Avista Corp’s Rate Plan and Capital Spending Drive Steady Growth Amid Regulatory Constraints

Avista Corporation sustains modest revenue and earnings growth driven by rate adjustments and capital investments while navigating regulatory and market risks.

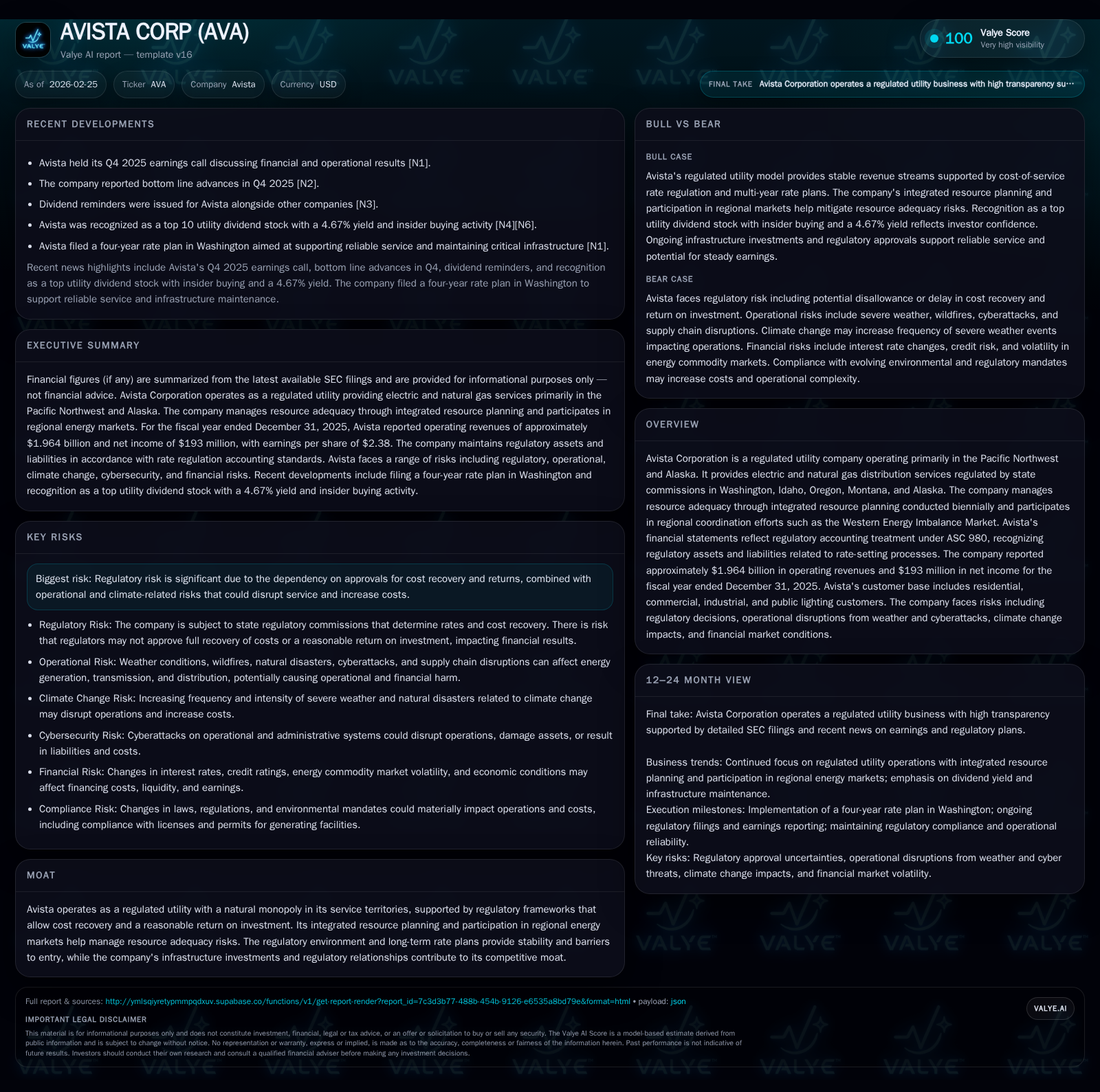

Avista Corporation, a regulated utility primarily serving the Pacific Northwest and Alaska, reported steady revenue growth of 1.3% in fiscal 2025 supported by electric and natural gas distribution services. The company’s integrated resource planning and a recently filed four-year rate plan underpin its strategy to maintain infrastructure reliability and service quality. Capital expenditures remain elevated to support regulated operations, with $570 million spent in 2025 and planned ongoing investment through 2028. Despite regulatory dependencies and potential climate-related operational risks, Avista maintains investment grade credit ratings and pays consistent dividends, though free cash flow remains negative due to substantial capex outlays. Key factors to watch include regulatory approvals of rate plans and the company’s ability to balance capital spending with cash flow generation.

Business Overview

Avista Corporation is a regulated utility servicing customers predominantly in the Pacific Northwest states—Washington, Idaho, Oregon—and Alaska through its subsidiary Alaska Electric Light & Power Company (AEL&P). The company delivers both electric and natural gas distribution services under cost-of-service regulation by state commissions. Its business model depends heavily on regulatory frameworks that authorize cost recovery plus an allowed return on invested capital. Avista's customer base spans residential, commercial, industrial sectors, as well as public lighting.

Historical Performance

Over the past four years, Avista has exhibited stable revenue growth supported by modest increases in volume from retail customers combined with periodic rate adjustments approved by regulators. Total consolidated revenues reached approximately $1.96 billion for the fiscal year ended December 31, 2025—representing a 1.3% increase over $1.94 billion in 2024 [F1]. Net income demonstrated stronger growth at 7.2%, rising to $193 million from $180 million last year [F1]. Operating income also improved by about 15.7%, reaching $354 million.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1964 | 193 | 469 | 354 | +1.3% | +7.2% |

| 2024 | 1938 | 180 | 534 | 306 | +10.6% | +5.2% |

| 2023 | 1752 | 171 | 447 | 258 | +2.4% | +10.3% |

| 2022 | 1710 | 155 | 124 | 190 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 159 | -101 | 7.1 |

| 2024 | 150 | 1 | 6.9 |

| 2023 | 141 | -52 | 6.9 |

| 2022 | 129 | -328 | 6.6 |

Source: SEC companyfacts cache [F1]. | Note: CFO=Operating Cash Flow; Capex=Capital Expenditures; Div=Dividends Paid [F1]

Operating cash flow decreased by approximately 12.2% in the latest year despite net income growth, primarily attributable to increased working capital requirements and higher cash requirements related to power purchases [F1]. The company's elevated capital expenditures reflect investments toward grid modernization, compliance with environmental regulations such as Washington’s Clean Energy Transformation Act (CETA), and infrastructure resilience upgrades.

Future Growth Prospects

Growth drivers for Avista include ongoing demand growth from population increases and economic activity within its service territories alongside strategic rate filings that allow timely recovery of investment costs plus an allowed return on equity (ROE). Notably, the company filed a four-year rate plan in Washington state at the start of 2026 targeting predictable revenue streams for critical infrastructure investment and reliable service maintenance [N13]/[S1]. This multi-year approach reduces regulatory lag risk compared to traditional single-year filings.

Integrated Resource Planning (IRP), conducted every two years, guides generation portfolio decisions to ensure resource adequacy over a twenty-plus-year horizon considering load forecasts, fuel price volatility, renewable integration mandates, regional transmission projects, participation in the Western Energy Imbalance Market (EIM), and western power pools [S1]. These initiatives provide risk mitigation against capacity shortfalls while complying with evolving environmental policies.

Potential constraints stem from regulatory uncertainties—delays or disallowances in rate cases could constrain margins—and climate-related operational impacts such as wildfire risks or extreme weather damaging infrastructure or requiring costly repairs [S26]. Additionally, increasing electrification trends may raise load but also impose demands for additional capital spending.

Financial Outlook & Milestones

While explicit forward guidance on earnings or cash flow was not provided in filings [S3], key upcoming milestones include:

- Final approval of the four-year Washington rate plan expected during calendar year 2026 will set allowed returns and revenue targets critical for near-term financial stability [N13].

- Ongoing capital spending programs aimed at grid reliability enhancements continue through at least FY2028 based on disclosed investment schedules totaling approximately $63 million for AEL&P alone over three years—a proxy for broader ongoing spend [S1].

- Monitoring regulatory developments around decarbonization mandates will impact future capital allocation priorities.

Analysts should track quarterly earnings releases for updates on these milestones alongside regulatory commission publications outlining any modifications or disputes regarding rate filings.

Returns & Capital Allocation

Avista generates an approximate return on equity near 7.1%, calculated as fiscal year-end net income divided by shareholder equity of roughly $2.71 billion at December 31, 2025 [F1]. The steady dividend program remains a key component of capital allocation priorities with a payout nearing $159 million during FY2025 representing about an estimated payout ratio consistent with industry-regulated peers [F1].

Free cash flow was negative approximately $101 million last year given large investments relative to operating cash flows—typical of utilities undergoing modernization cycles [F1]. Avista relies on access to capital markets which remains supported by its investment grade credit ratings (BBB / Baa2) secured through prudent leverage controls—in particular keeping consolidated debt-to-capitalization under targeted thresholds mandated under credit facility covenants [S1]/[S4]/[S5]. In July of last year, the firm executed a $120 million private placement of first mortgage bonds at a fixed coupon of about 6.18% maturing in 2055 used to refinance short-term debt thereby smoothing maturity profiles [S9]/[S13].

Liquidity management encompasses committed revolving credit facilities totaling $500 million expiring mid-2029 providing buffer against working capital fluctuations particularly related to energy commodity price volatility exposures [S15]/[S17]. Letters of credit outstanding are moderate around low double-digit millions reflecting normal collateral requirements tied to energy contracts.

Industry Context & Competitive Moat

Avista operates effectively as a natural monopoly within its service regions where competition is generally limited due to infrastructure scale requirements and regulatory protections that grant exclusivity subject to public oversight [S1]/[S29]. The company's competitive moat stems from established long-term relationships with commissions allowing stable cost recovery frameworks plus integrated resource planning that addresses both supply reliability and compliance challenges proactively.

Participation in regional markets such as the Western EIM helps optimize generation dispatching across balancing authorities reducing exposure to costly emergency procurement while enhancing grid efficiency [S1]. Meanwhile evolving policy landscapes around renewable portfolio standards require capital outlays but also open opportunities for Avista to invest strategically in cleaner generation assets securing future rate base growth.

Risks Overview

Principal risks hinge on regulatory dependencies requiring timely approval of rates so that invested capital earns authorized returns without significant lag or disallowance which could compress earnings [S26]/[N13]. Operational risks include potential disruption from climate-related events necessitating unplanned repair expenses beyond regulated recovery mechanisms. The company also faces commodity price volatility risks mitigated partially via hedging arrangements but which can impact working capital demands including collateral postings [S14]/[S17]. Credit rating downgrades would materially increase borrowing costs impairing financial flexibility.

Conclusion & What To Watch

Avista's near-term trajectory is anchored by a recently filed multiyear rate plan designed to deliver steady earnings growth funded by continued high levels of capital expenditure focused on sustaining an aging utility infrastructure amid accelerating environmental mandates. Monitoring regulatory outcomes related to this rate plan will be critical alongside tracking execution against planned capex programs given implications for liquidity and free cash flow generation. Detail attention is warranted on how Avista manages emerging climate-related operational dynamics while preserving its investment grade credit profile supporting access to low-cost financing. Ultimately the company’s regulated utility model provides reasonably predictable revenues underpinned by natural monopoly advantages albeit shaped intricately by regulatory processes inherent to this sector.

This report summarizes publicly available information without providing investment advice or recommendations regarding securities transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments