Bloom Energy's Innovation and Financial Dynamics Amid Accelerating Clean Energy Demand

Bloom Energy balances groundbreaking fuel cell technology with ongoing profitability challenges in a rapidly evolving energy market.

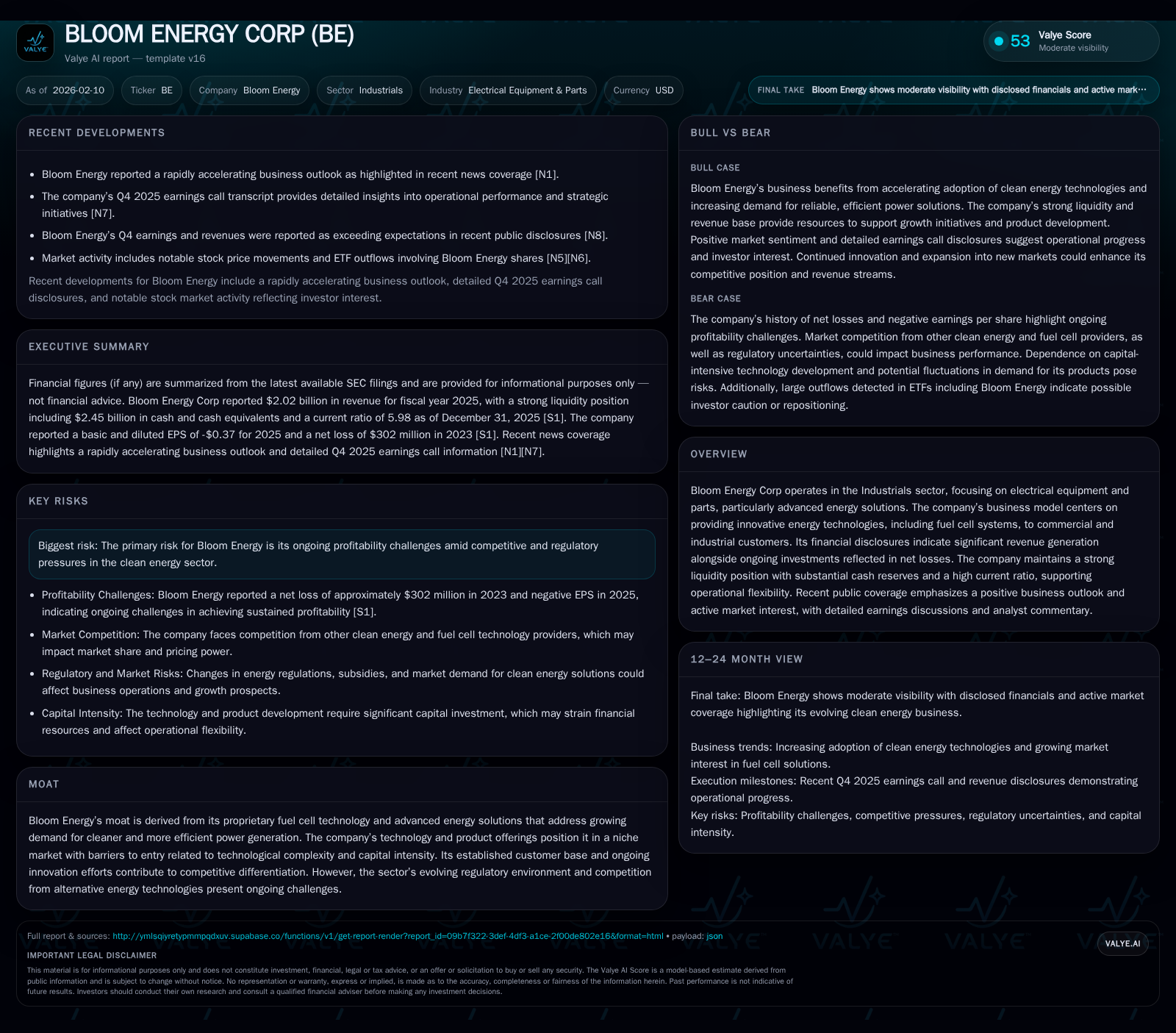

Bloom Energy Corp has exhibited robust top-line growth and innovation leadership through its proprietary fuel cell systems, fueling investor enthusiasm following its Q4 2025 earnings beat. Despite strong liquidity and a solid current ratio near 6.0, the company continues to face significant net losses as it invests heavily in technology and scaling operations. Market sentiment reflects optimism tempered by concerns over competition and regulatory uncertainty. Moving into 2026, Bloom Energy’s trajectory will hinge on its ability to convert technological promise into sustainable financial performance amid an evolving clean energy landscape.

Powering Forward: Bloom Energy's Strategic Momentum

Bloom Energy Corp operates at the confluence of innovation and sustainability within the Industrials sector, carving out a niche centered on advanced electrical equipment solutions that leverage proprietary fuel cell systems. Positioned as a technology-driven energy pioneer, Bloom’s mission aligns with growing commercial and industrial demand for cleaner and more efficient power generation options. The company's strategic momentum is anchored in its ability to translate cutting-edge science into deployed systems that respond to emergent energy demands while navigating complex market forces [valye_report_excerpt].

Its business model hinges on delivering tailored energy solutions that offer both environmental benefits and operational reliability—factors increasingly pivotal as companies seek to decarbonize operations without sacrificing performance. This unique focal point differentiates Bloom within the electrical equipment industry, especially as the global transition toward low-carbon technologies accelerates.

Decoding the Q4 2025 Earnings Beat and Market Reaction

The market’s enthusiastic response following Bloom Energy’s Q4 2025 results underscores the bullish sentiment around its growth trajectory. Revenues reported at $2.02 billion for calendar year 2025 notably exceeded analyst estimates [F1], igniting a swift after-hours rally where the stock price surged significantly [N11][N14]. Investors embraced the strong top-line performance as validation of accelerating customer adoption across commercial and industrial segments.

During the earnings call, management emphasized improving unit economics alongside expanding backlog visibility—a narrative that was well-received by market participants [N2]. The enthusiastic trading flows in subsequent sessions reflected this confluence of positive operational execution signals merging with broader energy transition tailwinds. Nonetheless, scrutiny remains over profit conversion given persistent net losses visible in recent financial disclosures.

The Technology Moat: Proprietary Fuel Cells in a Competitive Arena

Bloom Energy’s technological fortress rests on its proprietary fuel cell platform—a complex synthesis of materials science, engineering precision, and scalable manufacturing expertise. This moat affords barriers against new entrants due to substantial capital requirements and steep learning curves required to replicate such sophisticated systems [valye_report_excerpt.moat].

In an arena crowded with alternative green energy technologies—ranging from battery storage to hydrogen electrolyzers—Bloom’s fuel cells occupy a distinct segment characterized not just by innovation but also critical reliability suited for continuous power needs. While competition intensifies with emerging substitutes vying for market share, Bloom’s established customer relationships and ongoing investment into next-generation improvements reinforce its differentiation.

The company’s strategy appears to leverage this innovation pipeline as a shield while seeking economies of scale that can progressively improve cost structures—a high-stakes balancing act essential for maintaining competitive standing.

Financial Foundations: Cash Reserves, Losses, and Liquidity Dynamics

Scrutinizing Bloom’s financial architecture reveals a juxtaposition between impressive liquidity metrics and sustained negative profitability dynamics. As of year-end 2025, cash and cash equivalents stood at approximately $2.45 billion accompanied by current assets totaling $3.73 billion against current liabilities near $624 million—yielding a robust current ratio of about 6x [F1]. This suggests admirable operational flexibility that can support continued investments essential for scaling.

However, this solidity contrasts with ongoing net income losses; the reported net loss figure extends beyond $300 million as per latest filings [F1]. Such losses predominantly reflect substantial expenses linked to research & development efforts, production scale-up costs, and high fixed overheads common in pioneering technology businesses [S1][S2].

The sustainability question centers on how effectively Bloom can leverage these cash reserves while progressing toward profitability thresholds amidst an aggressive innovation agenda.

Market Sentiment and Analyst Voices: Navigating Optimism and Risk

The recent Nasdaq coverage charts an optimistic yet measured landscape. Headlines like "Bloom Energy Blossoms on Rapidly Accelerating Outlook" capture investor excitement grounded in expansion prospects while simultaneously highlighting prudential viewpoints regarding sector risks [N8]. Analysts preparing for key metric revelations ahead of earnings underscored expectations for continued revenue acceleration tempered by scrutiny over margin improvements [N6].

Analyst discussions increasingly consider external shifts such as AI-driven industrial applications potentially favoring select energy tech winners—a dynamic that could redirect sector leadership profiles this year [N7]. Meanwhile, large ETF outflows detected in some energy-related vehicles signal cautious risk recalibration among investors wary of valuation extremes or regulatory headwinds [N10]. Collectively, these voices weave an intricate mood: constructive enthusiasm restrained by realistic caution.

Regulatory Landscape Impacting Growth Prospects

Embedded within the broader narrative is the influential backdrop of an evolving regulatory environment shaping clean energy viability. Incentive programs designed to foster green technology deployment stand alongside stringent compliance requirements—creating both opportunity windows and unpredictability channels [valye_report_excerpt.moat].

Policy frameworks around emissions standards, renewable portfolio mandates, and subsidy regimes directly affect project economics central to Bloom’s prospects. Fluctuations or delays in these policies could modulate revenue visibility or necessitate strategic pivots. Conversely, favorable regulation could accelerate adoption curves but may come with intricate reporting or operational conditions that increase indirect costs.

Navigating this regulatory terrain requires tactical agility reflective in both technological adaptations and financial planning.

Balancing Bold Innovation Against Profitability Headwinds

Bloom Energy confronts a classic growth paradox: substantial investments catalyze competitive positioning yet perpetuate near-term profitability challenges [valye_report_excerpt.risks]. The ongoing accumulation of net losses underlines tension between nurturing ambitious R&D pipelines and achieving scalable manufacturing efficiencies necessary for cost reduction [S1][S2].

This dilemma embodies a critical inflection point whether high upfront capital outlays will yield long-term sustainable returns or create persistent margin pressure demanding reassessment of resource allocations. Stakeholders are keenly focused on indicators such as operating leverage improvement trajectories, gross margin enhancements, or shifts towards higher-margin service revenues.

The company's approach to balancing these conflicting pressures will likely shape investor confidence going forward.

Positioning Into 2026: Catalysts and Caution Points

Looking ahead, Bloom Energy’s path is poised between accelerating opportunity sets and looming execution risks. Key catalysts include successful commercialization of next-gen products capable of outperforming incumbents on cost/performance metrics; expansion into new geographies or industry verticals; and constructive regulatory developments providing clearer subsidy visibility or carbon pricing mechanisms [N8][F1][valye_report_excerpt].

Nonetheless, caution remains warranted given ongoing net losses challenging balance sheet endurance over extended horizons without clear break-even milestones. Macro uncertainties—including raw material supply chain constraints or competitor technological leaps—also carry contingency importance.

Ultimately, Bloom's trajectory embodies both promise rooted in proprietary technology leadership coupled with prudent acknowledgment of critical profitability imperatives as it strides into a dynamic clean-energy epoch.

This report is intended for informational purposes only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments