Eagle Materials Surpasses Q4 Revenue Estimates Despite Profit Decline

The latest quarterly results show Eagle Materials exceeding revenue targets while grappling with margin pressures, reflecting both operational challenges and strategic growth investments.

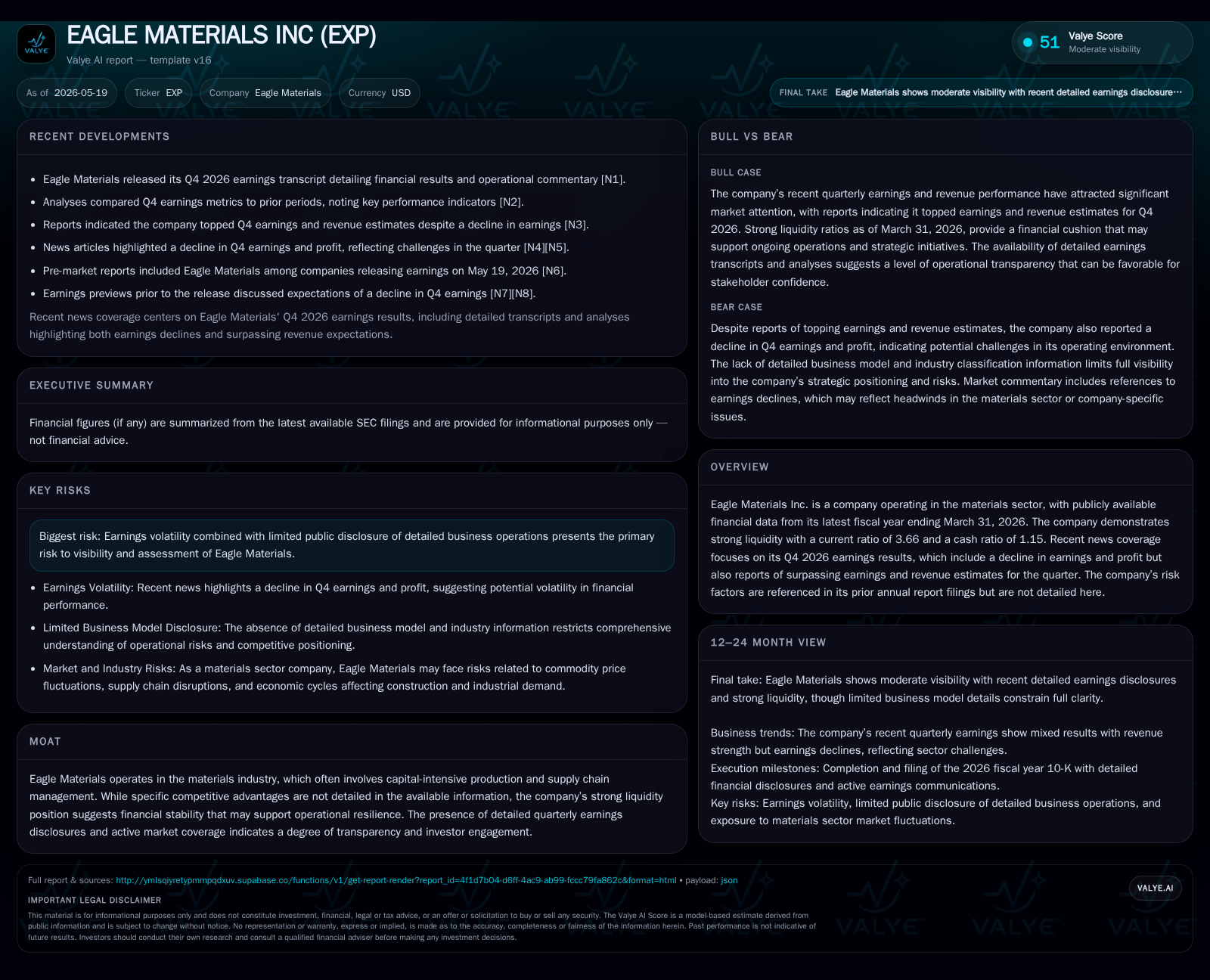

Eagle Materials reported Q4 and full-year fiscal 2026 results with revenues above estimates despite a decline in net income, highlighting short-term earnings volatility amid sustained market demand for concrete and aggregates. The company’s business model centers on heavy materials production, characterized by capital intensity and an expanding footprint through recent acquisitions in Northern Kentucky and Western Pennsylvania. Earnings pressures reflect cost escalations and regulatory headwinds, notably ongoing EPA litigation, while strong liquidity and a solid balance sheet underpin operational resilience. Looking ahead, execution of acquisition synergies and regulatory outcomes are key factors shaping near-term performance.

Q4 2026 Operating Update and Earnings Summary

Eagle Materials released its results for the quarter and fiscal year ended March 31, 2026, on May 19, revealing a nuanced performance mix. The company reported that revenues for the quarter surpassed consensus expectations, a positive signal amid ongoing market demand for heavy construction materials [S3],[N3]. However, this top-line strength coincided with a decline in net income compared to prior periods due to margin pressures intrinsic to raw material costs, workforce expenses, and energy prices [N10]. This disconnect between revenue growth and profit contraction underscores operating cost inflation challenges. The surpassing of revenue estimates implies solid sales volumes or pricing resilience in concrete and aggregate products even as input cost inflation compressed earnings.

Business Model and Product Offerings: Capital-Intensive Materials Focus

Eagle Materials operates principally within the heavy materials industry, deriving revenues from supplying key construction inputs such as concrete, cement, aggregates (sand, gravel), and related building materials [S1]. These products require substantial fixed capital investment in mining operations, processing plants, and distribution networks due to bulk nature and regional logistics constraints. The firm’s business model depends on steady throughput volumes with pricing influenced by local supply-demand dynamics.

Its strategy has included recent acquisitions—Northern Kentucky in August 2024 ($24.9 million purchase price) and Western Pennsylvania in January 2025 ($150 million)—both folded into its Concrete and Aggregates segment [S1]. These acquisitions enhance regional coverage, provide incremental production capacity, and improve supply chain efficiency by consolidating local footprints. In capital-intensive segments like heavy materials, continuous reinvestment is essential to maintaining competitive product quality and meeting environmental standards.

Competitive Positioning Within the Heavy Materials Industry

Within its sector, Eagle competes amid scale-driven dynamics where capital requirements create high entry barriers but also limit pricing flexibility due to competition from major national players as well as regional suppliers [S1]. Pricing power is partially contingent on regional construction demand cycles; switching costs are relatively low for end users but constrained by geographic proximity to sources given transportation economics.

The company faces regulatory complexity exemplified by current litigation against the EPA concerning disapproval of state implementation plans (SIPs) related to ozone National Ambient Air Quality Standards (NAAQS) for Nevada, Oklahoma, and Texas [S1]. This introduces compliance uncertainty that can affect permitting timelines or operational costs. Transparency in reporting such legal proceedings aligns Eagle with industry peers focused on maintaining investor confidence despite regulatory challenges.

Strategic Growth Drivers: Acquisitions and Market Penetration

Eagle’s growth thrust leverages both organic demand expansion aligned with infrastructure spending trends across U.S. regions served plus inorganic expansion via strategic acquisitions completed over the past two fiscal years [S1],[S3]. The Northern Kentucky and Western Pennsylvania deals exemplify targeted moves to augment capacity in growing markets. Such acquisitions allow Eagle to capture incremental volumes while integrating complementary assets which may benefit pricing mix through broader product offerings or enhanced distribution network effects.

With many infrastructure projects requiring large quantities of concrete or aggregates, underlying demand is largely structural rather than cyclical. This steadies volume outlooks despite occasional quarter-to-quarter variability. Continued penetration into underrepresented markets or scaling operations within existing territories forms a core pillar of Eagle’s commercial strategy [N1]. Additionally, potential efficiency gains from combining acquired operations could improve margins over time if integration executes smoothly.

Risks and Constraints: Earnings Volatility and Regulatory Challenges

Despite top-line momentum, Eagle’s quarterly earnings volatility remains a prominent risk factor driven by fluctuating input costs including fuel and raw materials—themselves sensitive to global commodity cycles—and labor market tightness affecting operating expense controls [S2]. Moreover, ongoing EPA litigation regarding SIP approvals constitutes regulatory risk with potentially significant financial implications depending on final rulings or required operational adjustments [S1].

Another challenge resides in the capital-intensive nature of Eagle’s business where supply chain disruptions or delays in capacity expansions can constrain responsiveness to demand shifts.

Limited detailed public disclosures on some operational specifics constrain external visibility on efficiency metrics or backlog positions which adds complexity to forecasting near-term profitability trajectories [S2]. Hence investors should closely monitor cost trends alongside demand signals.

Key Near-Term Catalysts and What to Monitor Next

Upcoming milestones include management’s quarterly guidance updates expected following this earnings report cycle which will shed light on how cost inflation trends evolve alongside volume prospects [S3],[N6]. The pace of benefits realization from recent acquisitions—particularly operational synergies or localized market share gains—will be critical indicators for sustained growth.

Progression toward resolution in EPA litigation represents another key event as it impacts regulatory compliance frameworks potentially influencing capex priorities or permitting outcomes [S3],[N7]. Market watchers should track legal developments closely as well as any public disclosures on mine safety violations or environmental compliance matters highlighted periodically by the company.

Additionally, broader macroeconomic factors such as infrastructure funding levels at federal/state levels may shape overall market demand environment during fiscal 2027.

Financial Profile: Liquidity, Leverage, and Profitability Snapshot

As of March 31, 2026, Eagle Materials displayed strong liquidity with a current ratio of approximately 3.66 supported by nearly $951 million in current assets versus around $260 million in current liabilities [F1]. Cash and equivalents stood robust at about $298 million providing ample buffer for working capital needs. However, net debt remained substantial at an estimated $1.48 billion reflecting ongoing leverage consistent with capital-intensive industry norms [F1].

Profitability metrics showed some pressure due to compressed operating margins amid rising costs though full-year net income totaled approximately $424 million demonstrating underlying cash generation capability [F1],[S3]. The firm’s balance sheet strength coupled with operating cash flow stability supports continuing investment in capacity expansions while managing financial flexibility responsibly.

This analysis avoids investment research views but highlights how Eagle Materials balances top-line growth against margin challenges within a heavily regulated industry environment characterized by sizable capital obligations. Ongoing monitoring of cost dynamics alongside regulatory developments will remain key to assessing sustainable profitably progress.

Financial position in context

As of 2026-03-31, companyfacts shows $298mm in cash and equivalents and $1781mm of total debt [F1]. The same snapshot implies net debt of roughly $1483mm, keeping balance-sheet context relevant but secondary to the operating story [F1]. Current assets of $951mm and current liabilities of $260mm imply a current ratio near 3.66x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments