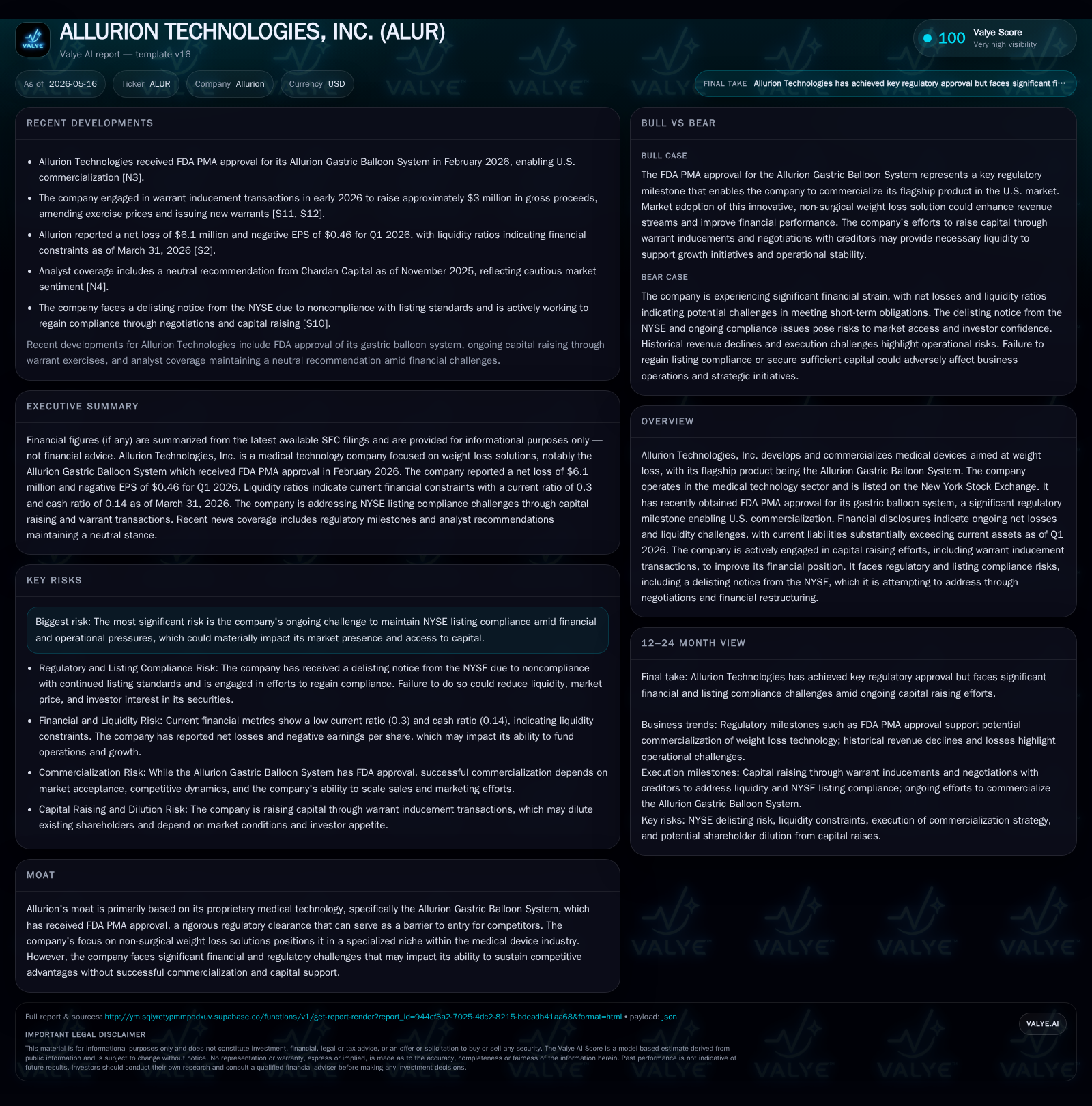

Allurion Technologies Battles NYSE Delisting Risks While Advancing FDA-Cleared Weight Loss Devices

The company’s recent FDA approval marks a key commercial milestone amid severe financial pressures and listing compliance challenges.

Allurion Technologies secured FDA PMA approval for its flagship gastric balloon system in early 2026, enabling U.S. commercialization of its non-surgical weight loss device. Simultaneously, the company faces critical risks with NYSE delisting proceedings triggered by insufficient equity and market capitalization. Liquidity constraints and ongoing net losses pose significant challenges to scaling commercialization efforts despite the promising regulatory endorsement. The firm’s near-term outlook hinges on capital raising success and execution of its FDA-approved product launch while navigating potential loss of major exchange listing.

Recent Operating Update: FDA Approval and NYSE Delisting Proceeding

Allurion Technologies' latest quarterly filing dated May 15, 2026 [S2] spotlighted a stark duality defining the company's near-term trajectory. Following the pivotal receipt of FDA Premarket Approval (PMA) in late February 2026 [S20], which sanctions the U.S. commercialization of its Allurion Gastric Balloon System featuring the innovative Smart Capsule technology [S20], the company simultaneously confronted an existential threat via a March 2026 NYSE delisting notice [S3]. The NYSE determined Allurion failed to meet minimum equity or market capitalization criteria per Section 802.01B of its Listed Company Manual [S3]. Although trading continues on the NYSE pending appeal [S3], this regulatory dichotomy places the company at a crossroads: leveraging an FDA approval that unlocks substantial market opportunity while grappling with risks that could curtail capital access if delisting proceeds.

Management disclosed ongoing vigorous efforts to regain NYSE compliance through financial restructuring initiatives including negotiations with creditors, warrant inducement transactions completed in February 2026 [S27], and active capital raising programs [S2][S3]. The juxtaposition of regulatory success with pressing governance challenges underscores a fragile operating environment where advancing market penetration must be balanced against mounting financial constraints.

Business Model and Product Offering: Non-Surgical Weight Loss Device Innovation

At its core, Allurion develops proprietary medical devices targeting obesity treatment, principally through its flagship Allurion Gastric Balloon System—a swallowable balloon deployed endoscopically or via capsule technology that non-surgically induces satiety to facilitate weight loss over a defined treatment window [S1]. This positioning distinguishes Allurion from more invasive bariatric surgeries and pharmaceutical weight loss interventions by offering a less risky, outpatient alternative with reduced recovery time.

Revenue generation is primarily driven by sales of the balloon system to healthcare providers who administer the procedure, alongside service contracts potentially tied to patient monitoring technologies embodied by the Smart Capsule variant [S1]. The business model relies heavily on physician adoption as well as payer reimbursement policies since affordability and coverage determine patient access rates.

Allurion's FDA PMA clearance enhances its strategic posture by certifying safety and efficacy under rigorous standards that few competitors achieve—this creates an important moat by elevating barriers for rivals while appealing directly to regulators and payers concerned about clinical outcomes [S1]. However, converting this regulatory credential into commercial scale necessitates overcoming constraints related to marketing reach, physician training, and reimbursement enrollment.

Competitive and Regulatory Environment in Medical Weight Management

The broader obesity treatment landscape is intensely competitive and multi-modal: it spans surgical approaches (e.g., gastric bypass), pharmaceuticals (recently bolstered by GLP-1 receptor agonists), lifestyle programs, and medical devices such as balloons and implants. Among these, devices like Allurion's gastric balloon occupy an intermediate niche—attempting to balance invasiveness against efficacy.

Against this backdrop, Allurion's FDA PMA clearance constitutes more than mere regulatory box-checking; it confers significant marketplace credibility relative to competitors reliant on less stringent clearances such as 510(k) notifications. PMA involves rigorous clinical data demonstrating safety and effectiveness, which supports stronger provider recommendation and insurer coverage.

Nevertheless, risks remain endemic given evolving insurance reimbursement frameworks which can limit usage based upon cost-effectiveness assessments. Moreover, entrenched providers might prefer established surgical solutions or newer pharmacotherapies unless demonstrated outcomes decisively shift preference [S1]. Regulatory vigilance will also persist post-market to ensure ongoing compliance—a failure here could jeopardize both license status and reputation.

Growth Drivers: Commercialization, Market Penetration, and New Product Development

Primary growth levers derive from expanding U.S. commercial rollout enabled by FDA PMA status [S20]. This milestone permits marketing directly to American health systems hungry for innovative obesity treatments amidst rising prevalence rates.

Additional growth vectors include geographic expansion beyond initial markets leveraging regulatory approvals internationally obtained prior to U.S. clearance [S1], physician education initiatives to improve adoption rates, strategic partnerships with payers easing reimbursement hurdles, and iterative product enhancements such as integration of connected digital health monitoring via the Smart Capsule platform [S3].

These initiatives seek to enlarge addressable markets by improving patient adherence through remote monitoring tools while providing physicians actionable data—both factors potentially boosting procedural volumes.

However, execution capacity depends heavily on securing sufficient working capital amid currently strained liquidity conditions (discussed below), highlighting an operational tradeoff between scaling investments versus maintaining financial resilience.

Key Risks and Constraints: Listing Compliance, Liquidity, and Market Adoption Challenges

Foremost is the imminent risk from NYSE delisting proceedings initiated March 2026 owing to failure in meeting stockholders’ equity or market cap minimum thresholds (~$50M required) [S3]. Delisting would markedly reduce liquidity for shareholders, constrict access to public equity capital markets for fundraising efforts required for commercialization scale-up [S3]. While management appeals this determination actively [S3], outcome uncertainty persists.

Liquidity constraints are acute: as of March 31, 2026, cash balances stood at roughly $5.06 million against current liabilities around $37.26 million producing a precarious current ratio near 0.3 — a textbook indicator of cash stress impacting day-to-day operations [F1]. Total debt remains elevated near $43.5 million culminating in net debt north of $38 million excluding cash buffers [F1]. These metrics underpin urgent need for successful capital raises or liquidity infusions such as warrant inducements executed recently [S27], yet financing terms may be dilutive or costly given market conditions.

Further commercial adoption risks relate to insurance reimbursement variability across jurisdictions possibly limiting patient affordability; additionally, provider hesitancy around novel procedural adoption can curtail revenue ramp speed despite favorable clinical evidence supporting efficacy [S1]. Failure to convert early interest into repeatable sales cycles could impair long-term viability.

Forward-Looking Indicators and Execution Milestones

Investors and stakeholders should closely monitor several forward markers:

- Progress reports on capital-raising activities including new financing closes or debt-to-equity conversions critical for shoring liquidity [S2][S3].

- Timelines surrounding resolution of NYSE appeal process defining continued listing prospects or transition paths to alternative exchanges like OTCID or NYSE American [S3][S21].

- Early U.S. sales volumes post-FDA PMA launch capturing physician uptake velocity alongside emerging reimbursement codes acceptance.

- Clinical trial updates illuminating real-world performance enhancing payer confidence or driving differentiation in crowded obesity therapeutics market.

- Implementation status of digital health extensions attached to Smart Capsule technology potentially increasing patient adherence metrics.

Achievement or delay across these execution nodes will materially influence operational durability amidst existing financial strain.

Latest Financial Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $5mm | |

| 2026-03-31 | ||

| Total debt | $44mm | |

| 2026-03-31 | ||

| Net debt | $38mm | |

| 2026-03-31 | ||

| Current assets | $11mm | |

| 2026-03-31 | ||

| Current liabilities | $37mm | |

| 2026-03-31 | ||

| Current ratio | 0.3x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

This snapshot portrays an organization wrestling with liquidity headwinds alongside material indebtedness supporting ongoing R&D/commercial activities but risking funding interruptions absent successful capital markets engagement.[F1]

This report is based solely on publicly available SEC filings and company disclosures as of May 16, 2026. It reflects analytical observations without investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments