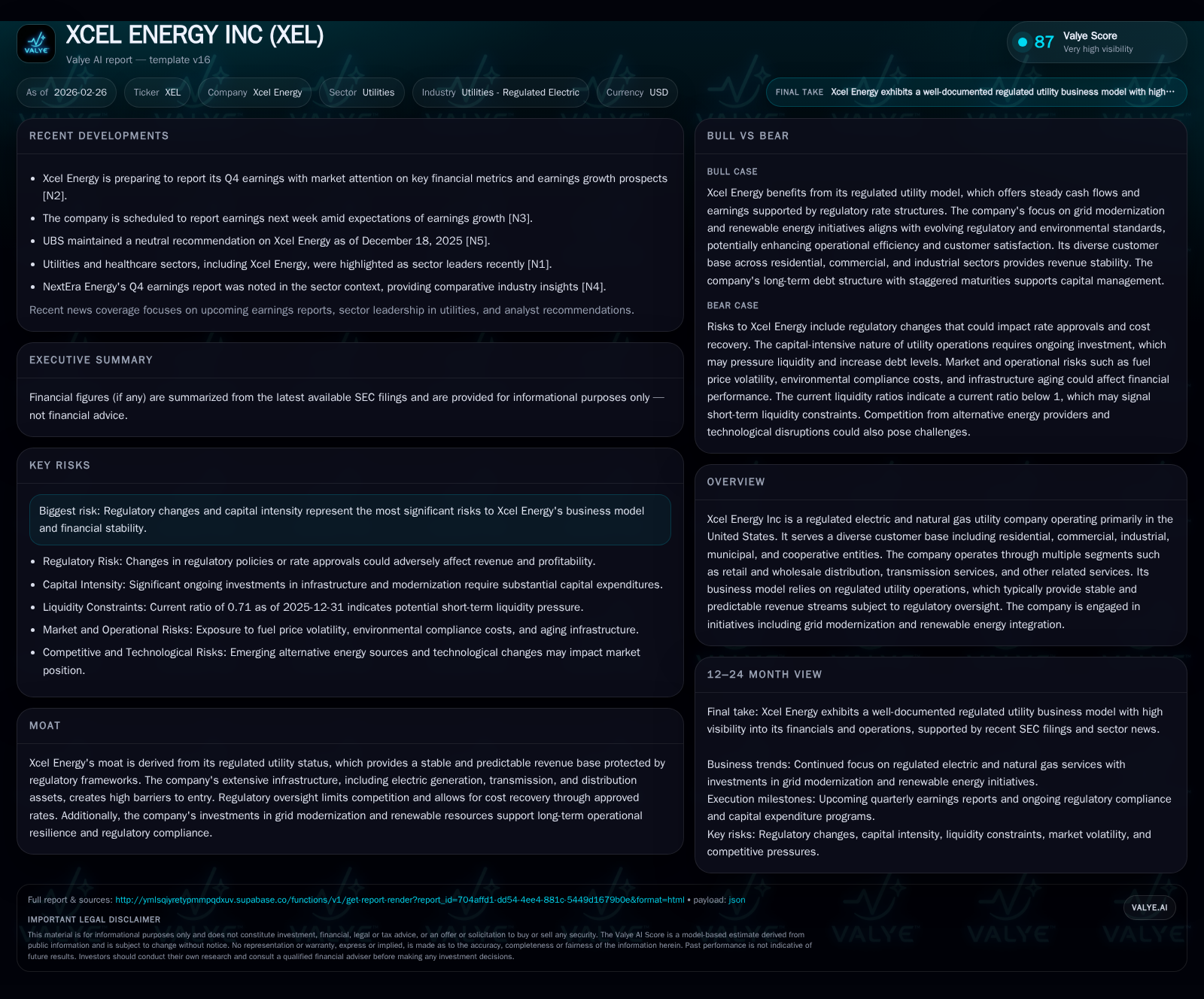

Xcel Energy's Earnings Momentum and Capital Strategy in 2025

Examining Xcel Energy's steady earnings growth alongside its capital allocation amidst rising regulatory and modernization demands.

Xcel Energy delivered solid financial results in 2025, supported by an 8.3% operating income increase and consistent net income growth, highlighting the stability of its regulated utility model. Despite a 12% decline in operating cash flow, the company maintained robust capital investments primarily in grid modernization and renewable integration efforts. Regulatory frameworks continue to underpin its earnings visibility, while capital intensity and evolving rate cases present ongoing challenges. Xcel’s capital allocation balances dividend growth with infrastructure spending within a tight liquidity profile.

Historical Performance: Revenue and Income Trajectory Highlight Stability

Over the past four years, Xcel Energy has demonstrated consistent growth in revenue and profitability metrics emblematic of its regulated electric utility standing. Revenues rose modestly by around 3% year over year, culminating at approximately $30.1 billion by the end of 2025 [F1]. Operating income exhibited a sturdier increase of 8.3% to $2.58 billion in FY2025, aided by efficient cost management within largely rate-regulated environments that cap margin volatility [F1]. Correspondingly, net income expanded by over 4%, reaching roughly $2.02 billion last fiscal year [F1]. This progression underscores the company's capacity to steadily grow earnings even within mature markets.

Historical performance (annual)

| FY | Net ($bn) | CFO ($bn) | OpInc ($bn) | Net YoY |

|---|---|---|---|---|

| 2025 | 2.0 | 4.1 | 2.6 | +4.2% |

| 2024 | 1.9 | 4.6 | 2.4 | +9.3% |

| 2023 | 1.8 | 5.3 | 2.5 | +2.0% |

| 2022 | 1.7 | 3.9 | 2.4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 1282 | 8.5 |

| 2024 | 1175 | 9.9 |

| 2023 | 1092 | 10.1 |

| 2022 | 1012 | 10.4 |

Source: SEC companyfacts cache [F1].

Revenue growth calculated between latest available years; operating income and net income exhibit continuous upward trends [F1].

Shifts in Operating Metrics: Understanding Recent Earnings Dynamics

While Xcel’s earnings on an accounting basis have advanced solidly through 2025, operating cash flow (CFO) tells a nuanced story influenced by working capital fluctuations and seasonal factors typical of utilities with regulated receivables and payables cycles [N1][N2][F1]. CFO declined by approximately 12% after peaking the prior year, reflecting higher infrastructure spending cycles and timing differences on customer billing normalization [F1][N1]. The disparity between operating income gains and cash flow contractions exemplifies the challenge of managing liquidity in capital-heavy sectors where AFUDC (allowance for funds used during construction) deferrals impact interim cash generation.

Segment Composition and Geographic Footprint: Regulated Electric Backbone

Xcel’s operations span regulated electric and natural gas distribution predominantly via subsidiaries like Northern States Power (Minnesota/Wisconsin), Public Service Company of Colorado, Southwestern Public Service Company, among others detailed in filings [S4][S6]. The bulk of revenue arises from retail distribution to residential, commercial, industrial, municipal, and cooperative customers under state-approved rate cases ensuring cost recovery with stipulated ROE bands [S4]. Transmission services form a secondary but critical segment reflecting grid backbone maintenance and interconnection responsibilities.

This segmental composition entrenches Xcel’s regulated asset base (RAB), which enjoys protection from competition through regulatory oversight but requires continuous upgrades—particularly supported by rate cases setting allowed return parameters based on historically prudent capital investments [S4][S6]. The geographic diversity offers some balance yet the company remains sensitive to policy shifts in core jurisdictions.

Future Growth Drivers: Grid Modernization and Renewables Integration

Strategic priorities revolve around decarbonizing energy delivery through integrating renewables and modernizing distribution networks [N5]. Investments aim at enhancing system resiliency via advanced metering infrastructure (AMI), smarter grid controls capable of handling variable renewable generation, and increased capacity additions including solar and wind assets backed by federal incentive provisions.

Such initiatives align well with broader industry decarbonization mandates incentivizing utilities to transition away from coal-fired generation toward cleaner resources . Grid modernization not only supports environmental objectives but facilitates operational efficiencies in load dispatching and outage management—critical as demand grows from electrification trends including EV adoption.

Regulatory and Capital Intensity Challenges Impacting Expansion

Despite supportive regulatory environments affording revenue visibility, the company flags ongoing risks from uncertain regulatory changes that may alter allowable returns or impose additional compliance costs [S5][S6]. Heavy upfront capital requirements for network enhancements strain both liquidity profiles and free cash flow generation even as rate recoveries occur with lags.

Rate case processes remain pivotal future catalysts but also represent potential bottlenecks if approvals fall short of requested investments or ROE adjustments—affecting growth projections directly tied to RAB expansions [S4][S6]. Furthermore, shifting political/regulatory landscapes could alter renewable integration pace or cost allocation mechanisms impacting financial outcomes.

Wall Street Sentiment and Near-Term Expectations Post-Upgrade

The recent UBS upgrade affirming Xcel’s investment-grade creditworthiness signals market confidence in the company’s ability to sustain earnings momentum amid sector headwinds [N5–N14]. Analysts highlight consistent quarter previews projecting earnings beats supported by operational stability coupled with strategic investment plans.

This sentiment reflects recognition of Xcel’s moat rooted in regulatory frameworks alongside credible execution on environmental transition pathways—a key differentiator amidst utilities navigating CAPEX intensity versus rate case timings.

Capital Allocation: Maintaining Dividend Growth Amid Cash Flow Pressure

Xcel has consistently increased dividend payouts each year through at least FY2025, distributing approximately $1.28 billion in dividends last year up from $1.01 billion four years prior [F1]. Notably, share repurchases are minimal historically indicating a preference for reinvestment into infrastructure rather than buybacks.

Capital expenditure levels remain elevated given grid modernization demands; while free cash flow (estimated as CFO minus capex) sustains positive territory near $4 billion last fiscal year, capital intensity limits discretionary funding availability for aggressive shareholder returns despite increasing dividends [F1][S25–S29]. This approach aligns with utility norms emphasizing steady dividend policies anchored on regulated cash flows balanced against essential capital reinvestment needs.

Return Metrics Analysis: ROE Trends in a Utility Context

Based on FY2025 net income of roughly $2.02 billion against equity of approximately $23.6 billion yields an implied ROE around 8.5% [F1]. This figure fits comfortably within typical allowed regulatory ROE ranges for utilities which usually target mid-to-high single-digit returns reflecting low-risk business profiles constrained by rate-setting commissions.

Such returns indicate no excessive profitability but stable value creation underpinned by cost plus regulatory frameworks that enable recovery of prudently incurred costs plus reasonable compensation for invested capital.

Liquidity Profile and Debt Structure: Navigating Capital Needs

Xcel’s current ratio hovers around 0.71 underscoring tight near-term liquidity commonly observed in utilities due to regulatory timing mismatches between receivables collection and payables settlement cycles [F1][S5][S7–S29]. However, extensive unsecured debt issuances staggered across multiple maturity bands provide manageable refinancing flexibility complemented by revolving credit facilities.

The company maintains an investment-grade credit profile supported by large asset base collateralizing debt obligations alongside predictable cash flows derived from tariff structures approved by public utility commissions—facilitating access to debt markets despite substantial leverage reflective of heavy infrastructure investments [S5–S9].

What to Watch: Milestones, Rate Cases, and Capacity Additions

Looking forward through H2-2026, key developments include several pending rate case approvals that will determine allowed revenue increases tied directly to grid investments plus renewable capacity build-out schedules highlighted by industry peers' earnings reports [N3][N1]. These decisions will influence Xcel's operational trajectory given their impact on regulatory asset base growth rates as well as allowed ROEs.

Monitoring utility commission rulings in core states alongside deployment progress on AMI upgrades or wind/solar commissioning will illuminate the balance between accelerating modernization efforts versus cost recovery cadence—factors critical for sustaining earnings momentum amid economic pressures at large.

Disclaimer: This report synthesizes publicly available financial data, regulatory filings, and market news to analyze Xcel Energy Inc.'s business dynamics without providing investment recommendations or price forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments