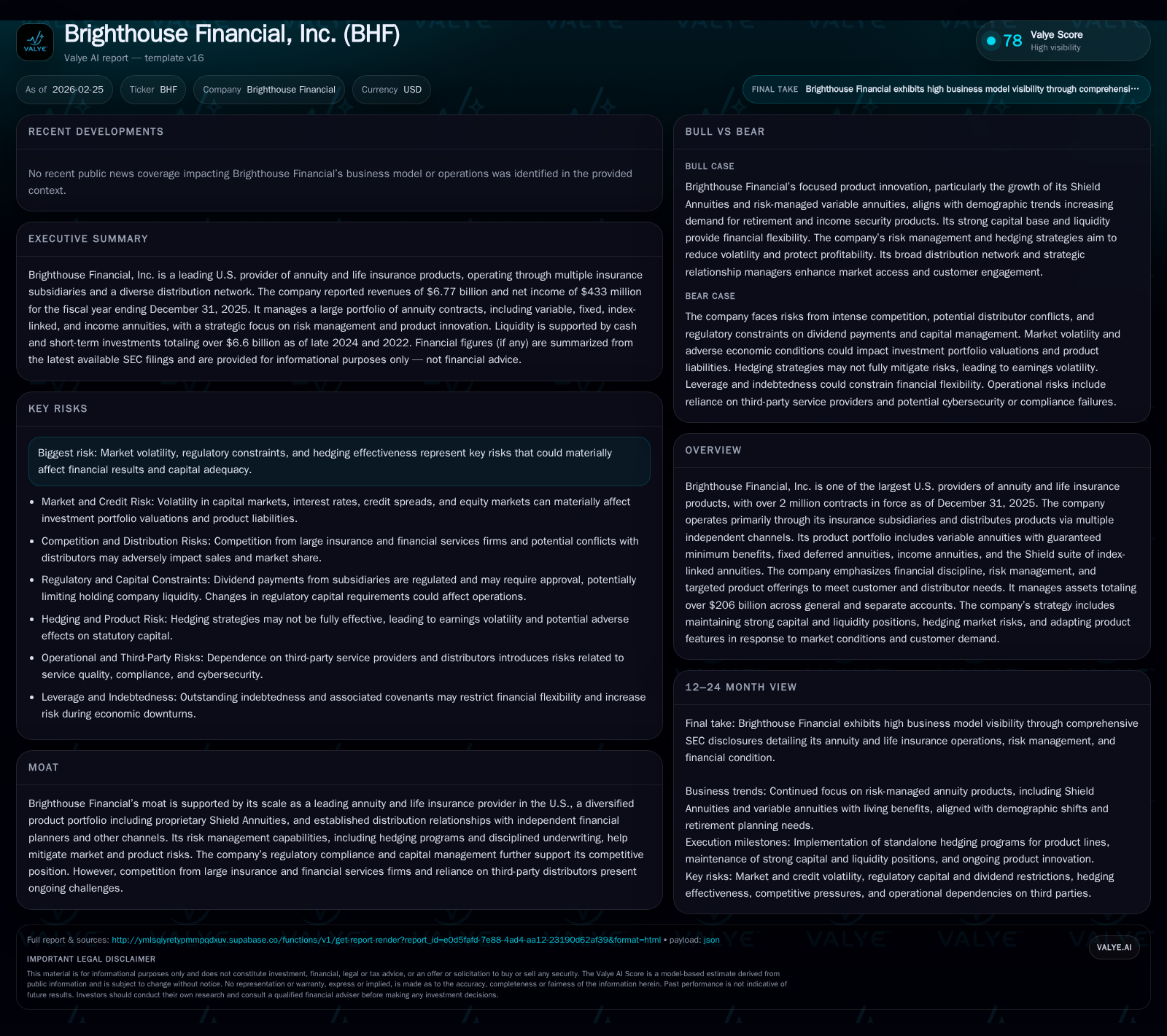

Brighthouse Financial’s Revenue Surge and Capital Strategy in a Competitive Annuity Market

A close examination of Brighthouse Financial’s recent revenue growth, evolving earnings profile, and capital management amidst a challenging insurance market environment.

Brighthouse Financial has experienced a notable rebound in revenues between 2023 and 2025, principally driven by increased sales of targeted annuity products through established independent distribution channels. While net income returned to positive territory with incremental improvements, operating cash flow remains modest despite the top-line growth, reflecting ongoing margin pressures and hedging complexities. The company’s competitive position is bolstered by its proprietary Shield suite of annuities and risk management capabilities, yet competition intensifies alongside regulatory challenges. Capital structure management, including rising equity and controlled leverage, supports liquidity but limits the scope for dividends or repurchases. Looking ahead, demographic tailwinds promise demand growth while market volatility and regulatory developments could constrain profitability and capital flexibility.

Robust Revenue Growth Amid Strategic Product Focus

Brighthouse Financial demonstrated a powerful revenue recovery after a sharp contraction in 2023. Revenues surged from $1.4 billion in FY2023 to $4.724 billion in FY2024 (238% increase), then rose further to $6.766 billion in FY2025—representing a substantial 43.2% growth year-over-year in the latest reported fiscal year [F1]. This expansion reflects the firm’s strategic emphasis on its annuity product portfolio anchored by variable annuities featuring guaranteed minimum benefits and its proprietary Shield suite of index-linked annuities, complemented by fixed deferred and income annuities designed to meet shifting customer demand patterns [S1].

The company’s scale as one of the largest U.S. providers—with over two million contracts in force at December 31, 2025—provides a broad base for cross-selling through multiple independent distribution agreements. These channels enable Brighthouse to maintain differentiated access despite growing consolidation among brokers and financial planners which tends to increase distribution costs and negotiation leverage challenges [S7]. However, this diversified network remains vital for targeted product placement amid evolving retirement planning needs fueled by demographic shifts toward individual responsibility for financial security [S1].

Earnings and Operating Cash Flow: Understanding the Recent Performance Shifts

While top-line figures highlight robust demand, translating this into sustained earnings stability has proven complex. Brighthouse swung from a net loss of -$917 million in FY2023 to positive net income of $388 million in FY2024, then advanced slightly higher to $433 million in FY2025—a double-digit net income growth of approximately 11.6% year-over-year last fiscal year [F1].[N1][N2] Notably, this reflects recovery from an extraordinary downturn that tarnished profitability metrics.

Operating cash flow (CFO) tracked a similar narrative; it was deeply negative at -$1.151 billion in 2022 before partially improving but still negative through 2023 (-$137M) and into 2024 (-$290M). Only recently did CFO turn positive at $259 million for FY2025—a sign that cash generation is improving albeit at modest absolute levels relative to revenues [F1]. This lag underscores margin pressure stemming from hedging program effectiveness—the company deploys various derivative strategies intended to mitigate market risks embedded within guaranteed minimum benefits and other product liabilities—but residual exposures can create earnings volatility given market gyrations [S9].

Additionally, fourth-quarter earnings commentary noted margins compressed due to persistent market headwinds causing valuation fluctuations tied to separate account assets under management—a sector challenge common among annuity providers reliant on equity-linked guarantees [N1][N2]. As hedging remains critical to controlling statutory capital impact as well as earnings swings, Brighthouse continues refining this dynamic.

Competitive Moat Supported by Distribution Networks and Risk Management

Brighthouse Financial’s moat largely derives from its leadership position within U.S. annuity markets combined with focused operational discipline around risk control and tailored product innovation—such as its Shield suite indexing features that offer downside protection while participating in market gains [S1][S23]. This product mix aligns with consumer demand for secure yet growth-oriented retirement solutions.

The company benefits from lasting distributor relationships primarily with independent financial planners who value Brighthouse’s niche offerings; however, ongoing threats include competitive intensity not only from established financial institutions offering broader product arrays but also new entrants leveraging technology platforms or distribution consolidation trends [S7][S23]. Some distributors also offer their own competing products or may shift preference toward firms with more attractive commissions or brand strength.

Hedging efficacy directly influences competitive positioning by enabling more consistent financial results that assure counterparties and ratings agencies—though these programs themselves can be imperfect under extreme market conditions requiring ongoing adjustment [S9]. Regulatory compliance burdens also act as an entry barrier but simultaneously impose cost demands that may constrain agility.

Capital Structure and Liquidity: Managing Leverage and Funding Risks

As of end-2025, Brighthouse exhibited solid equity capitalization amounting to approximately $6.768 billion compared with $4.959 billion just one year prior—an indicator of significant capital buildup over the recent period alongside earnings retention [F1]. Total long-term consolidated debt stood near $3.2 billion consisting primarily of debt securities issued externally; importantly cash flows servicing this debt depend on dividends or intercompany transfers from insurance subsidiaries since parent-level operations generate limited standalone cash flow [F1][S4][S5].

Liquidity is maintained via a senior unsecured revolving credit facility capped at $1 billion maturing April 2027 plus available reinsurance financing arrangements which collectively underpin operational flexibility subject to compliance with covenant testing requiring minimum consolidated net worth thresholds and leveraging ratios [S6][S8]. These covenants potentially restrict additional borrowing or limit capital deployment if ratios approach limits.

Regulatory oversight enforces dividend restrictions on subsidiaries aimed at preserving statutory capital adequacy (measured via RBC ratios) that may limit distributable cash—especially extraordinary dividends require regulator approval—thereby constraining holding company flexibility around shareholder returns or leverage reduction initiatives [S10]. Failure to maintain requisite capital levels invites supervisory intervention possibly impacting business conduct.

Dividend Policy, Share Repurchases, and Return on Equity Analysis

Capital allocation displays caution consistent with maintaining robust solvency positions amid ongoing market uncertainty. Dividends on common stock have been largely absent post-2019; historical activity notably includes material dividend payouts through 2018 but none reported beyond that period according to filings [F1]. Conversely, share repurchase programs remain active albeit scaled down—from repurchases totaling $488 million in FY2022 gradually declining through FY2024 ($250 million) down to about $102 million in FY2025 reflecting more conservative deployment aligned with profitability trends [F1][N6].

This restrained approach prioritizes balance sheet strength over aggressive capital returns given the sensitivity of annuity liabilities to market cycles.

Based on reported net income of $433 million over shareholders’ equity around $6.768 billion at year-end 2025, an approximate trailing return on equity (ROE) stands near 6.4%—indicating recovering yet moderate profitability relative to invested capital levels typical within risk-averse life insurance segments where emphasis lies equally on capital preservation along with growth [F1].

Industry commentary suggests some buy-side views regard Brighthouse as undervalued given its improving fundamentals and disciplined allocation framework supporting sustainable competitive advantages despite cyclical challenges [N6].

Outlook: Monitoring Market Conditions, Regulatory Impact, Milestones & Product Evolution

Looking forward, Brighthouse’s opportunities are anchored by favorable demographic trends: an aging U.S. population increasingly responsible for retirement funding fosters sustained demand for annuities offering stable lifetime income solutions combined with inflation protection features embedded within proprietary indexed products like Shield Annuities[S1][N6].

However, constraints loom large—from persistent market volatility undermining hedging predictability thus affecting earnings consistency; potential tightening of regulatory capital requirements or standard-of-conduct rules influencing distribution economics; heightened pricing competition among channel partners; plus macroeconomic shifts such as prolonged low interest rates dampening investment yield floors critical for profit margins [S9][S23][S28].

Management communications emphasize continuing disciplined underwriting coupled with adaptive product design capable of frequent repricing or feature revision under changing conditions—a critical capability given evolving regulation—and highlight vigilance around liquidity under adverse stress scenarios entailed by derivative collateral calls or rising claims experience variation associated with public health events[S9][N6].

Key milestones include quarterly updates on sales volumes particularly across newly launched indexed annuities demonstrating customer acceptance; progression of hedging program refinement yielding smoother accounting outcomes; regulatory developments potentially reshaping allowable compensation schemes affecting distributor alignment; as well as rating agency actions reflecting perceived financial strength trajectory[N1][N2][S9]. These milestones will be critical indicators shaping investor expectations.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 6.8 | 433 | 259 | +43.2% | +11.6% |

| 2024 | 4.7 | 388 | -290 | +237.4% | +142.3% |

| 2023 | 1.4 | -917 | -137 | -83.5% | -18440.0% |

| 2022 | 8.5 | 5 | -1151 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc, Capex, Div, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 102 | 6.4 |

| 2024 | 250 | 7.8 |

| 2023 | 250 | -18.6 |

| 2022 | 488 | 0.1 |

Source: SEC companyfacts cache [F1]. Note: Dividend data less than two years not available; last material dividends paid before this period

This analysis is based solely on information publicly disclosed through company filings ([F1],[S#]) and recent media coverage ([N#]). It does not constitute investment advice or recommendations but aims to provide an informed view of Brighthouse Financial’s recent financial dynamics and strategic position within the U.S. insurance sector.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments