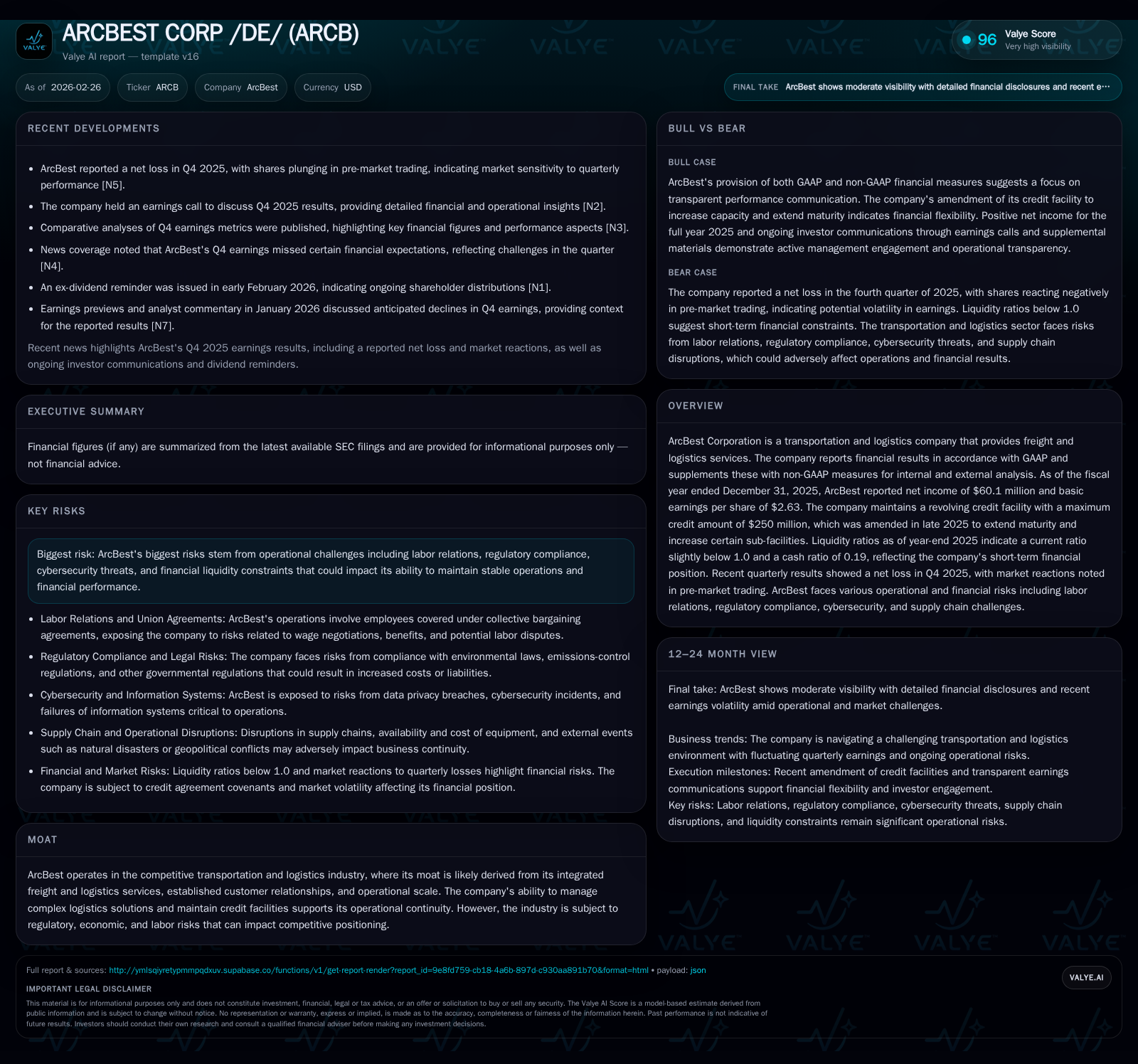

ArcBest’s Sharp Profit Decline Challenges Growth and Capital Allocation in a Soft Freight Market

ArcBest Corporation experienced a marked earnings contraction in 2025 driven by freight market softness and operational headwinds, despite stable liquidity and ongoing capital return programs.

ArcBest reported a significant drop in operating income and net income for the fiscal year 2025, reflecting weaker freight demand, pricing pressures, and typical seasonal volatility in its Asset-Based segment. The company's revenue dynamics show modest shipment growth offset by declining revenue per shipment amid a rational pricing environment. Liquidity remains adequate with a revolving credit facility extended through 2030. Capital allocation continues to support dividends and substantial share repurchases, though returns measured by ROE are under pressure.

Company Overview

ArcBest Corporation operates as an integrated transportation and logistics provider offering freight services across asset-based and asset-light segments. The company's business model leverages an extensive network suitable for both bulk shipments via ABF Freight (asset-based) and managed transportation solutions (asset-light). Known for its operational scale and established customer relationships, ArcBest aims to provide flexible logistics solutions addressing complex supply chain needs .

Historical Financial Performance

Fiscal year 2025 brought considerable headwinds resulting in sharply lower profitability compared to prior years. Operating income fell to $90.3 million versus $244.4 million in FY2024—a decline exceeding 60%. Net income similarly retreated by more than two-thirds to approximately $60.1 million from nearly $174 million the year prior [F1]. This erosion largely reflects unfavorable market conditions impacting rates and shipment sizes.

### Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

| --- | :---: | :---: | :---: | :---: | :---: |

| 2025 | 60 | 229 | 90 | 115 | -65.5% |

| 2024 | 174 | 286 | 244 | 223 | -11.0% |

| 2023 | 195 | 322 | 173 | 219 | -34.5% |

| 2022 | 298 | 471 | 399 | 148 | |

*Source: SEC companyfacts cache [F1].*

### Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

| --- | :---: | :---: | :---: |

| 2025 | 11 | 76 | 114 |

| 2024 | 11 | 75 | 63 |

| 2023 | 12 | 92 | 103 |

| 2022 | 11 | 65 | 323 |

*Source: SEC companyfacts cache [F1].*

Note: Revenue data not available in the provided facts; declines are focused on earnings metrics.

Operating cash flow decreased roughly one-fifth to $229 million, while capital expenditures were nearly halved compared to FY2024 levels—reflecting more cautious investment pacing amid uncertain demand [F1]. This combination resulted in free cash flow near $114 million.

Revenue and Market Dynamics

While explicit full-year revenue data is unavailable, operational details from late-2025 describe modest shipment growth offset by declining price per shipment within ArcBest's segments [S14][S28]. In November 2025, Asset-Based shipments rose about 3%, tonnage increased by approximately the same rate, but revenue per hundredweight dropped around ~2%, suggesting pricing pressures dominate volume gains.

The pricing environment is described as rational but softening overall freight market conditions have led to an expected deterioration of operating ratios by nearly four percentage points sequentially into Q4—a historically weak quarter worsened this cycle by fewer workdays affecting volumes [S14][S28].

Asset-Light revenue per shipment also declined year-over-year due to soft market conditions and a higher mix of smaller sized Managed shipments, despite a slight increase in shipment counts [S28]. Such trends imply competitive pressures and evolving customer demand affecting revenue quality.

Future Growth Prospects

Growth catalysts may derive from expanding Asset-Light managed logistics offerings responding to changing supply chain complexities and e-commerce demands; however, these are tempered by pervasive pricing pressure and operational expenses related to labor negotiations under collective bargaining agreements covering the ABF Freight unionized workforce [S11][S12].

Additionally, industry-wide challenges such as regulatory changes—including emissions controls—and cybersecurity risks pose risks that could cap upside or introduce volatility [S8][S11].

Management anticipates continued softness into Q4 based on seasonality and ongoing market dynamics with quarterly expectations calling for a non-GAAP operating loss between $1 million and $3 million excluding amortization charges—highlighting near-term margin pressures at least through early-2026 [S14].

Capital Structure and Liquidity

ArcBest secured an amended revolving credit facility in late-2025 extending maturity through November 2030 with maximum credit lines of $250 million inclusive of a swing line loans sub-facility ($40M) and letter of credit sub-facility increased recently from $20 million to $50 million—demonstrating proactive liquidity management [S4][S7][S17][S18][S19][S20].

Despite this ample liquidity access, balance sheet metrics at December-end showed current assets of approx. $626 million against current liabilities totaling about $657 million, yielding a current ratio slightly below parity at 0.95; meanwhile cash balances stood near $102 million yielding a modest cash ratio (0.19), underscoring tight working capital positioning common in the transportation sector [F1].

These factors emphasize the importance of working capital efficiency particularly given exposures related to deferred revenues on undelivered freight per accounting policies affecting timing of revenue recognition in the asset-based segment [S28].

Returns and Capital Deployment

Return on equity has compressed alongside profitability pressures with approximate ROE at just over 4.6% for FY2025 compared with significantly higher prior levels—signaling margin contractions impact equity holder returns substantially [F1].

Dividend payouts have remained relatively stable at about $11 million annually reflecting a low dividend yield consistent with a capital allocation focus on share repurchases which proceeded robustly around $75 million last year paralleling historical buyback activity [F1][S13][S27]. This buyback cadence signals management’s confidence in returning excess cash while balancing investment requirements.

Capex spending reduction—from above $220 million mid-cycle levels down near half that amount recently—reflects tactical recalibration amidst a more cautious investment stance likely aligned with market uncertainty around demand normalization post-pandemic surges [F1][S23][S22].

Competitive Positioning & Operational Risks

ArcBest’s moat stems from its integrated offerings combining asset-based freight capabilities with asset-light managed logistics solutions providing tailored scalability attractive to shippers navigating complex distribution networks increasingly leveraging technology-enabled supply chains. Still, intense pricing competition within trucking logistics markets constrains pricing power while labor agreements introduce cost uncertainties with unionized drivers gaining heightened bargaining leverage affecting wage structures and service consistency risks [S11][S12].

Cybersecurity threats along with regulatory compliance burdens—covering environmental standards such as emissions regulations—impose incremental costs and operational complexity risks that weigh on margins alongside potential litigation exposures detailed within SEC filings [S5][S8][N10].

Furthermore, volatile fuel prices remain pivotal given their dual role impacting both operating costs directly through consumption expenses and indirectly via customer resistance or delays collecting fuel surcharges—a perennial challenge for transport operators managing cost pass-throughs effectively.

What To Watch / Analysis

Absent explicit formal guidance beyond industry commentary on Q4 expected losses due to seasonality ([S14]), key forthcoming milestones include monitoring how ArcBest manages cost structure flexibly through these soft patches while growing its Asset-Light Managed segment as a proportion of overall revenues.

Additional factors will include:

- Renewal outcomes of ABF Freight’s collective bargaining agreement influencing labor cost trajectory.

- The evolution of freight market pricing reflecting broader economic demand shifts impacted by inflation trends.

- Execution against liquidity commitments ensuring no covenant breaches amid earnings compression.

- Strategic deployment of free cash flow towards debt reduction versus continued aggressive share repurchases.

- Progress integrating technology upgrades enhancing operational efficiency without incurring disproportionate capital outlays.

Investors will also look for signs that the company can stabilize operating margins given freight tonnage growth albeit at smaller shipment size dynamics potentially pressuring unit economics short term.

Summary

ArcBest’s financial results signal that its historically strong earnings platform is encountering significant challenges from a deteriorating freight pricing environment compounded by usual seasonal softness amplified this cycle along with operational headwinds such as labor costs and regulatory complexity. While top-line tonnage trends show resilience, shrinking revenue per unit dampens overall profitability causing steep declines in operating income and net income reported for FY2025 [F1].[N1][N3]

The company maintains solid liquidity measures with an extended credit facility securing financial flexibility through at least late-decade horizons while preserving shareholder returns through steady dividends augmented by sizable share repurchases reflecting robust free cash flow generation despite capex pullbacks [F1][S13].[N7]

However, lower ROE reveals pressures on value creation highlighting the need for close execution on growth initiatives especially within the managed logistics segment alongside careful cost management amid persistent external risks including labor relations tension, evolving regulation, cybersecurity threats, and fuel price volatility.

In sum, ArcBest stands at an inflection point balancing legacy asset-based freight operations challenged by muted pricing dynamics against emerging opportunities within managed services requiring nimble adaptation amid an environment laden with operational risk factors.

This analysis is based exclusively on publicly available information as of February 26, 2026, without any predictive statements or investment recommendations intended or implied.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments