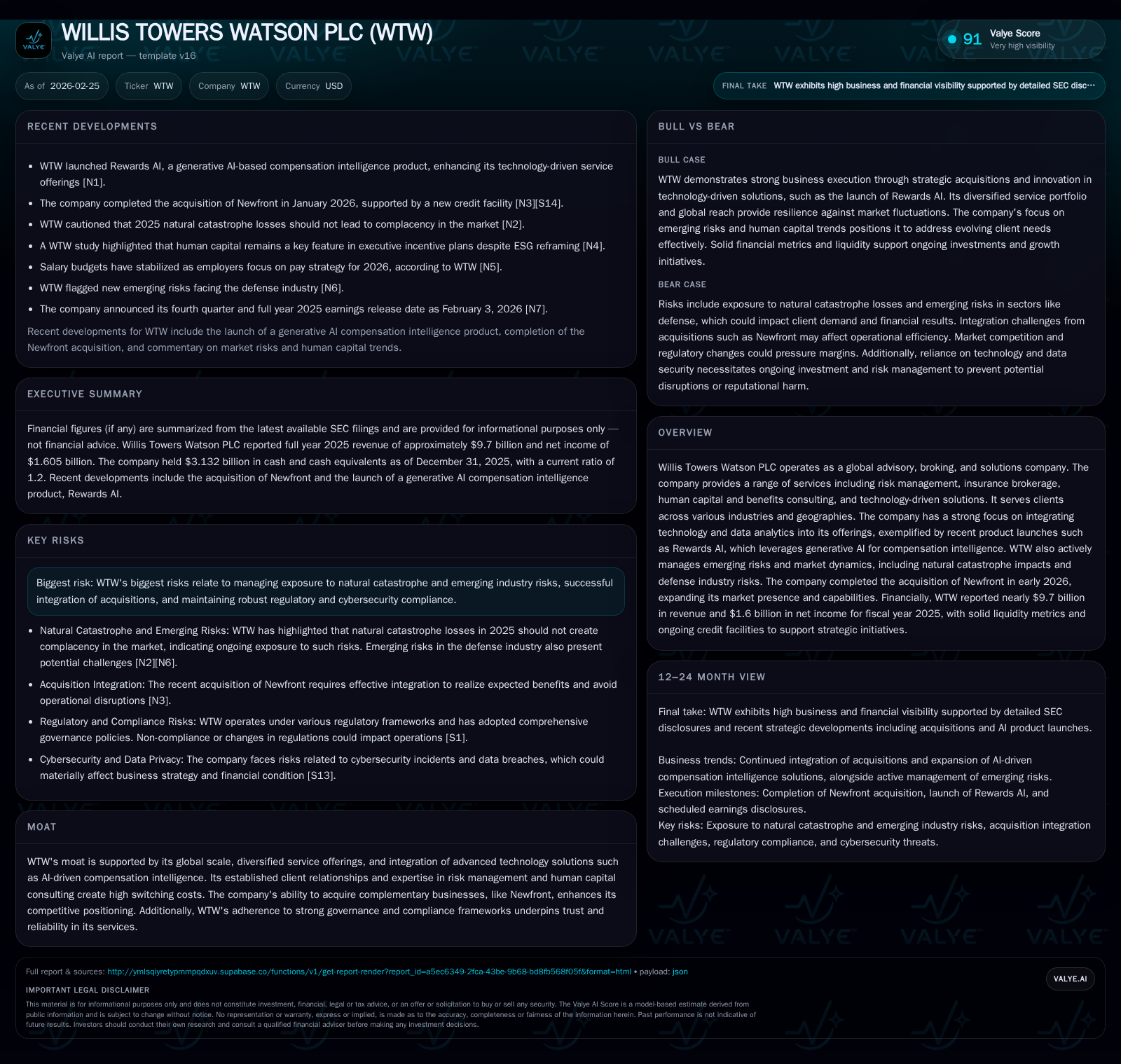

WTW reversed its 2024 net loss to report $1.6 billion net income in 2025, supported by solid operational execution and the January 2026 acquisition of Newfront expanding its brokerage footprint. Revenue approached $9.7 billion but declined slightly amid market dynamics. The launch of Rewards AI marks a notable push into AI-powered compensation solutions, reinforcing WTW’s tech integration strategy. Risks persist around natural catastrophe exposures, defense industry threats, and cybersecurity compliance. Capital returns accelerated with buybacks rising to $1.65 billion, while dividends remained steady.

Overview

Willis Towers Watson PLC (WTW) operates globally as an advisory, broking, and human capital solutions firm serving diverse industries across geographies. Its portfolio spans risk management, insurance brokerage, human capital consulting, and increasingly technology-driven products that embed data analytics and AI capabilities. In fiscal year (FY) 2025, WTW reported just under $9.7 billion in revenue alongside a substantial rebound in operating profits and net income [F1]. The company also consummated the acquisition of Newfront Insurance Holdings early in January 2026 [N2], expanding its market presence particularly in U.S.-based insurance brokerage.

The firm's strategic orientation towards integrating advanced technology is underscored by the February launch of its Rewards AI platform—a generative AI solution designed for compensation intelligence—reflecting a broader sector-wide trend towards embedding artificial intelligence for enhanced client outcomes [N3]. Concurrently, WTW continues vigilant risk monitoring around natural catastrophe impacts [N4] and emerging risks specific to the defense sector [N7], reflective of the increasingly complex operating environment.

Historical Performance

WTW’s financial trajectory over recent years illustrates resilience punctuated by transformative acquisitions and strategic pivots:

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 9.7 | 1605 | 1775 | 2.2 | -2.2% | +1737.8% |

| 2024 | 9.9 | -98 | 1512 | 0.6 | ||

| 2021 | 9.5 | 1055 | 1345 | 1.4 | +1.4% | +5.9% |

| 2020 | 9.4 | 996 | 1774 | 1.2 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 358 | 1650 | 20.1 |

| 2024 | 354 | 901 | -1.2 |

| 2021 | 352 | 1000 | 11.1 |

| 2020 | 346 | 0 | 9.2 |

Source: SEC companyfacts cache [F1].

The substantial increase in operating income and net income for FY25 follows prior years' challenges including a net loss in FY24 [F1]. The improvement reflects effective cost management, operational leverage, and contributions from acquisitions such as Newfront [S3]. While revenue dipped slightly due to market conditions impacting client budgets [N6], WTW's profitability margins expanded meaningfully.

Growth Prospects

WTW’s forward growth is shaped by multiple vectors:

- Acquisitions: The Newfront deal completed late January offers expanded cross-selling opportunities leveraging WTW’s global platform alongside Newfront’s digital-first broking model [N2].

- Technology Innovation: Launches such as Rewards AI embody WTW’s push into analytics-driven HR consulting segments which are gaining momentum amid corporate workforce transformation [N3][N5].

- Market Dynamics: Stabilizing salary budgets combined with ESG reshaping executive incentives signal evolving client priorities where WTW’s advisory expertise can add differentiated value [N5][N6].

Challenges include competitive pressures among advisory firms investing similarly into AI tools, regulatory changes affecting insurance placements, and economic uncertainties that may constrain consulting spend.

Forecasts & Milestones

While explicit forward guidance is not publicly disclosed, key milestones include:

- Integration of Newfront with targeted cost synergies realization within the next fiscal year.

- Expansion of Rewards AI capabilities beyond initial markets.

- Continued monitoring of natural catastrophe risk modeling given potential volatility. Quarterly performance updates will be critical for assessing margin progression post-acquisition and client retention trends.

Return on Equity & Capital Allocation

WTW demonstrated an approximate return on equity (ROE) of about 20% for FY25 based on net income of $1.605 billion against equity of approximately $7.976 billion at year-end [F1]. This indicates effective capital utilization amid ongoing integration expenses.

Capital allocation priorities include:

- Dividends: Stable payments around $358 million annually maintain shareholder income consistency [F1].

- Share Repurchases: A marked increase to $1.65 billion in buybacks during FY25 underscores confidence in cash flow generation and supports share price [F1][S29].

- Cash Flow & Liquidity: Operating cash flow reached $1.78 billion supporting an estimated free cash flow near $1.63 billion after capital expenditures; liquidity remains strong with over $3 billion cash equivalents complemented by access to a $775 million delayed draw term loan facility linked to acquisitions [F1][S4][S6][S7].

Industry & Risk Considerations

Key risks include:

- Natural Catastrophe Exposure: Despite relatively benign losses in the latest period [N4], volatility remains a concern impacting demand for risk transfer solutions.

- Cybersecurity: Ongoing cyber threats require rigorous controls; WTW has implemented mandatory training and third-party risk management though residual risks remain [S11].

- Regulatory Compliance: Multi-jurisdictional operations face evolving regulatory frameworks including ESG-related executive compensation reforms [N5][S5].

- Acquisition Integration: Effective assimilation of Newfront is essential to avoid operational disruption.

- Emerging Risks: Defense industry exposures require adaptive risk strategies given geopolitical shifts [N7].

Conclusion

Willis Towers Watson’s fiscal year 2025 performance reflects strategic resilience through operational improvements and acquisitive growth supported by robust capital deployment policies. Its investment in AI-driven solutions like Rewards AI positions it well within evolving advisory landscapes while maintaining vigilance over significant risk factors ranging from natural catastrophes to cybersecurity challenges.

Execution on acquisition integration and technology adoption will be key determinants shaping medium-term outlook.

This analysis does not constitute investment advice or recommendations but aims to provide detailed insight into Willis Towers Watson PLC’s recent performance and strategic context based on publicly available information.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments