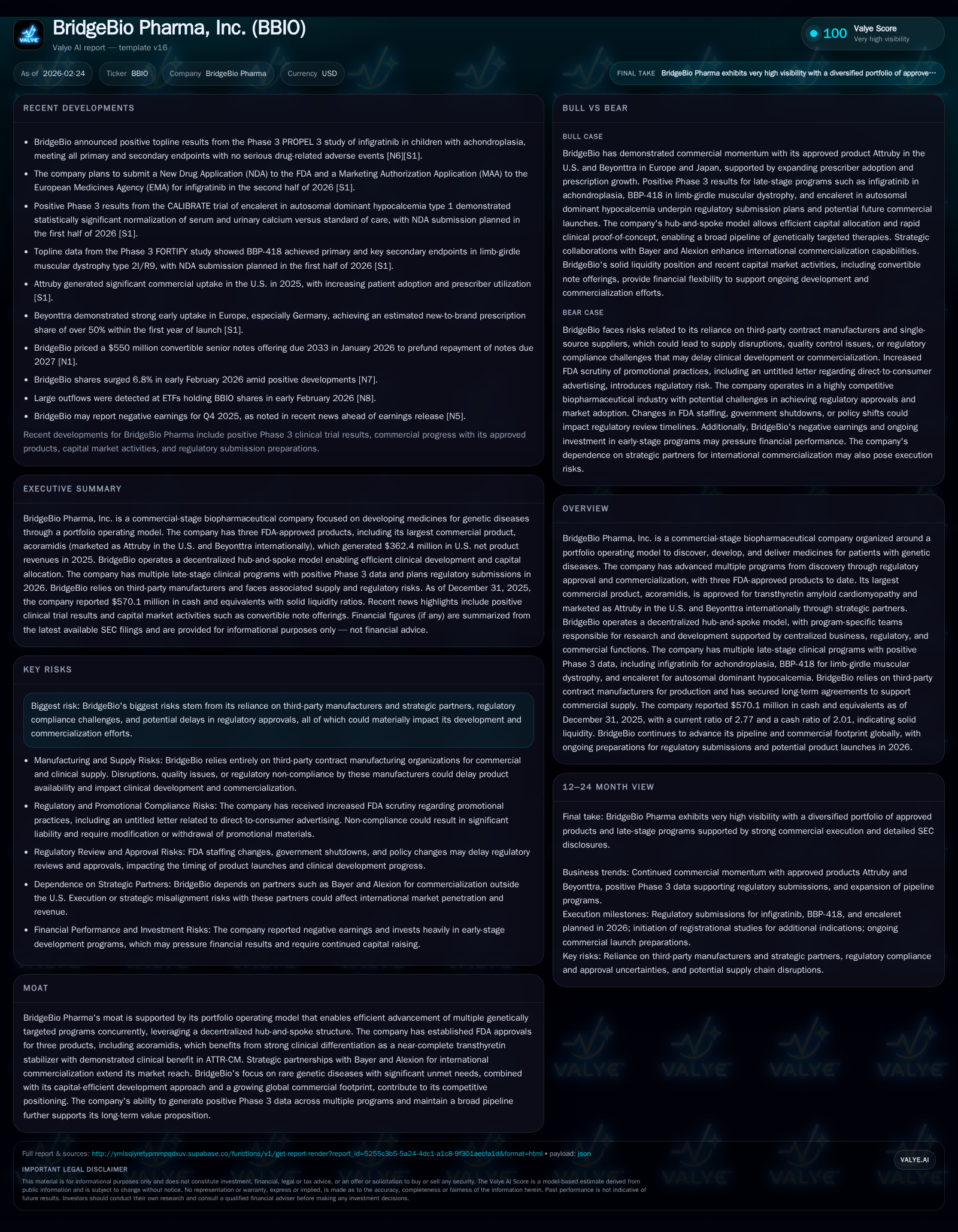

BridgeBio Pharma’s Portfolio Model and Late-Stage Pipeline Drive Commercial Momentum Despite Operating Losses

BridgeBio advances multiple genetic disease programs with growing commercial sales from its lead product Attruby amid elevated development costs and regulatory scrutiny.

BridgeBio Pharma, Inc. operates as a commercial-stage biopharma company focused on genetic diseases, leveraging a portfolio operating model to efficiently advance numerous drug candidates. Its flagship approved therapy acoramidis (Attruby) has gained U.S. FDA approval and is marketed domestically and internationally through strategic partnerships, contributing to growing commercial traction. The company continues to push late-stage clinical assets, particularly in achondroplasia, limb-girdle muscular dystrophy, and autosomal dominant hypocalcemia, with positive Phase 3 readouts supporting upcoming regulatory submissions. However, BridgeBio’s historical financials reveal sustained operating losses and negative cash flows driven by high R&D and SG&A expenses, reflecting its growth investments amid a complex regulatory landscape. Capital structure includes convertible senior notes and royalty agreements linked to acoramidis sales, with active share repurchases suggesting management confidence. Going forward, key milestones include regulatory filings and market adoption of pipeline therapies, while risks center on manufacturing reliance and promotional compliance.

Company Overview

Historical performance (annual)

| FY | CFO ($mm) | OpInc ($mm) | Capex ($mm) |

|---|---|---|---|

| 2025 | -446 | -523 | 1 |

| 2024 | -521 | -593 | 1 |

| 2023 | -528 | -607 | 1 |

| 2022 | -419 | -512 | 5 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Net, Div, ROE%. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) |

|---|---|---|

| 2025 | 48 | -447 |

| 2024 | -522 | |

| 2023 | 0 | -529 |

| 2022 | 0 | -424 |

Source: SEC companyfacts cache [F1].

BridgeBio Pharma, Inc. is positioned as a commercial-stage biopharmaceutical company uniquely organized around a portfolio operating model concentrated on genetic diseases. Founded roughly a decade ago, the firm has scaled from discovery to regulatory approval across several programs, culminating in three FDA-approved therapeutic products that have collectively treated over 8,500 patients. The hallmark of its business structure consists of decentralized program-specific teams responsible for development activities backed by centralized regulatory, commercial, and corporate functions — a design aimed at efficiency and speed along the drug development continuum [S1].

Of these approvals, acoramidis (marketed as Attruby™ in the U.S.) stands out as BridgeBio’s largest revenue-generating product targeting transthyretin amyloid cardiomyopathy (ATTR-CM). Approved by the FDA in late 2024, this near-complete stabilizer of transthyretin exhibits clinical differentiation with proven patient benefit. For markets outside the U.S., BridgeBio leverages strategic partnerships: Bayer handles European commercialization under the brand Beyonttra™, while Alexion oversees Japan alongside selective regional direct commercialization efforts by BridgeBio itself [S1].

Historical Performance and Financials

BridgeBio's financial trajectory reflects significant investments underpinning pipeline growth and commercial expansion efforts.

| Fiscal Year | Operating Income (USD M) | YoY Change (%) | Operating Cash Flow (USD M) | YoY Change (%) | Capital Expenditures (USD M) | YoY Change (%) | Stockholders’ Equity (USD M) | Share Repurchases (USD M) |

|---|---|---|---|---|---|---|---|---|

| 2025 | -523 | +11.7 | -446 | +14.4 | 1.10 | +17.6 | -2087 | 48 |

| 2024 | -593 | -2.3 | -521 | -1.3 | 0.93 | -28.5 | -1468 | 0 |

| 2023 | -607 | +18.6 | -528 | +25.9 | 1.30 | -73 | -1354 | 0 |

| 2022 | -512 | N/A | -419 | N/A | 4.82 | N/A | -1255 | 0 |

Note: Revenue data is not available from provided tags.

Operating losses remain significant but showed improvement in 2025 compared to prior years, narrowing to approximately $523 million versus nearly $593 million in FY24 [F1]. This improvement partly reflects early revenues from Attruby alongside controlled operating expenses despite substantial R&D spending.

Operating cash flows continue to be negative (-$446 million in FY25), consistent with loss generation and reflecting ongoing clinical trial investments [F1]. Capital expenditures remain minimal (~$1M annually), indicating limited physical asset expansion relative to operational spending.

The company's shareholders’ equity remains deeply negative (around -$2 billion at end-2025), indicating accumulated losses exceeding invested capital since inception [F1]. Net income beyond mid-2019 is not available from provided tags; thus, meaningful calculation of ROE is not feasible.

BridgeBio has not paid dividends recently; the most recent dividend data point dates back to FY2019 [F1]. Share repurchases resumed significantly in FY25 with approximately $48 million spent after no repurchases during FY23 or FY24 except historical activity in FY21, possibly signaling management’s intent to support shareholder value amid continued losses.

Growth Drivers and Pipeline Catalysts

Future growth relies heavily on:

Attruby Expansion: Following FDA approval in November 2024 for ATTR-CM indication, BridgeBio markets Attruby domestically while leveraging Bayer (Europe) and Alexion (Japan) partnerships internationally—providing expanding commercial reach backed by royalty arrangements supporting capital inflows tied directly to sales performance [S1].

Late-Stage Clinical Progress: Positive Phase 3 data have been reported for multiple candidates poised to broaden BridgeBio's portfolio:

- Infigratinib achieved primary endpoints in achondroplasia trials [N6], setting groundwork for regulatory submissions.

- BBP-418 targeting limb-girdle muscular dystrophy type 2I/R9 reported encouraging Phase 3 results enhancing filing prospects.

- Encaleret for autosomal dominant hypocalcemia type 1 advanced positively through pivotal trials supporting potential first-in-class status.

These developments highlight BridgeBio’s efficient platform approach enabling concurrent program advancement at relatively low per-program investment levels (<$40M to proof-of-concept) [S1].

Regulatory Environment and Risks

Risks include:

FDA Advertising Scrutiny: Since September 2025 increased FDA focus on pharmaceutical advertising led to an untitled letter issued to BridgeBio regarding Attruby's direct-to-consumer marketing campaigns [S12][N4], underscoring compliance challenges that may require marketing adjustments.

Manufacturing Dependencies: Reliance on third-party contract manufacturers for active pharmaceutical ingredients (APIs), packaging, and distribution outside the U.S., including German CMOs supporting European operations under Bayer collaboration introduces supply chain risks subject to regulatory inspections and quality control challenges [S22].

Healthcare Laws & Pricing Pressure: Federal laws such as Anti-Kickback Statutes, False Claims Act enforcement risks, evolving pricing reforms including Medicare negotiation provisions present ongoing uncertainties impacting future reimbursement levels and revenue potential [S23][S24].

Capital Structure & Liquidity Profile

BridgeBio’s capital structure combines equity financing with significant debt instruments:

In January 2026, BridgeBio issued approximately $550 million convertible senior notes due in 2033 bearing a coupon of approximately 0.75%, intended for refinancing earlier maturities and enhancing liquidity flexibility [N13][S16].

Earlier issuance includes $632.5 million senior unsecured notes due in 2031 with conversion options supporting balanced capital optimization [S19][S21].

Royalty monetization agreements provide upfront non-dilutive capital tied to acoramidis sales royalties capped at $950 million total payments protecting investors while funding operations [S21].

As of December 31, 2025, cash and cash equivalents stood at approximately $570 million against current liabilities of about $288 million yielding a current ratio near ~2.77—a healthy liquidity position supportive of ongoing operations despite significant cash burn [F1].

Outlook & Key Considerations

While explicit forward guidance is not provided within available disclosures, key factors shaping near-term outlook include:

- Timing and success of regulatory filings based on recent Phase 3 trial data;

- Commercial ramp-up trajectory for Attruby amid competitive pricing pressures;

- Management’s capital allocation strategy balancing continued pipeline investment against shareholder returns such as buybacks;

- Operational risk management around manufacturing compliance essential for uninterrupted supply;

- Monitoring regulatory developments related to promotional conduct given recent FDA scrutiny.

These elements will influence the path toward sustainable profitability alongside revenue growth prospects.

Conclusion: Strategic Positioning Amid Investment Cycle

BridgeBio Pharma exemplifies a biopharmaceutical entity embracing portfolio diversification centered on rare genetic disorders—a niche demanding specialized scientific expertise combined with operational agility enabled by its decentralized 'hub-and-spoke' model.

Anchored commercially by successful launch of Attruby complemented by promising late-stage candidates,[N6][S1] BridgeBio confronts a transition from sustained net losses fueled by R&D investments but supported by robust liquidity and flexible capital structures designed to underpin execution across global markets.

Regulatory risks related to promotional compliance alongside manufacturing dependencies underscore operational complexities requiring vigilant oversight consistent with industry standards.[S12][S22]

Notably, resumption of share repurchases amidst negative equity highlights management confidence aiming to enhance intrinsic shareholder value even amid developmental uncertainties.[F1]

Disclaimer: This analysis reflects publicly available information from SEC filings, news releases, and third-party sources cited herein without extrapolating missing financial metrics such as revenue or recent net income beyond provided data points.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments