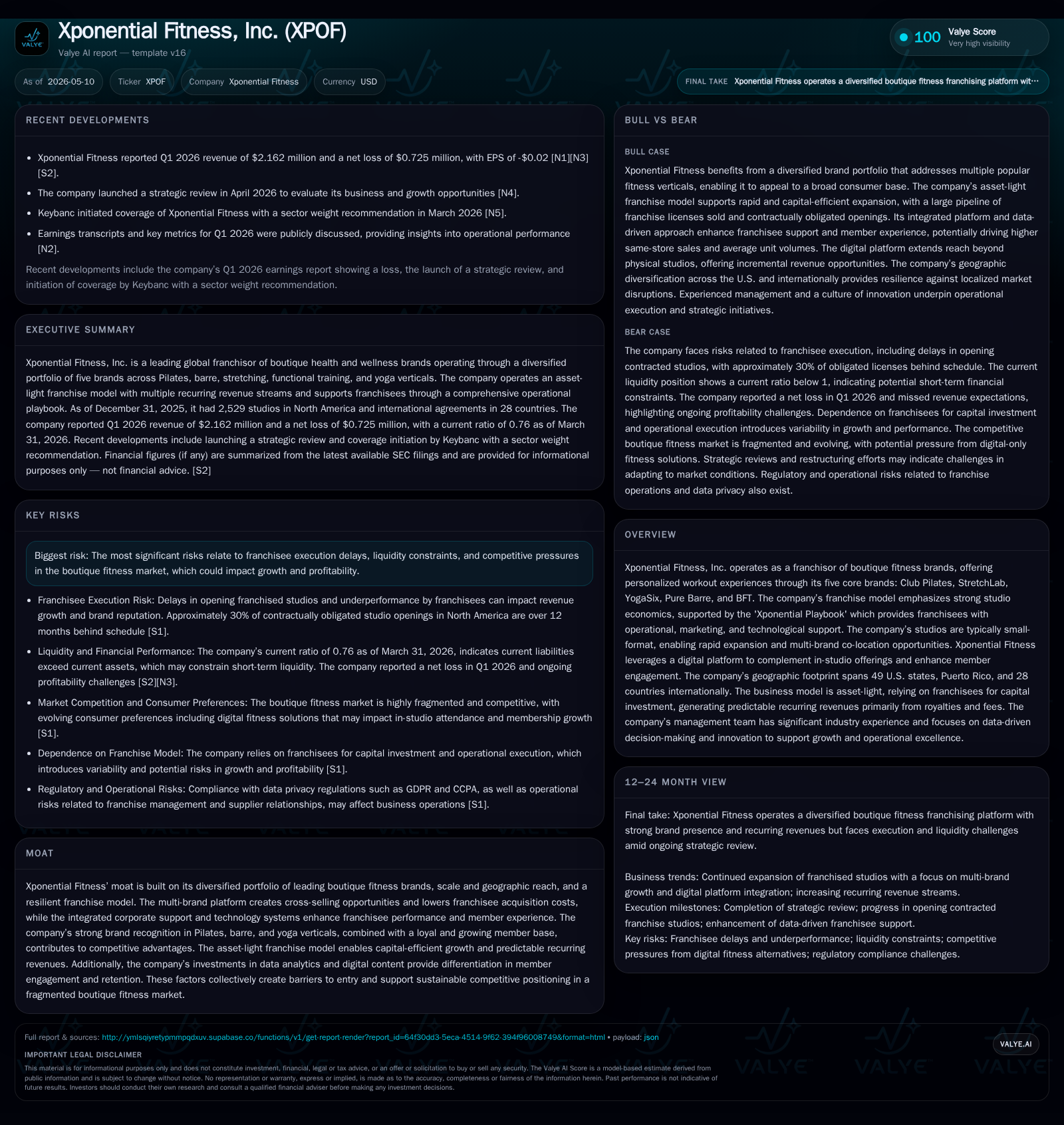

Xponential Fitness Strengthens Franchise Model with Q1 Operational Advances

Xponential Fitness's latest quarter reveals progress in franchise development and operational execution within its multi-brand boutique fitness platform.

In its Q1 2026 filing, Xponential Fitness highlighted operational advances centered on studio expansion and franchisee support across its core boutique fitness brands. The company’s asset-light franchising model, leveraging five complementary brands and a proprietary operational playbook, continues to underpin geographic and unit growth amid ongoing industry competition. While leverage and execution risks persist, management’s strategic initiatives around data-driven member engagement and multi-brand co-location remain key growth vectors.

Quarterly Operating Highlights and Recent Developments

Xponential Fitness’s first-quarter ending March 31, 2026 (Q1 2026) report ([S2], [S3]) signals continued expansion of its boutique studio footprint alongside intensified franchisee support programs aimed at operational consistency. The company reported incremental additions of studios across its flagship brands—Club Pilates, Pure Barre, YogaSix, StretchLab, and BFT—reflecting successful progress on new unit openings despite macroeconomic headwinds impacting discretionary spending ([N1], [N2]). Management underscored enhancements to the proprietary 'Xponential Playbook' designed to optimize operational execution at franchised locations.

The Q1 results revealed mixed revenue performance with modest misses over estimates attributed partially to timing delays from some franchisees in opening scheduled studios ([N3]). Nevertheless, underlying metrics such as unit economics and same-store sales trajectories showed resilience. The May 7 event filing ([S3]) accompanying the earnings release also highlighted a strategic review underway to refine portfolio positioning and cost structures in light of evolving competitive dynamics.

Xponential’s Franchise-Based Business Model and Brand Portfolio

Xponential Fitness operates primarily via an asset-light franchising model that generates predictable recurring revenues from royalties on studio sales, initial franchise fees, and ancillary service charges ([S1]). Its five core brands span differentiated verticals within the boutique fitness ecosystem: Club Pilates (largest U.S. Pilates brand), Pure Barre (leading barre workouts), YogaSix (largest franchised yoga brand), StretchLab (specialized assisted stretching), and BFT (functional training). This multi-brand approach allows Xponential to leverage cross-selling potential to consumers while offering franchisees avenues for multi-brand co-located studios enhancing capital efficiency.

The company mandates that franchisees procure equipment exclusively from approved suppliers to maintain consistent quality across studios; equipment lifecycle replacement is guided by manufacturer timelines ensuring service reliability ([S1]). Furthermore, integrated technology platforms bolster member engagement by blending digital content with in-studio experiences—a notable differentiator amid rising consumer expectations for seamless omni-channel fitness interaction.

With operations spanning all 49 U.S. states plus Puerto Rico and reaching into 28 international countries ([S1]), Xponential positions itself as one of the largest global franchisors of boutique fitness brands. This broad geographic reach provides scale advantages in marketing fund utilization and vendor negotiations.

Competitive Positioning within the Boutique Fitness Industry

The boutique fitness sector is fragmented but expanding, characterized by consumer demand for community-centric, specialized workout experiences in small format studios ([S1]). Xponential commands competitive advantages through its diversified brand portfolio that spans several key subsegments—Pilates, barre, yoga et al.—reducing dependency on any single vertical.

Cross-brand platform benefits lower customer acquisition costs and increase lifetime value via multi-brand memberships or bundled offerings. Unlike standalone local studios or single-brand chains, Xponential’s ecosystem creates switching costs through proprietary content delivery platforms and standardized franchisee operational support systems ([S1], [N1]).

However, industry-wide challenges include saturation risks in urban markets where studio density increases competition for members alongside higher real estate costs. Regulatory scrutiny around franchise disclosure compliance adds complexity to rollout strategies globally ([S23]).

Drivers Fueling Growth in Studio Expansion and Member Engagement

Growth drivers are anchored in accelerating new studio openings backed by enhanced franchisee training programs refined under the Xponential Playbook ([S2]). This initiative aims to raise unit-level profitability by improving service delivery efficiency while supporting complex multi-brand site strategies.

Adoption of Xponential’s digital content platform fosters improved engagement metrics which management views as increasingly important given consumer shifts toward blended fitness modalities combining at-home and in-studio activities ([N4]). Geographic expansion remains robust particularly within untapped international markets offering long-term runway.

Additionally, the streamlined small-format studios allow rapid scaling without large upfront capital commitment from Xponential itself but hinges critically on franchisee access to financing—a potential bottleneck mitigated somewhat by third-party financing partnerships guaranteed partly by the company ([S12], [S13]).

Risks and Constraints Impacting Execution and Profitability

Principal execution risks revolve around franchisee capacity to timely open new locations aligned with planning assumptions or market conditions ([S22]). Any delays can disrupt revenue recognition cadence impacting near-term performance. Financial constraints at the franchisee level may hinder expansion given macroeconomic volatility affecting discretionary spending patterns captured in attendance variability ([S23]).

High leverage totals approximately $523.7 million as of Q1 end with a sub-1 current ratio (0.76) spotlight liquidity tightness that could limit flexibility amidst uncertain economic cycles ([F1], [S2]). Debt servicing demands may divert resources away from growth investments or marketing efforts enhancing competitive positioning.

Ongoing government investigations related to compliance with franchise laws impose reputational risk as well as potential operational restrictions including temporary limitations on selling franchises in select jurisdictions ([S23], [S24]). Dependence on a single provider for critical information systems represents concentration risk threatening business continuity if disrupted.

Leadership transitions noted historically may challenge management execution consistency although recent reports suggest stabilization efforts underway ([S23]). Competitive intensity remains elevated across boutique fitness especially from emerging digital-only platforms offering low-cost alternatives.

Upcoming Catalysts and Points to Monitor for Investors

Investors should track progress on the strategic review announced prior to Q1 release that may culminate in portfolio rationalization or operational restructuring measures intended to enhance profitability margins ([N4], [S3]). Subsequent quarterly guidance updates will serve as barometers for trajectory stabilization or acceleration.

Key indicators such as new franchise licensing agreements signed per quarter along with digital platform monthly active users provide tangible metrics linked directly to revenue levers. Monitoring regional penetration rates especially internationally will elucidate scope for sustained network effect gains.

Execution milestones tied to multi-brand co-location rollouts could unlock incremental revenue synergism enhancing franchisor take rates. Any regulatory clarity developments concerning ongoing investigations remain critical watch points due to their implications for expansion capabilities.

Current Financial Position: Liquidity, Leverage, and Cash Flow

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Total debt | $524mm | |

| 2026-03-31 | ||

| Net debt | $524mm | |

| 2026-03-31 | ||

| Current assets | $75mm | |

| 2026-03-31 | ||

| Current liabilities | $99mm | |

| 2026-03-31 | ||

| Current ratio | 0.76x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

The March 31, 2026 quarter-end balance sheet reflects total debt of $523.7 million with net debt approximately equal given modest cash levels; current assets stood at roughly $74.99 million against $99.02 million current liabilities resulting in a current ratio of 0.76 indicating some liquidity pressure but manageable near-term obligations given cash flow generation capacity ([F1], [S2]).

The company’s credit agreement matured recently includes covenants limiting additional indebtedness or material asset disposition without lender approval causing capital allocation discipline ([S5], [S6]). Cash flow from operations has improved compared to prior periods; however elevated interest expense above $49 million per annum continues consuming significant free cash flow potential ([S17]).

| Metric | Value | Period Ended |

|---|---|---|

| Total Debt | $523.7M | |

| 2026-03-31 | ||

| Net Debt | $523.7M | |

| 2026-03-31 | ||

| Current Assets | $74.99M | |

| 2026-03-31 | ||

| Current Liabilities | $99.02M | |

| 2026-03-31 | ||

| Current Ratio | 0.76 | |

| 2026-03-31 |

This analysis is based solely on information available through SEC filings dated May 8, 2026 [S2], May 7 event filings [S3], annual filings [S1] plus referenced news reports without any speculative or forward-looking extrapolations beyond stated disclosures. It is intended for informational purposes only without any investment recommendation or advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments