Byrn, Inc. Highlights Dormant Status with Critical Ownership Changes

The latest quarterly filing confirms Byrn operates as a dormant shell while a recent major stock purchase signals a shift in control.

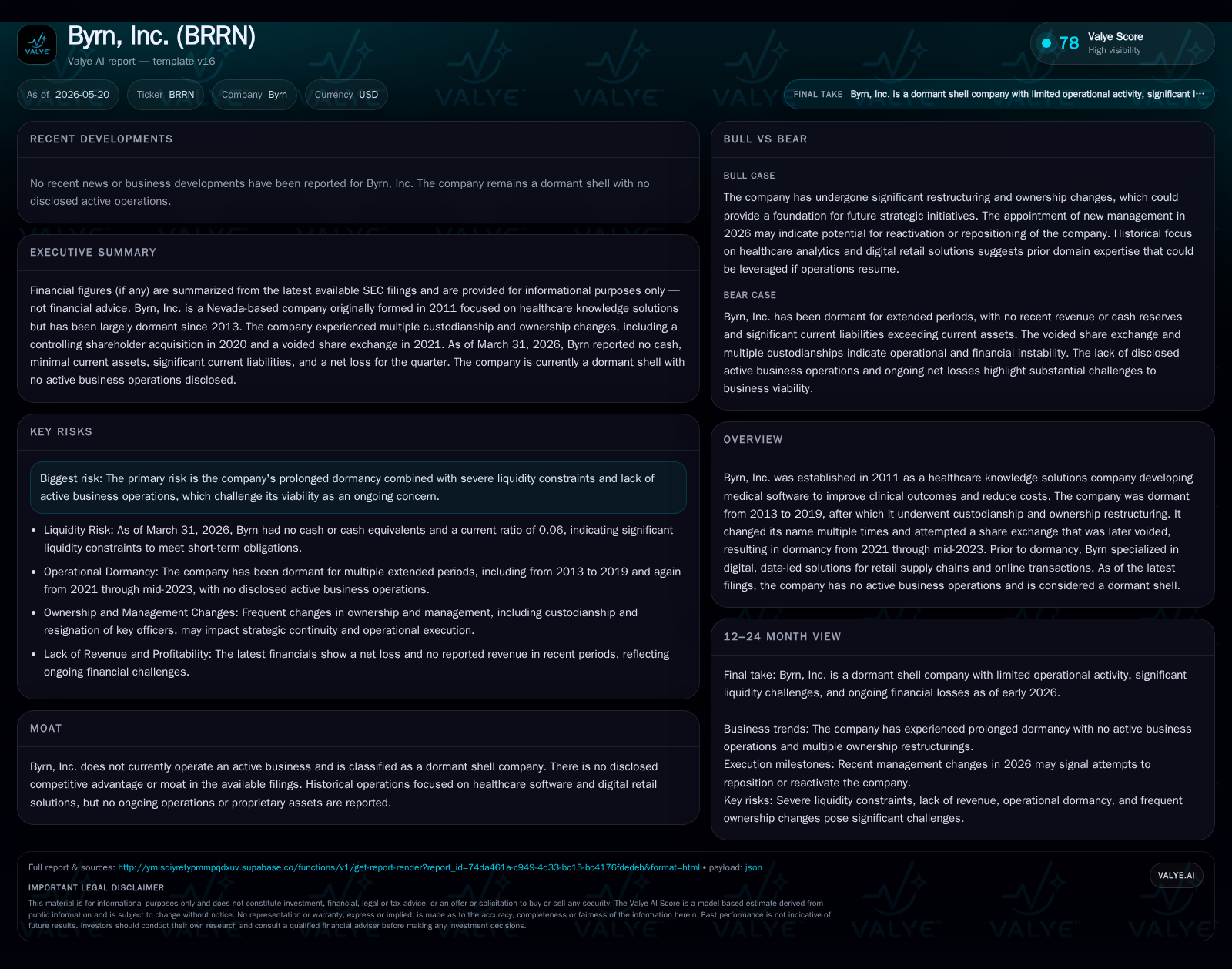

Byrn, Inc.’s 10-Q filed May 19, 2026, reaffirms its dormant operational status with no active business. An April 8-K disclosed a pivotal transaction where MEDO Healthcare LLC acquired super-voting preferred shares controlling nearly 85% of voting power, replacing prior custodian-led ownership. Historically focused on healthcare analytics and digital retail supply chains, Byrn now lacks any operating assets or revenues amid severe liquidity constraints. The new ownership structure positions the company for a potential strategic reset, though no concrete business plans have been disclosed.

Latest Quarterly and Event Filings Clarify Current Status

Byrn’s most recent Form 10-Q filed May 19, 2026, marks a continuation of its long-standing dormancy with clear evidence of no active operations. Notably, the company indicated it has not submitted electronically any Interactive Data Files required under Regulation S-T for the past twelve months—a strong signal that it maintains no substantive financial activity or operational data reporting [S2]. The filing reflects a company in stasis without commercial revenue or underlying product engagement.

Complementing this disclosure is an April 24, 2026 Form 8-K detailing a significant change in control event: MEDO Healthcare LLC acquired the entire issuance of Series A-1 Preferred Stock from Custodian Ventures LLC for $175,000 in cash. Given each preferred share carries voting power equivalent to 250 common shares, this acquisition confers over 84% voting power to MEDO Healthcare LLC—effectively consolidating majority control from the prior custodian-led ownership arrangement [S3], [S7]. Following this transaction, David Lazar resigned his roles as sole director and officer; John Leo was appointed sole director and CEO alongside Arthur Magee as CFO and Secretary [S16]. This governance shift illustrates tangible near-term changes in leadership despite no immediate operational revival.

Historical Business Model and Operational Context

Established in April 2011 as Quture International before evolving into Byrn Inc., the company initially sought to establish itself as an emerging healthcare knowledge solutions provider focused on developing software tools and analytic platforms intended to transform clinical performance measurement. Its stated aim was enhancing outcomes and predictive insight within healthcare while reducing costs through evidence-based clinical processes [S1],.

However, Byrn experienced two notable dormancy phases: first from March 2013 until December 2019 when it was inactive; then after an attempted share exchange deal in February 2021 involving Alkeon Creators Inc. was voided, leading to another extended period of dormancy until July 2023 when custodianship resumed under Custodian Ventures LLC [S1], [S5],. During its brief active years prior to dormancy episodes, Byrn pivoted towards digital retail supply-chain technology focusing on data-driven solutions for digitizing discovery and transactions online but failed to substantiate sustainable operations or revenue streams. These prolonged operational interruptions severely hampered its ability to maintain technology products or secure customer adoption.

Dormant Shell and Ownership Structure Dynamics

Byrn’s capital structure includes approximately 450 million issued common shares alongside 10 million Series A-1 Preferred Shares—each convertible into 250 common shares and bearing super-voting rights tantamount to controlling influence on corporate governance [S3], [F1]. This structure allows preferred shareholders outsized voting clout relative to their economic stake and concentrates decision-making power.

The recent transfer of these preferred shares from Custodian Ventures LLC—controlled formerly by David Lazar—to MEDO Healthcare LLC represents a critical realignment of control. MEDO Healthcare now wields approximately 84.7% of voting power owing to these rights despite holding only about 2% of total common-equivalent shares. Common stock holders number over four hundred million but possess minimal effective control compared to dominant preferred shareholders [S7], [F1].

John Leo's appointment as sole director and CEO post-transaction brings seasoned financial services leadership including decades of experience in investment banking and regulatory compliance—indicating potential strategic intent behind the ownership change. Nonetheless, governance concentration presents risks related to limited minority shareholder influence.

Competitive Landscape and Industry Context of Past Operations

Byrn's former business endeavors straddled highly complex sectors such as healthcare IT analytics and digital retail supply chain management—both characterized by significant regulatory oversight, demanding technology innovation cycles, and competitive barriers related to integration with client workflows and data ecosystems. These industries typically require sustained R&D investment alongside robust customer acquisition and retention strategies supported by differentiated software offerings with proven outcome improvements or cost savings.

Given Byrn's repeated dormancy intervals disrupting continuity in product development or customer engagement plus absence of ongoing operations, it effectively holds no competitive moat in these markets today. The challenges of pricing pressures, channel access limitations, switching costs inflicted by incumbent platforms likely compounded its inability to sustain traction historically, [S1]

Key Risks Stemming from Prolonged Dormancy and Financial Health

A primary red flag is Byrn’s precarious liquidity position evidenced by zero cash balance at quarter-end March 31, 2026 coupled with minimal current assets ($2.2k) against liabilities exceeding ~$36k—yielding a perilously low current ratio (0.06), which highlights an acute working capital deficit scenario [F1]

This weak financial footing considerably undermines Byrn’s viability absent external capital infusion or a transformative strategic transaction restoring operational activities. The dormant shell status implies heightened regulatory scrutiny risks especially around timely filings compliance and disclosure adequacy given lack of ongoing business transactions.

Governance concentration within super-voting preferred stockholders presents additional shareholder dilution risks and potential conflicts should new stakes seek restructuring maneuvers or asset dispositions without broad stakeholder consensus.

Growth Opportunities or Revival Pathways: Current Outlook

While the change in control reflected by MEDO Healthcare’s majority acquisition combined with John Leo’s financial industry leadership hints at groundwork for possible future revitalization efforts or strategic repositioning using Byrn as a public shell vehicle; there is neither explicit operational plan nor pipeline indicated in disclosed filings at present [S3],.

Potential paths could include pursuit of reverse merger targets or asset acquisitions leveraging the existing public listing feature; however these remain speculative without formal announcements or milestones. Absent clear business reactivation initiatives detailed publicly the outlook remains uncertain.

What Investors Should Watch Next

Stakeholders monitoring Byrn should prioritize assessing future quarterly Form 10-Q filings for any deviation from dormancy disclosures such as resumption of interactive data file submissions or mention of renewed business activities [S2]. Additionally tracking insider transactions including any further equity transfers among preferred holders or changes in beneficial ownership could signal evolving strategic directions.

Management commentary if forthcoming regarding capital raises or strategic partnerships would represent important barometers for execution progress given the company currently lacks operating revenues or assets generating value internally.

Financial Profile Summary

Byrn’s balance sheet as of March-end shows negligible liquid resources with cash at zero USD and limited current assets totaling $2,178 against current liabilities around $36,440 resulting in a sharply negative working capital posture (current ratio ~0.06) consistent with dormant shell characteristics [F1]. Total recorded debt approximates $70,000 dating back to earlier periods without offsetting revenue streams evident since last operating activities ceased years ago [F1]. This tensile strain on financial health underscores dependence on equity funding events like the recent preferred stock sale for continued existence.

This analysis is based strictly on publicly available filings up to May 19, 2026 ([S1]-[S18], [F1]) and does not incorporate speculative assumptions beyond documented facts. It aims solely to provide detailed insights into Byrn's recent operating posture alongside structural corporate developments affecting its trajectory going forward.

Financial position in context

As of 2026-03-31, companyfacts shows 0 USD in cash and equivalents [F1]. Current assets of $2178 and current liabilities of $36440 imply a current ratio near 0.06x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments