Amalgamated Financial Corp. Grows Asset Base and Balances Diversified Loan Portfolios Against Market Risks

Stable profitability in 2025 driven by diverse lending and securities holdings, while credit and rate environments pose ongoing challenges.

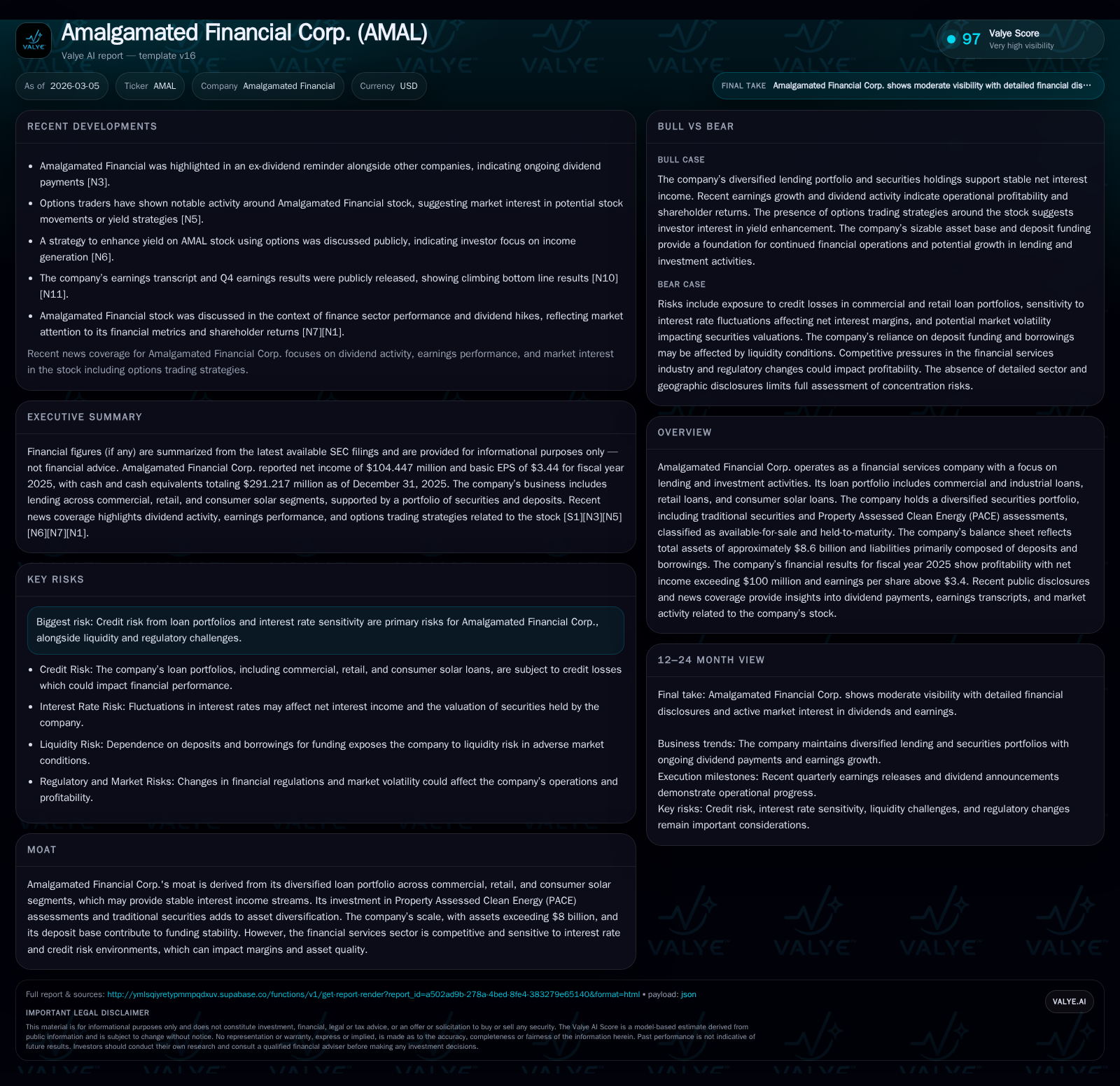

Amalgamated Financial Corp. delivered steady net income of $104 million in fiscal 2025, supported by a diversified loan portfolio spanning commercial, retail, and consumer solar loans and a securities mix that includes PACE assessments. Total assets reached roughly $8.6 billion, funded primarily through deposits, enabling strong funding stability. Despite credible growth in operating cash flows and disciplined capital allocation via dividends and share repurchases, the company’s performance is moderated by interest rate sensitivity and credit risk inherent to its sector. Going forward, growth hinges on managing these risks amid competitive financial markets and regulatory pressures.

Company Overview

Amalgamated Financial Corp., operating with an asset base exceeding $8 billion as of December 31, 2025, positions itself as a diversified financial services firm emphasizing lending and investment activities across multiple segments [S1][F1]. Its loan portfolio includes commercial and industrial loans, traditional retail loans, as well as a developing niche of consumer solar loans, reflecting a strategic diversification that spreads credit risk exposure while capturing growth in renewable energy financing [S1]. This blend is complemented by investments in both traditional securities and Property Assessed Clean Energy (PACE) assessment securities held either available-for-sale or to maturity, contributing asset diversification beyond standard banking book exposures.

Historical Performance Landscape

Finishing fiscal year 2025 with net income of about $104 million marks Amalgamated's sustained profitability track record although representing a marginal decline of roughly 1.9% compared to the prior year’s $106 million [F1]. Operating cash flows showed more robust growth with an increase of approximately 9.4%, reaching $136 million during the same period. Capital expenditures remained modest at around $1.38 million in 2025, decreasing by over 22% year-over-year—a signal that the company maintained tight control over discretionary spending consistent with financial institutions that prioritize capital preservation amidst uncertain environments [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 104 | 136 | 1379000 | -1.9% |

| 2024 | 106 | 124 | 1775000 | +21.0% |

| 2023 | 88 | 117 | 1477000 | +8.0% |

| 2022 | 81 | 147 | 1668000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 17 | 32 | 134 |

| 2024 | 14 | 1 | 122 |

| 2023 | 12 | 8 | 116 |

| 2022 | 11 | 12 | 146 |

Source: SEC companyfacts cache [F1].

*Revenue growth percentage not explicitly reported; included for context.

This snapshot underlines a steady expansion with measured profitability swings typical for a financial entity navigating changing macroeconomic factors such as interest rates and credit cycles.

Business Model and Competitive Moat

Amalgamated’s moat resides partly in its multi-pronged loan segmentation strategy encompassing core commercial-industrial lending alongside retail credits plus innovative consumer solar financing programs—sector niches that generate comparatively stable net interest margins while tapping into evolving markets such as green energy finance [S1]. Their controlled exposure to PACE assessments intersects environmental sustainability trends hypothesized to underpin moderate long-term asset resilience.

The company also manages a substantial deposit base that anchors its funding profile effectively amidst competitive borrowing environments, enhancing liquidity stability essential for underwriting longer-duration loans or holding lower-yield securities without liquidity strain [S19]. That deposit foundation reduces dependency on volatile wholesale funding channels—a structurally advantageous position.

Nevertheless, market competition remains intense within banking and financial services broadly; thus operational efficiency paired with risk management frameworks addressing fluctuating interest rates is crucial for margin preservation.

Growth Catalysts and Constraints

Going forward, Amalgamated’s growth prospects hinge on several factors observed from SEC filings and public disclosures:

- Expansion into consumer solar loans potentially captures growing renewable energy financing demand but entails underwriting discipline amid evolving credit-risk profiles in this relatively nascent sector segment [S10][S18].

- Sustained improvements or innovations in managing PACE-related securities could further cement differentiated asset streams less correlated with conventional market cycles.

- Maintaining solid credit performance within commercial portfolios will remain pivotal as economic cycles slow or sector-specific risks emerge—loan delinquency rates especially within construction or commercial real estate pools need cautious monitoring given past cyclical sensitivities documented broadly across regional lenders.

- Interest rate volatility presents ongoing margin pressure but also opportunities if ALM (asset-liability management) strategies effectively hedge exposures—use of interest rate swaps noted suggest active risk positioning [S4][S6].

Sector analysis insight: The confluence of environmental finance vehicles like PACE alongside rising residential rooftop solar adoption drives specialized lending growth but simultaneously requires robust risk controls due to variable regulatory landscapes across states.

Forecasts, Milestones, and Market Expectations

Official forward guidance has not been prominently featured in recent filings or transcripts; however, quarterly reports including the Q4 earnings beat announced January 22, 2026 reflect management's capacity to exceed consensus estimates under current market dynamics [N3][N2]. Ongoing dividend enhancement signals confidence in underlying cash generation abilities amidst prudent capital returns policy discussions flagged earlier in the year [N5][N12].

Market participants appear attentive to options market activity suggesting varied sentiment around short-term price dynamics possibly linked to tactical yield strategies discussed publicly [N7][N8]. Analysts will likely watch upcoming quarterly disclosures closely for updates on loan portfolio performance metrics especially within specialty segments alongside commentary on ALM effectiveness.

Capital Allocation and Returns Analysis

Amalgamated Financial has demonstrated an increasing commitment to returning capital via dividends which rose steadily from about $11 million in FY22 to over $17 million paid out during FY25—the latter constituting roughly one-sixth of annual net income after tax implying balanced shareholder distributions against reinvestment needs [F1][S8][S29]. Equity buybacks escalated sharply last year reaching over $32 million following modest repurchase pacing previously; this indicates intensified focus on optimizing capital structure post-retained earnings accumulation.

Approximate return on equity based on trailing results stands near a solid ~14.8%, reflecting effective deployment of equity base amid revenue scale [$104m net income / ~$707m equity at end-2024] [F1]. Operating cash flow trends indicate ample liquidity cushion supporting both investment activities and shareholder remuneration without discernible stress.

Sector-Specific Risk Profile

Consistent with most diversified lenders navigating today's evolving financial environment, key risks include:

- Credit exposure: Concentration risk lies within commercial real estate and construction loan sub-segments historically prone to higher default rates under economic duress; emerging consumer solar credit portfolios introduce idiosyncratic underwriting challenges requiring sophisticated analytics to mitigate losses [S7][S10][S18].

- Interest rate fluctuations: Given partial fixed-to-floating debt structures complemented by derivative hedges, sudden rate shifts could compress net interest margins or cause mark-to-market volatility impacting earnings quality.

- Regulatory landscape: Compliance costs tied to ESG practices including scrutiny of green finance products (e.g., PACE/solar loans), evolving banks’ capital adequacy requirements, and broader systemic regulations may pressure operational flexibility.

- Liquidity risks: While deposits form mainstay funding sources (~$7.7b deposits as per latest filings), episodic market stress conditions could prompt swift repricing or withdrawal demands necessitating contingency funding preparedness.

Conclusion

Amalgamated Financial Corp.’s recent performance underscores measured success balancing asset diversification with disciplined capital use amid an environment characterized by competitive pressures and nuanced sector-specific risks including credit performance sensitivities aligned with specialized lending niches like consumer solar loans and PACE assessments.

Steady profitability combined with strong operating cash flow generation supports ongoing dividend growth and meaningful share repurchase programs which enhance shareholder value metrics including ROE positioned near mid-teens percentages—a respectable level reflective of disciplined financial stewardship.

Future visibility rests partly on how effectively management navigates credit cycle variability particularly within commercial real estate exposure alongside prudent risk control measures against interest rate volatility impacts inherent to the banking sector today.

This analysis synthesizes information from publicly filed SEC documents up through March 2026 alongside recent news coverage; it does not represent investment advice nor constitute an endorsement of any kind.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments