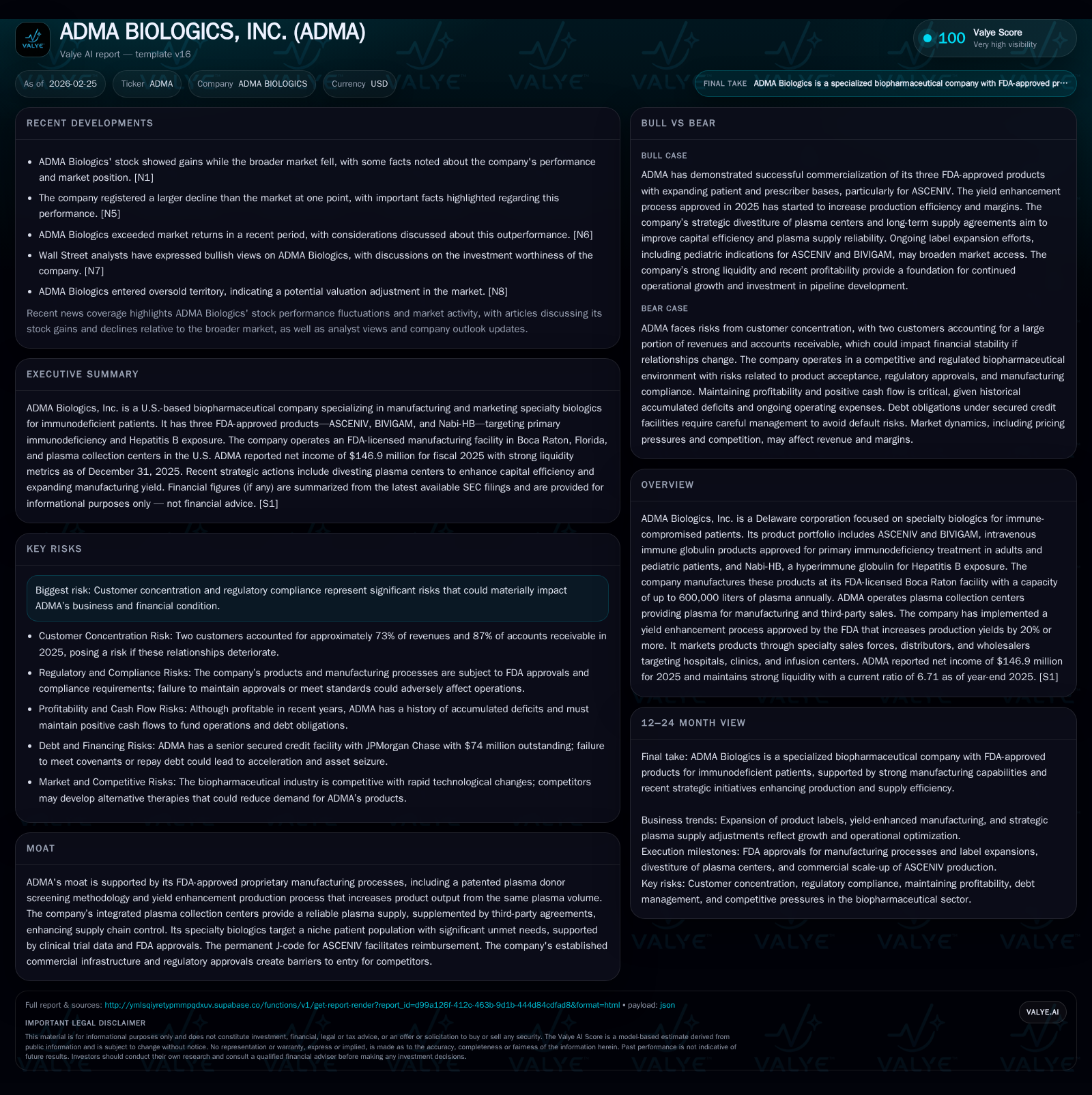

ADMA Biologics' Financial Turnaround and Strategic Supply Chain Shift Amid Specialty Biologics Expansion

ADMA Biologics achieved sustained profitability through proprietary manufacturing efficiencies and strategic plasma sourcing while managing significant customer concentration and regulatory risks.

ADMA Biologics, Inc. transitioned from losses to profitability by 2024 and 2025, driven by its specialty biologics portfolio targeting immunodeficient patients. The company leverages FDA-approved manufacturing with enhanced plasma utilization and recently divested select plasma centers to optimize capital structure and diversify raw material sourcing. Robust operating income and positive free cash flow underpin reinvestment capacity, while pipeline advancement including a pneumococcal hyperimmune candidate signals growth potential. Risks remain around customer concentration, regulatory compliance, and reimbursement dynamics.

Historical Performance and Growth Drivers

ADMA Biologics has demonstrated a marked financial turnaround over recent years. The company reported net income of $146.9 million for fiscal year (FY) 2025, a substantial improvement from prior years marked by losses [F1]. Revenue growth accelerated approximately 43.9% year-over-year leading into FY2025, driven primarily by sales of intravenous immune globulin (IVIG) products ASCENIV and BIVIGAM targeting primary immunodeficiency disorders (PIDD) [F1].

Operating income increased by nearly 38% in FY2025 to $191.4 million, reflecting enhanced operational leverage through increased volumes and proprietary manufacturing yield improvements [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 147 | 50 | 191 | 23 | -25.7% |

| 2024 | 198 | 119 | 139 | 8 | +800.0% |

| 2023 | -28 | 9 | 22 | 5 | +57.2% |

| 2022 | -66 | -60 | -39 | 14 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 28 | 30.8 |

| 2024 | 110 | 56.6 |

| 2023 | 4 | -20.9 |

| 2022 | -73 | -43.4 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures beyond earlier years are not explicitly disclosed; however trends indicate strong growth as reflected in profitability metrics [F1].

Commercial Footprint and Product Portfolio

The company’s portfolio includes three FDA-approved specialty biologics:

- ASCENIV: IVIG approved for treatment of PIDD; first commercial sales commenced October 2019.

- BIVIGAM: IVIG indicated for PI including pediatric patients aged two years and older; commercialized since August 2019.

- Nabi-HB: Hyperimmune globulin for hepatitis B exposure treatment.

Manufacturing occurs at an FDA-licensed facility with annual plasma processing capacity near 600k liters. ADMA employs a proprietary yield enhancement process that improves plasma utilization by more than 20%, providing a cost efficiency advantage [S1].

Distribution channels include a specialty sales force engaging hospitals and infusion centers as well as partnerships with major distributors BioCare Inc. and Priority Healthcare Distribution (CuraScript). These two customers represented approximately 73% of consolidated revenues in FY2025 highlighting notable customer concentration risk [S11][F1].

Supply Chain Strategy and Capital Efficiency

In late FY2025/early FY2026 timeframe ADMA divested three plasma collection centers but retained seven others under direct ownership [S23]. This strategic shift enables diversified plasma sourcing via long-term purchase agreements from third parties while reducing capital intensity tied to collection operations.

This transformation is designed to optimize capital deployment enabling reinvestment in production capacity expansion—particularly for ASCENIV—and enhance supply reliability through multiple sourcing channels while retaining control over high-titer plasma essential for hyperimmune products.

Pipeline Development

ADMA is advancing SG-001—a hyperimmune globulin candidate targeting multiple serotypes of Streptococcus pneumoniae. Having completed pilot-scale batch production with ongoing animal studies indicates pipeline maturation. The company plans a pre-Investigational New Drug (IND) submission during fiscal year 2026 which may facilitate entry into registrational clinical trials potentially accelerated via their Commissioner’s National Priority Voucher application submitted September 2025 [S1].

This development effort aims to broaden therapeutic indications beyond current IVIG products addressing niche immunodeficiency markets.

Financial Health and Capital Allocation

As of the end of FY2025:

- Stockholders’ equity stood at approximately $477 million reflecting strengthened net asset value versus prior years [F1].

- Operating cash flow was $50.4 million after declining from prior year’s peak due to elevated capital expenditures totaling $22.6 million supporting infrastructure growth initiatives [F1].

- Free cash flow remained positive at approximately $27.8 million indicating capacity for reinvestment alongside shareholder returns.

- Share repurchases amounted to $31.9 million demonstrating active capital return policies concurrent with growth investments [F1].

Leverage is managed under senior secured credit facilities totaling up to $300 million with $74 million outstanding bearing variable interest rates tied to SOFR plus spreads. These facilities are secured by liens on company assets imposing covenants that require careful liquidity management amid ongoing capex spend [S5][S6].

Return on equity is estimated near ~30.8%, signaling robust profitability relative to invested capital despite some fluctuations in operating cash flow year-over-year [F1].

Regulatory Environment and Risks

ADMA operates under extensive FDA oversight encompassing manufacturing quality controls (cGMP), post-marketing safety requirements including Risk Evaluation and Mitigation Strategies (REMS), and pricing transparency regulations affecting reimbursement reporting [S7][S8][S9][S12][S20].

Key risks include:

- Customer concentration risk from reliance on BioCare and CuraScript which could materially impact revenues if disrupted [S11][S18].

- Potential regulatory enforcement actions related to manufacturing compliance or pricing inaccuracies could affect operations materially.

- Product liability exposures requiring adequate insurance coverage; adverse claims could affect reputation or commercialization capacity [S12][S25].

- Evolving drug pricing reforms domestically and abroad may pressure net pricing levels despite FDA approvals impacting market access dynamics [S14][S22][S24].

- Data privacy regulations such as HIPAA impose obligations on donor information management within ADMA BioCenters operations [S14].

Forward-Looking Considerations

While detailed public guidance remains limited beyond preliminary statements pointing to an improved outlook for fiscal year 2026 [N1], critical factors shaping future performance include:

- Scaling ASCENIV production leveraging proprietary yield gains combined with operational capacity freed through plasma center divestitures.

- Clinical progression of SG-001 potentially broadening revenue base beyond current core indications.

- Managing concentrated customer relationships through diversification or contract negotiations.

- Navigating reimbursement environment volatility driven by healthcare policy reforms affecting drug pricing.

- Sustaining compliance rigor mitigating risks from regulatory inspections or enforcement actions that could disrupt supply chains or sales efforts.

Conclusion

ADMA Biologics exemplifies a specialty biologics firm that has successfully transitioned into profitability through focused product innovation combined with strategic supply chain realignment targeting underserved immunodeficient populations. Its recent financial performance evidences operational maturity supported by established product approvals alongside pipeline initiatives addressing invasive pneumococcal disease vulnerabilities. However, elevated customer concentration coupled with complex regulatory landscapes necessitates continued vigilance. For investors seeking insight into niche plasma-derived biopharma companies balancing growth investments against evolving reimbursement challenges, the company’s trajectory offers instructive perspectives on key operational levers driving sustainable expansion.

This analysis is based solely on publicly available filings as of February 25th, 2026 including the Form10-K for year-end December31st , company press releases dated early January-February 2026 plus SEC disclosures without offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments