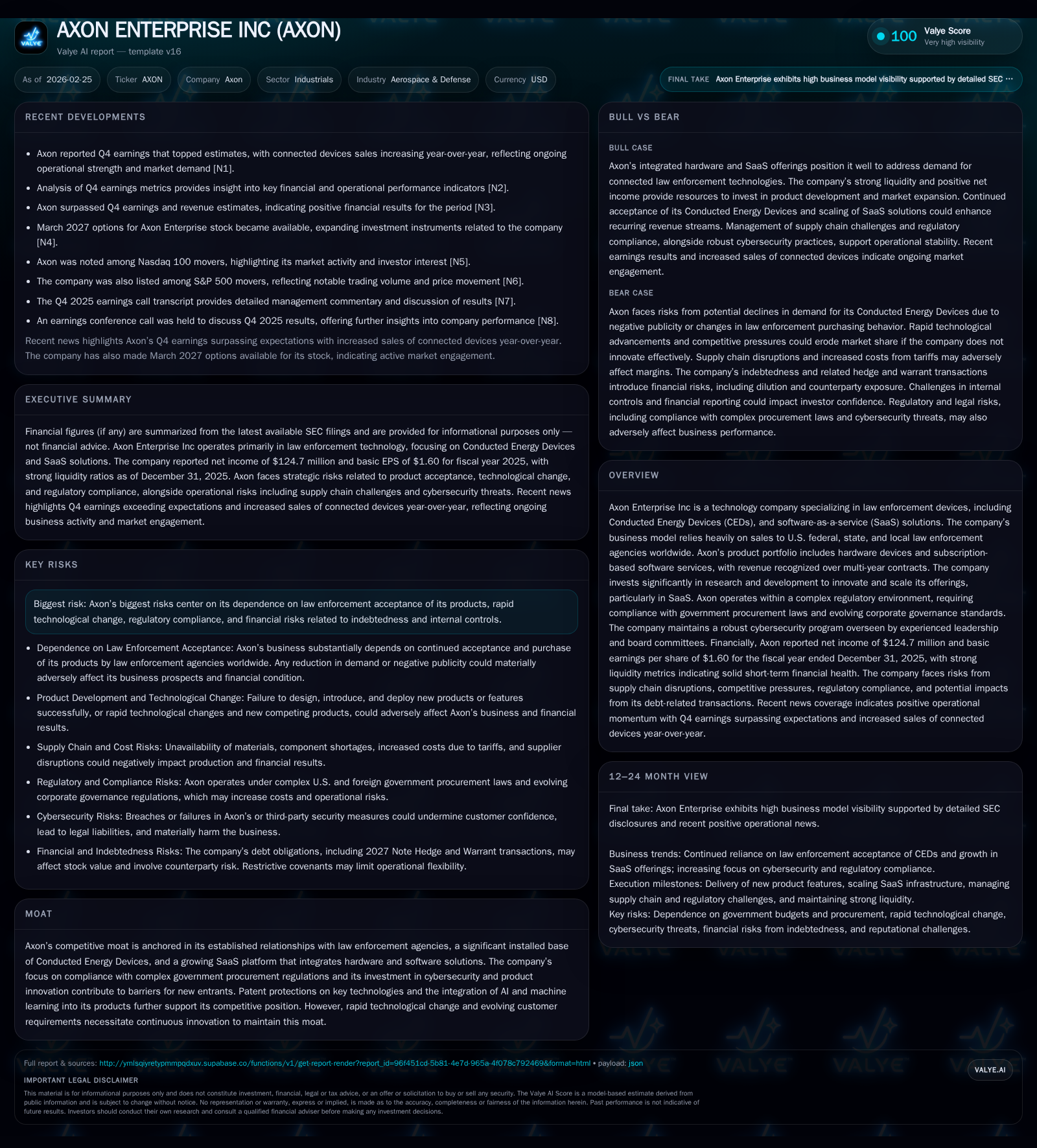

Axon Enterprise's Revenue Mix Tests Growth amid Product Cycle Fluctuations

Operating margin pressures and SaaS transition highlight crucial tradeoffs in Axon’s evolving law enforcement technology business.

Axon Enterprise's fiscal 2025 results reveal a sharp decline in operating income alongside sustained net income and robust operating cash flow, underscoring the company's strategic shift from hardware dependence toward recurring SaaS revenues. The firm's emphasis on multi-year contracts, substantial R&D investments, and compliance with complex government procurement regulations reflects a balancing act between near-term profitability challenges and long-term growth potential. Investors should closely monitor subscription renewal rates, connected device sales trends, and regulatory developments as key indicators of future performance.

Recap of Historical Financial Performance and Operating Drivers

Axon Enterprise’s fiscal 2025 results present a complex financial picture marked by a steep drop in operating income alongside solid net profitability and cash generation. Operating income fell from a positive $58.5 million in 2024 to an operating loss of $62.1 million in 2025—a negative 206% year-over-year change [F1]. This reflects significant upfront investments into research and development as well as the delayed revenue recognition characteristic of SaaS multi-year contracts.

Net income remained positive at $124.7 million for FY2025 but declined by 66.9% compared to $377 million in the prior year [F1]. This divergence stems largely from non-cash factors such as deferred revenue amortization typical of subscription models, tax effects, and other adjustments discussed in earnings communications [N2][S3]. Notably, operating cash flow stayed robust at $211.3 million despite a 48.2% decrease year-over-year, signaling strong underlying cash conversion even during compressed reported margins [F1].

Capital expenditures increased sharply by 72.9% to $136.3 million, driven by investments in expanding product offerings and scaling cloud infrastructure to support SaaS delivery [F1]. The elevated capex during margin pressure underscores Axon's focus on technological innovation over short-term profitability.

The balance sheet remains healthy with over $1.2 billion in cash and equivalents and a current ratio of approximately 2.53x, indicating solid liquidity coverage against current liabilities [F1]. Shareholders’ equity increased significantly to $3.24 billion reflecting retained earnings accumulation without reliance on external financing [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 125 | 211 | -62 | 136 | -66.9% |

| 2024 | 377 | 408 | 59 | 79 | +116.4% |

| 2023 | 174 | 189 | 155 | 60 | +18.4% |

| 2022 | 147 | 235 | 93 | 56 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 75 | 3.8 |

| 2024 | 330 | 16.2 |

| 2023 | 130 | 10.8 |

| 2022 | 180 | 11.6 |

Source: SEC companyfacts cache [F1].

Note: Revenue data not available from provided XBRL tags; recent dividends and share repurchases are not reported.

Evolving Product Portfolio: Hardware Challenges vs SaaS Growth

Axon operates at the intersection of tangible law enforcement hardware—primarily Conducted Energy Devices (CEDs)—and an expanding software platform delivered via subscription-based SaaS models . Traditionally reliant on hardware sales recognized mostly upon shipment, Axon’s shift towards multi-year subscription contracts leads to front-loaded expenses with ratable revenue recognition over contract duration.

The strategy involves bundling CEDs with cloud-based evidence management systems and officer safety software through subscription agreements aligned with municipal budgeting processes [N2][S15]. While this fosters customer retention via ecosystem lock-in effects, hardware sales face headwinds from governmental budget cycles and public scrutiny regarding CED use policies.

Recent quarters have seen connected device unit sales rise year-over-year but with expected fluctuations due to procurement lags intersecting political debates about law enforcement tools usage [N2]. Expanding direct sales channels and distributor networks remains challenging given the heterogeneous nature of global law enforcement agencies [S2].

Recurring subscription revenues trail initial contract signing due to ratable billing structures—a factor that depresses near-term earnings visibility but enhances long-term cash flow stability when effectively executed.

Regulatory Environment and Government Contracting Impacting Demand

Axon’s core customer base includes U.S. federal, state, local government agencies as well as international jurisdictions subject to complex procurement rules governed primarily by the Federal Acquisition Regulation (FAR) alongside local equivalents [S1][S6][S7]. Compliance requires detailed contract administration, reporting standards adherence, anti-corruption certifications, and other regulatory controls.

Recent executive orders aiming to streamline procurement while enforcing cost controls on defense acquisitions heighten cancellation risk for some programs where Axon is a vendor [S7]. Several major government contracts flagged for budget overruns or schedule delays exceeding thresholds face potential partial or full termination—posing tangible downside risk.

Evolving legislative scrutiny around ESG disclosures adds operational cost burdens related to governance oversight amidst politically sensitive policing technology debates today [S5][S11]. Municipal funding cycles impose budgetary constraints that may delay deal closings or renewals cyclically within fiscal periods.

R&D Investment and Technological Innovation Trends

R&D spending surged nearly three-quarters in FY2025 to approximately $136 million as Axon intensifies focus on integrating AI/ML capabilities within evidence management workflows and body camera analytics platforms [F1].

This investment supports longer product development cycles with rigorous validation ensuring compliance with public safety standards while addressing cybersecurity threats intrinsic to cloud services architectures . Although R&D costs weigh on near-term operating margins, they underpin a competitive moat based on proprietary algorithms and patented sensor fusion techniques.

Competitive pressures include rapid AI development among rivals that may erode feature differentiation if prematurely launched or inadequately tested—raising reputational risks plus possible IP litigation exposures impacting end users.

Capital Allocation Metrics, Cash Flow Generation, and Returns Analysis

Axon currently prioritizes reinvestment over shareholder distributions; there are no recent dividends or share repurchases reported while shareholders’ equity has markedly increased driven by retained earnings accumulation [F1].

Free cash flow approximated $75 million (operating cash flow minus capital expenditures) indicating moderate capital intensity relative to peers though ongoing investments constrain current profitability levels.

Return on equity stands near 3.8%, subdued primarily due to operating losses incurred during this development phase rather than weak top-line growth alone [F1]. Financial flexibility is maintained under existing debt covenants enforced through restrictive credit facilities designed for operational stability but limiting leverage capacity for rapid strategic initiatives.

Risks: Market Acceptance, Competitive Pressures, and Regulatory Compliance

Axon's business model depends heavily on continued law enforcement acceptance of its core CED technology—exposing it to concentrated strategic risk whereby shifts in policy sentiment or negative publicity could reduce demand or cause contract non-renewals [S1][S4][S8]. Product liability litigation remains a persistent risk given contentious CED usage; adverse rulings or settlements could bring substantial unplanned costs.

The intellectual property landscape presents ongoing litigation risks especially as AI-driven tools augment traditional offerings; protecting proprietary technologies is critical lest competitors infringe or displace key features without recourse eroding market position [S4][S20]. Cybersecurity vulnerabilities inherent in cloud-hosted evidence management services raise liability concerns should data breaches occur causing loss of customer trust or regulatory penalties.

Government procurement cycle unpredictability driven by budget delays adds operational risk contributing to fluctuating revenue flows challenging short-term forecasting accuracy amid extended public sector sales cycles.

Outlook Considerations: Milestones and What Investors Should Monitor

No explicit forward guidance is publicly available; investors should track leading indicators such as growth rates in connected device shipments and SaaS subscription renewal metrics which serve as bellwethers for organic traction gains within constrained municipal budgets [N2][N3].

Additionally important are updates regarding ongoing federal reviews of major defense programs which may rapidly alter contractual landscapes affecting Axon's large account exposures [S7][N4]. Regulatory changes including EU AI Act compliance may impact product deployment timelines or adoption internationally.

Options market activity signaling increased interest around March 2027 maturities may reflect investor focus on upcoming milestones or regulatory developments impacting valuation volatility [N9]. Litigation developments related to product liability suits also bear directly on Axon's reputation-sensitive positioning within law enforcement circles.

Disclaimer: This analysis is based solely on publicly available documents up to February 25, 2026. It does not constitute investment advice or recommendations regarding AXON securities or strategies.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments