Biglari Holdings’ Strategic Battle with Profitability and Asset Value

Balancing operational gains at Steak n Shake with financial volatility and capital stewardship defines Biglari Holdings’ current chapter.

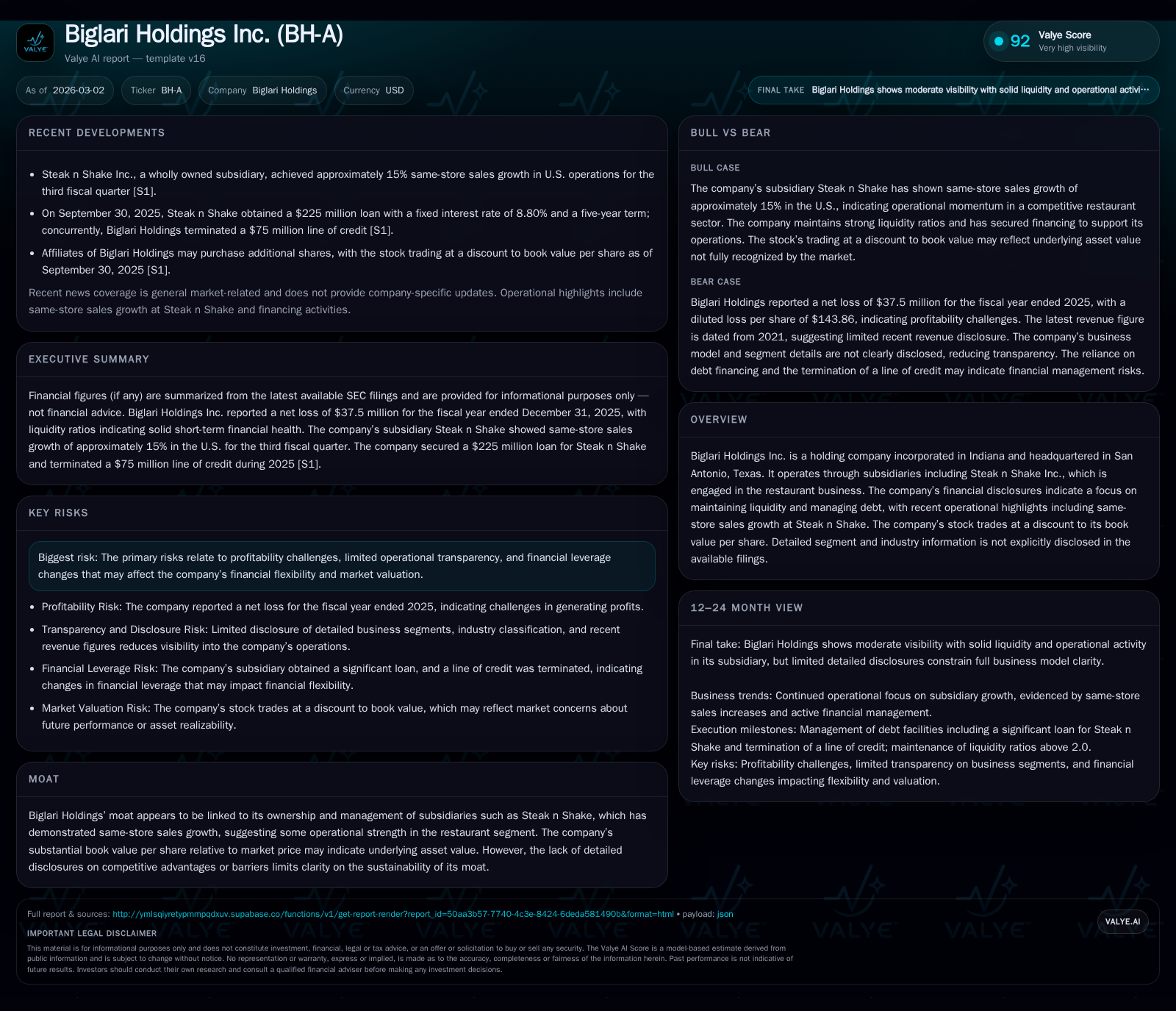

Biglari Holdings Inc.’s financial narrative over recent years reveals sharp revenue contractions contrasted by pockets of operational strength within its flagship restaurant subsidiary, Steak n Shake. Despite same-store sales momentum reported above 15%, the holding company endures significant net income volatility culminating in a heavy FY2025 loss, while operating cash flow remains robust. The capital structure features a notable $225 million subordinated loan taken by Steak n Shake at a high fixed interest rate, balanced against sizeable liquidity and equity capital. Investors reconcile the shares trading below book value amid profitability and transparency challenges, while future catalysts hinge on sustaining subsidiary growth and prudently managing leverage.

Operational Trajectory: Past Revenue and Profitability Trends

Biglari Holdings’ recent financial history is marked by pronounced revenue contraction alongside volatile profitability metrics. Examining annual data from FY2018 through FY2025 illustrates the trajectory: revenue decreased from roughly $195 million in FY2018 to just under $100 million by FY2020—a negative compound annual growth rate nearing 37% over those three years [F1]. This steep decline suggests prolonged challenges in maintaining top-line traction.

Profit volatility compounds this picture. Net income swung from losses of about -$32 million in FY2022 to a surprising profit of approximately $55 million in FY2023 before plunging again to a substantial loss near -$37.5 million in FY2025 [F1]. Such swings highlight discontinuities potentially linked to exceptional items, restructuring charges, or operational turnaround efforts but underscore inconsistency in earnings quality.

Operating cash flow trends tell a different story: after peaking at $127.8 million in FY2022, CFO dipped but then surged back to nearly $107 million by FY2025 despite net losses, indicating strong operational cash generation outside reported earnings [F1]. Capital expenditures have remained relatively stable around $25–30 million annually, implying steady reinvestment levels consonant with the company’s size and asset base.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -37 | 107 | 30 | -897.3% |

| 2024 | -4 | 50 | 31 | -106.8% |

| 2023 | 55 | 73 | 23 | +271.6% |

| 2022 | -32 | 128 | 30 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 77 | -7.2 |

| 2024 | 19 | -0.7 |

| 2023 | 50 | 9.2 |

| 2022 | 98 | -5.9 |

Source: SEC companyfacts cache [F1].

Note: Revenue series does not cover every year up to FY2025; net income, CFO, capex and equity for recent years are highlighted.

Key takeaway: Biglari Holdings exhibits severe revenue shrinkage historically while experiencing punctuated swings in net profits offset by solid operational cash flow resilience.

Levers Behind Same-Store Sales Progress at Steak n Shake

Within this mixed performance context, Biglari’s wholly owned subsidiary Steak n Shake emerges as a bright spot operationally. Recent disclosures indicate that for both company-operated and franchise partner stores across the U.S., same-store sales have grown over 15%, particularly noted in Q3 and Q4 of fiscal year 2025 [S21][S14]. This is notable within the broader restaurant industry where same-store sales growth is often a key barometer for customer retention and menu innovation success.

Steak n Shake’s role is pivotal: though the parent company grapples with wider revenue contractions and net losses, strong same-store sales momentum evidences improved operational execution possibly through optimized menu offerings or marketing tactics tailored to regional demand trends.

However, detailed material disclosures about Steak n Shake’s segment contribution or margins remain scant . Therefore, while sales progression offers some moat credibility through brand strength or competitive positioning within mid-tier casual dining, it does not fully illuminate scalable profitability or expansion runway.

Key takeaway: Steak n Shake boosts Biglari's profile via healthy comparable store growth but lacks transparent reporting on profitability drivers restricting comprehensive moat evaluation.

Recent Financial Performance: Swings in Net Income and Cash Flows

Fiscal year ended December 31, 2025 saw a puzzling divergence between Biglari Holdings’ profitability and cash generation metrics [F1][S3]. While net income plunged into a loss of nearly $38 million from a modest prior-year loss, operating cash flow more than doubled compared to FY2024 levels—climbing to nearly $107 million.

Such disjointed results frequently suggest significant non-cash adjustments such as impairment charges, restructuring provisions, or varying working capital movements that depress accounting earnings but preserve underlying cash flows favored by lenders or investors focused on liquidity.

Indeed, the disparity underscores nuances when valuing holding companies with embedded subsidiaries facing turnaround phases: profit figures may mask underlying business viability supported by tangible cash flow sustenance.

Key takeaway: Despite headline net losses signaling distress, Biglari’s operating cash flow strength indicates foundational business activity remains solidly cash-generative.

Debt Profile and Liquidity Management: The Role of $225 Million Subsidiary Loan

In late September 2025, Steak n Shake secured a sizable loan facility amounting to $225 million carrying an unusually high fixed interest rate of 8.8%, with scheduled amortization starting immediately at an annual rate of roughly 3% [S8]. Simultaneously, Biglari Holdings terminated its $75 million line of credit marking a shift directly towards longer-term term debt rather than revolving credit facilities.

This capital structure move reflects both increased leverage on the subsidiary level and concentrated refinancing risks given prevailing interest costs significantly above typical investment grade benchmarks.

Nevertheless, the company's liquidity remains robust with current assets totaling approximately $379 million versus current liabilities near $156 million—yielding an enviable current ratio of ~2.43 as of year-end [F1][S17], indicating ample short-term buffers despite leverage obligations.

The consolidated balance sheet thus presents complexity: strong liquidity cushions counterbalance elevated debt cost burdens raising questions on interest expense impact on future profitability.[F1]

Key takeaway: Biglari assumes elevated financing costs at subsidiary level with required vigilant liquidity management evidenced by solid current ratios supporting near-term flexibility.

Capital Allocation: Dividends, Share Repurchases, and Investment Strategy

Capital deployment has remained notably restrained across recent periods with no dividend distributions recorded per available filings [F1]. Instead free cash flow — approximated as operating cash flow minus capex — stood near $76.6 million for FY2025 suggesting resource availability for shareholder returns or debt reduction if prioritized.

Press releases emphasize judicious reinvestment into core operations especially Steak n Shake’s turnaround efforts rather than aggressive buybacks or dividends [S14]. The terminated revolving credit line further suggests capital allocation evolving toward deleveraging rather than shareholder payouts concurrently managing financial obligations arising from the new loan agreement.

Key takeaway: Management favors deploying excess free cash toward business stabilization and liability management over shareholder distributions reflecting conservative stewardship amid uneven earnings.

Asset Valuation Versus Market Price: Understanding the Book Value Premium

At year-end FY2025, Biglari reported shareholder equity approximating $523 million yet its stock trades materially below this book value per share benchmark [F1], signaling market skepticism vis-à-vis reported carrying values.

Such discounting often arises from investor concerns about recurring earnings deficits undermining tangible asset recoverability or challenges emanating from opaque disclosures complicating valuation certainty amid litigation or contingent liabilities noted elsewhere in risk sections [S4].

The price/book discount highlights tension between demonstrated asset substance versus apprehension on future earning power sustainability and governance clarity impacting investor confidence.

Key takeaway: Despite strong equity base underpinning tangible value, market discounts reflect unresolved questions on profitability consistency and transparency dampening valuation multiples.

Key Risks: Profitability Challenges, Leverage Constraints, and Transparency Issues

Biglari Holdings’ risk profile centers predominantly on persistent profitability difficulties evidenced by repeated net income losses including significant downturns captured in recent fiscal years alongside fluctuating operating results tied partially to its restaurant subsidiary operating environment [S4].

Financial leverage introduces interest expense burdens which could constrain discretionary investment or amplify stress during economic downturns given the fixed high-rate loan structure via Steak n Shake [S8]. The lack of granular segment disclosures restricts clarity on competitive threats or resilience factors that might stabilize earnings streams over time.

Additionally legal proceedings noted signal potential contingent liabilities though specifics remain limited per filed reports engaging heightened investor caution regarding unforeseen financial impacts [S4][S5][S6].

Key takeaway: The intersection of erratic earnings performance coupled with structural leverage introduces fragilities magnified by opaque reporting diminishing financial flexibility perceptions.

Looking Ahead: Growth Prospects and Critical Milestones to Monitor

No formal forward guidance has been provided according to latest filings suggesting reliance on periodic operational update releases such as quarterly same-store sales data from Steak n Shake as bellwethers for sustained topline momentum [N3][S3][S21].

Upcoming fiscal quarters will also stress-test company liquidity given scheduled amortization commencing on the large subsidiary loan alongside monitoring any refinancing activity or covenant compliance indicative disclosures potentially materializing post-FY25 closing events.

Investor focus should also encompass updated capital allocation signals particularly regarding share repurchases or potential dividend reinstatement which remain absent but could emerge if free cash flow durability strengthens further amidst greater earnings stability.

Key takeaway (analysis): Close tracking of subsidiary sales momentum combined with leverage servicing capability constitutes pivotal indicators shaping Biglari’s recovery trajectory absent explicit corporate guidance.

Disclaimer: This report is for informational purposes only based on publicly available data as of early March 2026; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments