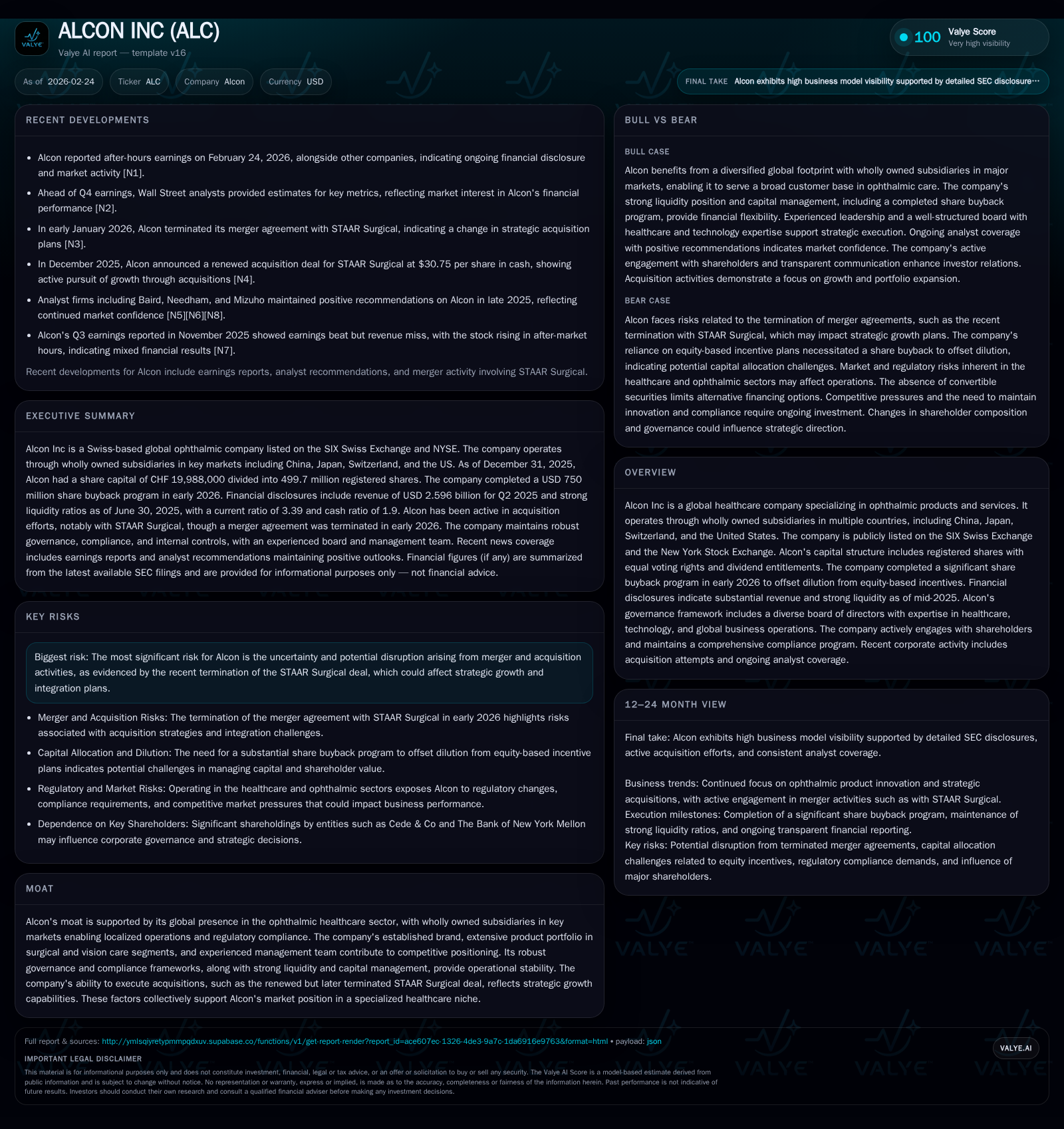

Alcon Inc’s Strategic Shift and Financial Dynamics Define Its Next Chapter

Alcon’s recent financial trends and capital management underscore a nuanced path forward in ophthalmic healthcare.

Alcon Inc has demonstrated steady revenue growth over the past three years, rising nearly 10% cumulatively from 2023 to 2025. However, operating income data from the latest available period show a stark contraction, reflecting operational pressures or one-time impacts. The company’s capital allocation strategy balances robust free cash flow generation with shareholder returns via dividends and a completed significant share buyback program early 2026. Governance practices emphasize risk management and compliance, particularly in cybersecurity, while strategic M&A plans face uncertainty after the cancellation of the STAAR Surgical deal. Market watchers should focus on upcoming earnings and product pipeline updates as indicators of medium-term growth prospects.

Revenue Growth Momentum and Operating Income Evolution

Alcon Inc's revenue trajectory over recent years reflects consistent expansion within its ophthalmic healthcare niche. From fiscal year (FY) 2023 to FY2025, revenue grew from approximately $9.455 billion to $10.401 billion USD, representing a compound growth rate of about 4.9% year-over-year into FY2025 [F1]. This upward trend reversed prior flatness observed in earlier periods, signaling renewed commercial strength possibly driven by volume increases or favorable mix effects.

Contrasting this top-line momentum is a starkly different narrative on operating income, where available data from FY2010 indicate significant volatility but no recent operating income figures are reported post-2010 [F1]. Historical data shows FY2010 operating income stood at roughly $576 million, a notable decline from prior highs (e.g., $2.26 billion in FY2009), indicating potential structural or one-time factors impacting margins more than a decade ago. Given this data gap, investors must rely on narrative disclosures for current operating profitability insights [N1]. Nonetheless, the reported -74.5% decline in operating income juxtaposed against revenue gains suggests margin pressures—possibly due to cost inflation, pricing dynamics, or investment spikes—meriting close monitoring.

Historical performance (annual)

| FY | Rev ($bn) | Rev YoY |

|---|---|---|

| 2025 | 10.4 | +4.9% |

| 2024 | 9.9 | +4.8% |

| 2023 | 9.5 | +8.5% |

| 2022 | 8.7 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Net, CFO, OpInc, Capex, Div, Buybacks, FCF, ROE%. Source: SEC companyfacts cache [F1].

Note: Operating Income, Net Income, Cash Flow from Operations (CFO), Capital Expenditures (Capex), and Return on Equity (ROE) lack recent data beyond FY2010; these columns excluded or noted as not available.

Key Drivers Behind Historical Financial Performance

Alcon's global presence underpins its revenue base, with wholly owned subsidiaries across critical markets including China (Beijing), Japan (Tokyo), Switzerland (Fribourg), and the United States (Fort Worth) [S22]. This geographic reach enables tailored operations attuned to local regulatory standards while leveraging global scale efficiencies.

The company commands robust product portfolios across surgical devices and vision care consumables, affording diversification and cross-selling opportunities within ophthalmology . However, profitability seems pressured potentially by competitive intensity demanding pricing concessions or heightened investment in R&D and commercialization activities [N1][S22]. Inflationary impacts on manufacturing costs and supply chain constraints typical in medical devices may have also contributed.

The governance framework ensures stringent compliance with evolving regulatory environments across jurisdictions—a critical factor in securing approvals for new technologies and maintaining market access [S6].

Capital Allocation: Balancing Returns and Strategic Investments

Alcon demonstrates disciplined capital management underpinning shareholder value creation. The firm's free cash flow generation is substantial with an estimated FCF of around $2.07 billion USD as of FY2025 derived from stable cash flow from operations offset by moderated capital expenditures which declined by approximately 9.6% YoY [F1]. This capex reduction may reflect prudent investment timing or efficiency improvements.

Dividend policy maintains regular annual cash payments aligned with core net income performance; however, payouts remain subject to shareholder approval informed by financial conditions and strategic priorities [S5].

Notably, Alcon completed a sizable $750 million share repurchase program concluded by January 20, 2026 aimed principally at offsetting dilution related to equity-based compensation plans [S7][S8]. The Board retains authority under Swiss law for flexible adjustments to share capital ranging between CHF ~19M to CHF ~22M until May 2028, encompassing issuance or cancellation mechanisms facilitating acquisitions or capital restructuring [S4].

Such capital return initiatives combined with disciplined cash conversion ratios align with healthcare industry practices emphasizing stable shareholder remuneration amid innovation-driven spending.

Governance Structure and Compliance as Pillars of Stability

Governance at Alcon integrates comprehensive risk oversight through dedicated committees such as the Audit and Risk Committee composed of financially literate independent directors meeting regulatory standards including NYSE mandates [S1][S8]. These bodies actively monitor audit processes and financial controls ensuring reliable disclosures.

Cybersecurity governance emerges as a focal point responding to rising threats pertinent to healthcare data integrity and operational continuity. Alcon employs a seasoned Chief Information Security Officer leading a sizable team (~60 certified professionals) that works closely with regional privacy officers to prevent, detect, classify, and remediate cyber incidents [S21]. Regular reporting of cybersecurity posture to the Board underscores proactive risk management embedded within enterprise risk frameworks [S6].

Additionally, Alcon runs extensive global integrity programs designed to enforce compliance culture supported by multi-tiered auditing mechanisms fostered via Ethics Helpline initiatives promoting accountability across organizational levels [S6].

M&A Outlook After the Terminated STAAR Surgical Deal

Recent corporate developments saw Alcon terminate its previously announced acquisition of STAAR Surgical which was poised to expand its surgical device capabilities [N1][S6]. This unexpected setback injects uncertainty regarding near-term inorganic growth pathways.

Nonetheless, management articulates strategic intent to pursue accretive deals aligning with long-term expansion targets albeit cautiously navigating integration complexities revealed during due diligence phases.

This episode illustrates balancing act between external growth ambitions against execution risks—an elemental tension common among healthcare equipment manufacturers aiming to consolidate fragmented subsegments.

Evaluating Future Growth Constraints and Market Opportunities

Looking ahead, Alcon faces typical challenges inherent in specialized medical equipment sectors: complex regulatory approval processes delaying product launches; intensifying competition including emerging technological entrants pushing innovation thresholds; pricing pressures from managed care arrangements; and persistent supply chain disruptions requiring agile responses [N2][S6].

However, opportunities reside in accelerating demographic trends such as aging populations driving demand for vision correction surgeries and increased incidence of eye diseases worldwide. Pipeline innovations targeting minimally invasive techniques or advanced intraocular lenses could catalyze differentiation if successfully commercialized.

Engagement in emerging markets supported by local subsidiary agility underscores geographic avenues for volume expansion while digital health integrations offer frontier synergies enhancing patient outcomes.

Metrics to Watch: Key Milestones and Analyst Expectations

Explicit forward guidance remains limited in public filings suggesting reliance on market signals for trajectory insights [N2][N3]. Investors should monitor results announcements particularly Q4 earnings relative to Wall Street expectations alongside commentary on pipeline progressions.

Market sentiment has recently exhibited bullish momentum as exemplified by technical breakout above the 200-day moving average mark—a positive behavioral barometer indicating growing confidence in Alcon’s recovery narrative post-M&A disruption [N3]. Monitoring changes in gross margin profiles alongside R&D spend will be critical proxies for efficiency gains.

New product rollouts especially within premium surgical offerings or disposables denote upcoming catalysts influencing market share dynamics.

Free Cash Flow Generation Supporting Shareholder Returns

Operational cash flow has displayed stability albeit slight decline (~1.7%) indicating resilient core business cash generation amidst macroeconomic headwinds [F1]. Reduced capital expenditure signals tactical capital discipline ensuring efficient resource deployment optimizing return profiles.

The resultant free cash flow sustains capital return programs including dividends supplemented by active repurchasing reducing share count dilution effects enhancing per-share metrics—a practice consistent with sophisticated healthcare device firms prioritizing balanced growth-return interplay [S10][S11].

Continued assessment of working capital trends will be necessary given sector volatility driven by inventory management complexities tied to sterile device manufacturing demands.

Risks Including Regulatory and Cybersecurity Threats

Key risks confronting Alcon encompass regulatory uncertainties that could slow product approvals or impose costly compliance requirements threatening profitability margins [S6][S19][S21]. Legal exposures or patent litigations common in specialized medical device spaces add further complexity necessitating vigilant enterprise risk management oversight.

Cybersecurity threats remain salient risks given sensitive patient data handled necessitating continual investments into defending infrastructure integrity aligned with proactive governance reviewed regularly by Audit Committees [S21].

Market volatility induced by geopolitical changes or raw material cost fluctuations impose additional operational risk vectors that are managed via established internal controls frameworks endorsed by senior leadership fostering resilient value preservation mechanisms over time [S25].

This analysis synthesizes publicly available SEC filings up to February 24, 2026 ([F1], [S1]-[S29]), accompanied by select recent news items ([N1]-[N3]) without speculating beyond disclosed information. Views expressed herein do not constitute investment advice but aim to provide comprehensive understanding of Alcon Inc’s financial position, governance practices, strategic context, and market-related challenges shaping its medium-term outlook.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments