Mobile Infrastructure Corp Battles Concentration Risks and Debt Maturities in Pursuit of Profitability

Mobile Infrastructure Corp contends with operator concentration, legacy losses, and looming debt expiration as it aims to stabilize financial health.

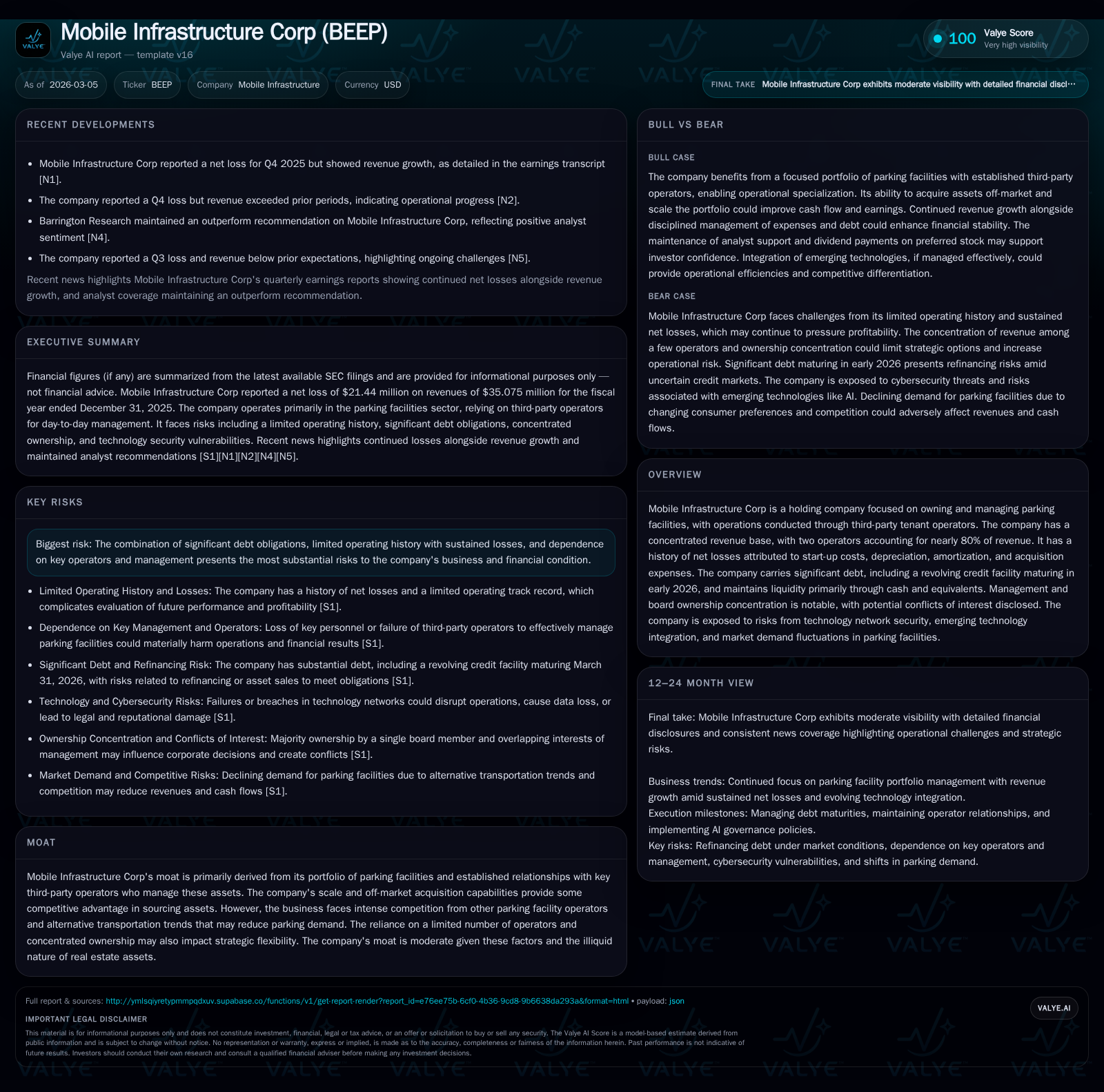

Mobile Infrastructure Corp's business model centers on owning parking facilities operated by a limited number of third-party tenants, exposing it to significant concentration risks. The firm’s historical financial performance reflects recurring net losses driven by start-up costs and acquisition expenses, despite some improvement in operating cash flow in 2025. A critical near-term challenge is the March 31, 2026 maturity of its $25.9 million revolving credit facility, requiring refinancing or asset sales under tight covenant restrictions. Additional risks stem from evolving technology impacts on parking demand and concentrated insider ownership affecting governance and strategic flexibility. Capital allocation has focused on modest share repurchases amid negative returns on equity. Going forward, growth prospects remain constrained by structural dependencies and a narrow operational base.

Unpacking FY2025 Performance: Revenue Trends and Persistent Losses

Mobile Infrastructure Corp closed fiscal year 2025 with total revenues of approximately $35.1 million, reflecting a 5.2% decline from $37.0 million reported in 2024 [F1]. This decrease contrasts with the prior year's rebound from $30.3 million in 2023 but underscores lingering operational challenges. Operating income data is limited beyond the last disclosed figure of a negative $2.66 million in 2022 [F1], yet net income trends reveal persistent deepening losses: -$21.4 million in 2025 versus -$5.77 million in 2024 [F1]. The magnitude of these net losses owes primarily to non-cash charges including depreciation, amortization related to acquired properties, startup expenses, and acquisition-related costs documented in management commentary [N2][S8].

Importantly, despite ongoing net losses, Mobile Infrastructure managed to turn operating cash flow positive at $848,000 for FY2025 compared to prior periods marked by negative CFOs (e.g., -$784k in 2024) [F1]. Coupled with sharply reduced capital expenditures ($15,000 in FY2025 versus over half a million annually prior), this resulted in modest free cash flow generation near $833,000 [F1]. This divergence suggests that while earnings remain challenged by accounting charges, underlying cash operations are improving gradually but remain sensitive to contract performance.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 35 | -21 | 1 | 15000 | -5.2% | -271.9% |

| 2024 | 37 | -6 | -1 | 595000 | +22.3% | +77.1% |

| 2023 | 30 | -25 | -2 | 647000 | -9250.3% | |

| 2022 | 0 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 4 | 1 | -15.2 |

| 2024 | 1 | -1 | -3.4 |

| 2023 | -3 | -23.0 | |

| 2022 | -6.0 |

Source: SEC companyfacts cache [F1].

*Last available operating income figure from FY2022 [F1]. Note: Operating income for FY23-25 not explicitly reported.

Operator Dependency: The Double-Edged Sword of Concentrated Tenant Relationships

A salient feature of Mobile Infrastructure’s business is its reliance on third-party managers operating its owned parking facilities under contractual arrangements such as management contracts or lease-operator agreements [S9]. As of end-2025, two operators — Metropolis and LAZ — accounted for approximately 63% and nearly 17% of company revenue respectively, cumulatively near 80% concentration [S9]. This dependency creates heightened risk exposure; adverse developments affecting these two operators’ financial health or strategic priorities could materially impair Mobile Infrastructure’s revenues and cash flows.

The company’s model involves delegating day-to-day operational responsibilities to these tenants under structured agreements that stipulate performance objectives yet inherently limit direct control [S9][S18]. Should either operator fail to meet obligations or elect not to renew contracts on favorable terms, the firm may face operational disruptions or renegotiations entailing lower income streams or higher oversight costs.

Debt Maturity on Horizon: Liquidity, Covenants, and Refinancing Strategies

Mobile Infrastructure Corp confronts a formidable near-term liquidity challenge with its $25.9 million revolving credit facility reaching maturity on March 31, 2026 [S4][S13][S29]. The facility carries accrued interest of roughly $5.6 million due upon repayment [S5]. In parallel, substantial additional indebtedness includes a $75.1 million CMBS loan secured by seven subsidiaries and around $99.6 million in asset-backed notes tied to nineteen properties [S15][F1].

All debt agreements embed restrictive covenants limiting asset sales without consent, liens creation thresholds, investments conditions and debt incurrence caps that collectively constrain financial flexibility [S4][S6]. Failure to comply can prompt events of default potentially accelerating loan repayments or foreclosure rights against collateralized properties [S6][S15].

Management has publicly approved an asset sale plan intended to satisfy part of this impending debt obligation before maturity; however uncertainty remains whether asset dispositions or refinancing agreements—amid volatile commercial real estate financing markets—will materialize on acceptable terms or timing [N1][S13][S29]. The interplay between leveraged balance sheet structure and restrictive debt covenants requires vigilant monitoring over the next few months as outcomes will critically affect solvency.

Technology and Market Demand: Emerging Threats in Parking Facility Operations

Beyond traditional market risks associated with real estate ownership lies a layer of industry-specific technological disruption risks impacting Mobile Infrastructure Corp’s long-term viability [S7][S26]. The integration of emerging technologies such as AI introduces exposure to network security failures including malware threats or unauthorized data access that could impair operations or customer trust.

Concurrently, evolving urban mobility paradigms—including ride sharing proliferation (Uber/Lyft), carpooling incentives, autonomous vehicle adoption potential—and legislative responses promoting mass transit usage depress aggregate demand for parking assets in dense metropolitan areas where many properties reside [S7][S9]. Given the company’s narrow focus solely on parking properties—with no portfolio diversification into complementary real estate types—such secular shifts magnify downside pressure on utilization rates and pricing power.

Management Influence and Governance: Ownership Concentration Risks

Governance at Mobile Infrastructure features considerable insider control with Mr. Osher holding over a 50% voting stake directly or indirectly through affiliated vehicles as of December-end 2025 [S1][S23][N1]. Additionally, key executives including CEO Ms. Hogue and Executive Chairman Mr. Chavez maintain overlapping interests linked to other entities potentially creating conflicts that complicate transparent strategic decision-making.

This concentrated ownership structure categorizes Mobile Infrastructure as a "controlled company" under Nasdaq rules permitting certain corporate governance exemptions—potentially limiting independent oversight mechanisms customary among broadly held counterparts [S29],[N1]. Minority shareholders might therefore experience governance constraints influencing responsiveness to broad investor interests particularly amidst restructuring initiatives necessitated by financial pressures [S23].

Capital Allocation Patterns: Dividends, Buybacks, and Implications for Shareholders

Mobile Infrastructure Corporation has refrained from declaring dividends historically given recurring net losses; instead capital allocation focused predominantly on share repurchase programs albeit at modest absolute levels relative to equity base [$3.97 million buybacks executed during FY25 versus equity around $141 million] [F1][S25]. These repurchases signal management’s selective attempt at supporting per-share metrics amidst shrinking book value (ROE approximating -15% based on FY25 net loss over equity) but appear financially constrained by persistent earnings deficits.

Low capital expenditure outlays ($15k in FY25 versus mid-six figures prior years) reflect limited reinvestment into properties possibly indicative of capital preservation orientation pending clearer path toward profitability improvements [F1]. Such conservative capex stance aligns with the firm's efforts to stabilize cash flows ahead of debt maturities.

Looking Ahead: Growth Prospects Tempered by Structural Constraints

Explicit forward guidance remains limited post-Q4 FY25 reporting; however analysis suggests that growth opportunities are principally anchored on expanding the parking asset portfolio through selective off-market acquisitions should financing environments permit scaling [N1][S9]. The illiquid nature of commercial real estate assets coupled with market fragmentation limits rapid scalability.

Dependency on third-party operators further narrows operational expansion flexibility since each asset requires close coordination for performance enhancement plans confirming business model rigidity under current concentration dynamics [S9]. Furthermore, changing consumer tendencies toward alternative transportation modes underpin cautious growth outlook leading management focus toward optimizing existing portfolio yield rather than aggressive enlargement.

Key Milestones to Monitor: Refinancing, Portfolio Optimization, and Profitability Goals

The paramount event horizon centers on refinancing or repayment success for the revolver coming due late Q1/Q2 calendar year 2026 as failure risks precipitating defaults triggering collateral foreclosure processes [N1][S4][S13]. Asset disposition progress will be a barometer for deleveraging efficacy.

Parallel attentiveness is warranted toward updates regarding renewal terms on major operator contracts given their outsized revenue contributions influencing near-term cash flow sustainability.

Progress toward turning net profitability positive alongside sustained positive operating cash flow trends would constitute meaningful markers indicating potential inflection points if achieved within the next fiscal cycle.

This report synthesizes publicly filed documents alongside recent earnings disclosures up through early March 2026 reflecting Mobile Infrastructure Corp's financial health and strategic challenges without expressing investment opinion or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments