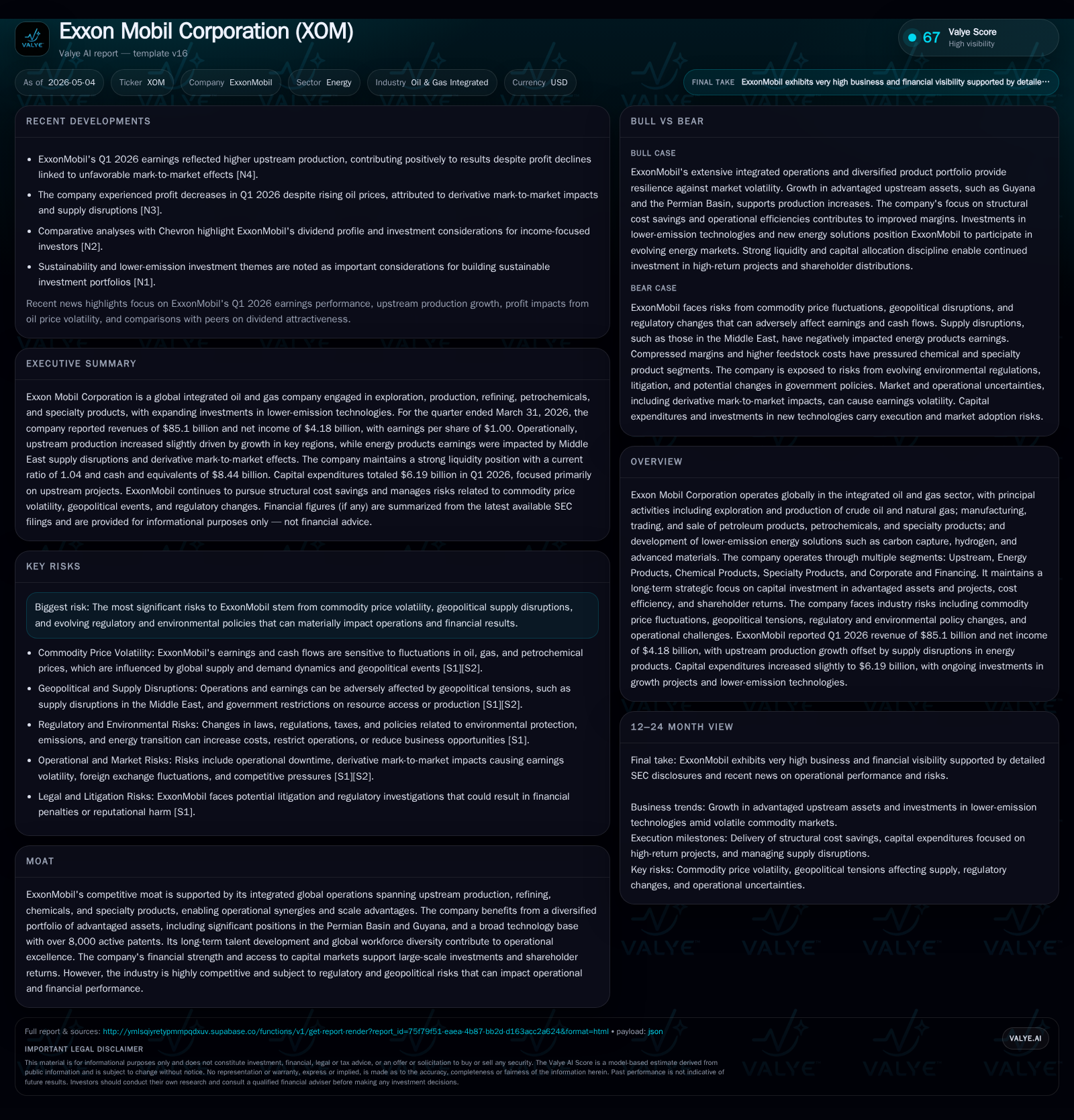

How ExxonMobil’s Integrated Operations Weathered the Q1 2026 Oil Price Surge

ExxonMobil’s first-quarter results reflect resilience amid historic oil price volatility and supply disruptions.

The first quarter of 2026 saw extraordinary volatility in oil and natural gas markets driven by geopolitical tensions and supply shocks, culminating in record monthly price gains in March. ExxonMobil’s integrated business model cushioned the impact of these fluctuations, although net income and cash flow declined versus the prior year due to higher depreciation, working capital movements, and persistent chemical segment headwinds. The firm’s strong upstream positions in key basins, strategic downstream operations, and investments in lower-emission technologies underpin its competitive footing as it navigates market complexities and evolving regulatory landscapes. Growth catalysts include expanded production from advantaged assets and deployment of carbon capture and hydrogen projects, while risks remain anchored in commodity price swings, geopolitical uncertainty, and policy shifts.

Q1 2026 Market Impact and Operational Performance

The first quarter of 2026 presented ExxonMobil with an exceptionally volatile energy market backdrop punctuated by sharp geopolitical disruptions centered on the Middle East. These events precipitated the largest monthly oil price increase ever recorded in March 2026 due to meaningful declines in global crude supply. Additionally, a pronounced contraction in LNG supplies during March elevated natural gas prices across Europe and Asia well above their decade averages [S2]. Despite this late-quarter surge lifting average crude oil prices modestly above fourth-quarter 2025 levels—and holding them roughly midrange within the historic 2010–2019 band—ExxonMobil reported a net income including noncontrolling interests of $4.5 billion for Q1. This marked a decrease of $3.6 billion compared to the same period last year [S2].

Cash flows also reflected these market dynamics; operational cash flow plus asset sales generated $8.9 billion during the quarter—a decline of $5.9 billion versus Q1 2025—with operating activities alone providing $8.7 billion, down $4.2 billion year-over-year [S2]. The earnings shortfall was influenced by a rise in noncash depreciation & depletion charges totaling $6.8 billion (an increase of $1.1 billion from Q1 2025) alongside a $1.8 billion reduction caused by working capital movements [S2]. Notably, while pricing conditions improved later in the quarter owing to supply constraints, overall demand impacts remained stable but cautious due to macroeconomic uncertainties.

ExxonMobil’s Business Model and Segment Dynamics

ExxonMobil operates a classic vertically integrated oil and gas model encompassing exploration & production (Upstream), energy products refining and marketing (Energy Products), petrochemicals manufacturing (Chemical Products), specialty product segments including lubricants and advanced materials (Specialty Products), with Corporate & Financing functions supporting capital allocation [S1]. This structure harnesses operational synergies—crude produced upstream feeds internal refineries downstream enabling margin capture insulation against external raw material cost fluctuations.

Upstream operations emphasize scale advantages via substantial positions in key productive basins such as the Permian Basin of Texas/New Mexico as well as emerging large-scale offshore developments like Guyana. These assets provide relatively low breakeven costs enabling resilience through commodity cycles [S1]. The company's patented technologies—totaling over eight thousand active patents worldwide—support drilling efficiency improvements, reservoir management techniques, and emission reduction processes integral across segments [S1]. While individual patent profitability is not pivotal per se, collective technology leadership galvanizes sustainable operational advantages.

In Energy Products refining units globally benefit from tight integration with upstream feedstocks; however industry-wide chemical margins remain pressured notably with Asian plants facing steep feedstock cost inflation dampening profitability below historical norms [S2]. Specialty Products continue innovation-driven strategies targeting novel materials such as Proxxima™ resin systems which align with emerging sustainability trends but operate in aggressive global markets with diverse competitive offering.

Competitive Positioning within Integrated Oil & Gas

ExxonMobil enjoys a competitive moat anchored by its scale—the breadth of integrated upstream/downstream operations spanning multiple continents buffers cyclical market swings inherent to commodity exposure [S1]. The company’s diversified portfolio mitigates regionally idiosyncratic risks while leveraging financial strength permitting access to favorable capital markets necessary for mega-project investments.

Technology is an enduring pillar: extensive R&D backed by thousands of patents fosters margins optimization via operational efficiency enhancements alongside early mover advantage deploying nascent low-carbon solutions such as carbon capture utilization and storage (CCUS) technologies. Talent development is prominently emphasized with systematic career planning nurturing domain expertise capable of managing complex long-cycle energy projects effectively against evolving regulatory landscapes.

Nonetheless, exposure remains significant to geopolitical events affecting Middle Eastern supply stability as well as regulatory evolutions reflecting climate policy shifts whose timing remains uncertain. Competitive pressures persist from peers aggressively advancing their own integrated resource bases along with technology platforms aiming for emission reductions.

Growth Opportunities Driving Future Earnings Potential

Looking ahead, near-to-medium term growth vectors hinge on several strategic thrusts:

- Expansion of upstream unconventional resource plays with anticipated production volume increases focused on basin-level efficiencies driven by enhanced recovery techniques.

- Leveraging elevated LNG pricing environments particularly benefiting natural gas revenue streams amid constrained global supplies [S2].

- Development of lower-emissions energy solutions including scaling up commercial projects targeting carbon capture infrastructure expansion aligned with World Bank Zero Routine Flaring goals; pursuit of hydrogen production capacity using blue hydrogen approaches; advancement of Proxxima™ resin systems fitting into circular economy frameworks [S1].

- Optimization of petrochemical operations dependent on stabilizing feedstock costs especially within Asian jurisdictions aiming to restore competitiveness.

- Integration benefits expected from partnerships such as those with Denbury Resources focused on enhanced CO₂ EOR (enhanced oil recovery) techniques promising returns synergistic with emission mitigation goals.

Capital allocation is calibrated towards balancing traditional hydrocarbon developments alongside incremental investments in cleaner energy avenues reflecting evolving societal expectations without compromising core financial discipline [S2].

Risks and Constraints to Growth Trajectory

Despite positioning advantages, several material risks could constrain growth trajectories:

- Commodity price vulnerability persists despite recent spikes; sudden demand shifts or supply rebalances may induce significant earnings volatility impacting cash flows necessary for reinvestment.

- Regulatory uncertainty tied to accelerating climate policies could impose additional capital costs or operational restrictions complicating project economics or permitting timelines.

- Geopolitical instability—particularly disruptions associated with Middle Eastern operations or trade sanctions—may unexpectedly affect production continuity or export logistics.

- Operational execution risk inherent in technically complex projects spanning unconventional resource extraction or new technology commercialization phases could delay returns.

- Capacity constraints at existing midstream/refining/chemical facilities might limit responsiveness to demand surges imposing margin squeezes until expansions come online.

- Feedstock cost inflation particularly within chemicals introduces margin pressure influencing segment profitability dynamics adversely [S2].

These risks underline the need for continuous innovation agility coupled with rigorous risk management frameworks embedded throughout ExxonMobil's global footprint.

Key Milestones and What to Watch Next

Several future developments deserve attention as markers of ExxonMobil's trajectory:

- Upcoming quarterly results will shed light on sustained upstream production growth capability amidst fluctuating commodity cycles.

- Progress reports concerning carbon capture initiatives—both technological deployment status and policy support evolution—will illustrate transition pathway viability.

- Monitoring capex guidance recalibrations toward greenfield versus brownfield projects will illuminate strategic emphasis shifts responding to market signals.

- Shareholder return programs including buybacks or dividend adjustments underpinned by free cash flow trends amid commodity fluctuation pressures will indicate financial discipline tone.

- Supply chain resilience amid lingering post-pandemic and geopolitical trade frictions could impact operational cadence.

- Regulatory announcements particularly in major jurisdictions defining emissions targets or incentivizing lower-carbon fuels will dictate opportunity/universe expansion for newly developing product lines.

Overall market pricing relative to historical benchmarks combined with internal operating metrics such as refinery run rates or chemical unit utilization will provide timely signals validating ongoing strategy execution effectiveness [S2][S3][N2][N4].

This analysis synthesizes ExxonMobil's latest quarterly disclosures alongside broader annual context to elucidate how its integrated operations enable navigation through volatile early 2026 energy markets. The firm’s deep asset base coupled with cutting-edge technology investments position it well for current challenges yet underscore sensitivity to external factors shaping future performance outcomes. As global energy landscapes evolve rapidly under economic pressures and sustainability imperatives, watching ExxonMobil’s execution on both traditional hydrocarbons and emerging low-carbon initiatives will be critical for assessing its longer-term resilience.

This report does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments