Bit Digital Shifts to AI-Focused Cloud and HPC Services Amid Ongoing Industry and Geopolitical Risks

The latest quarterly report reveals Bit Digital's strategic pivot from cryptocurrency mining to cloud and high-performance computing infrastructure tailored for AI workloads, alongside operational challenges and competitive pressures.

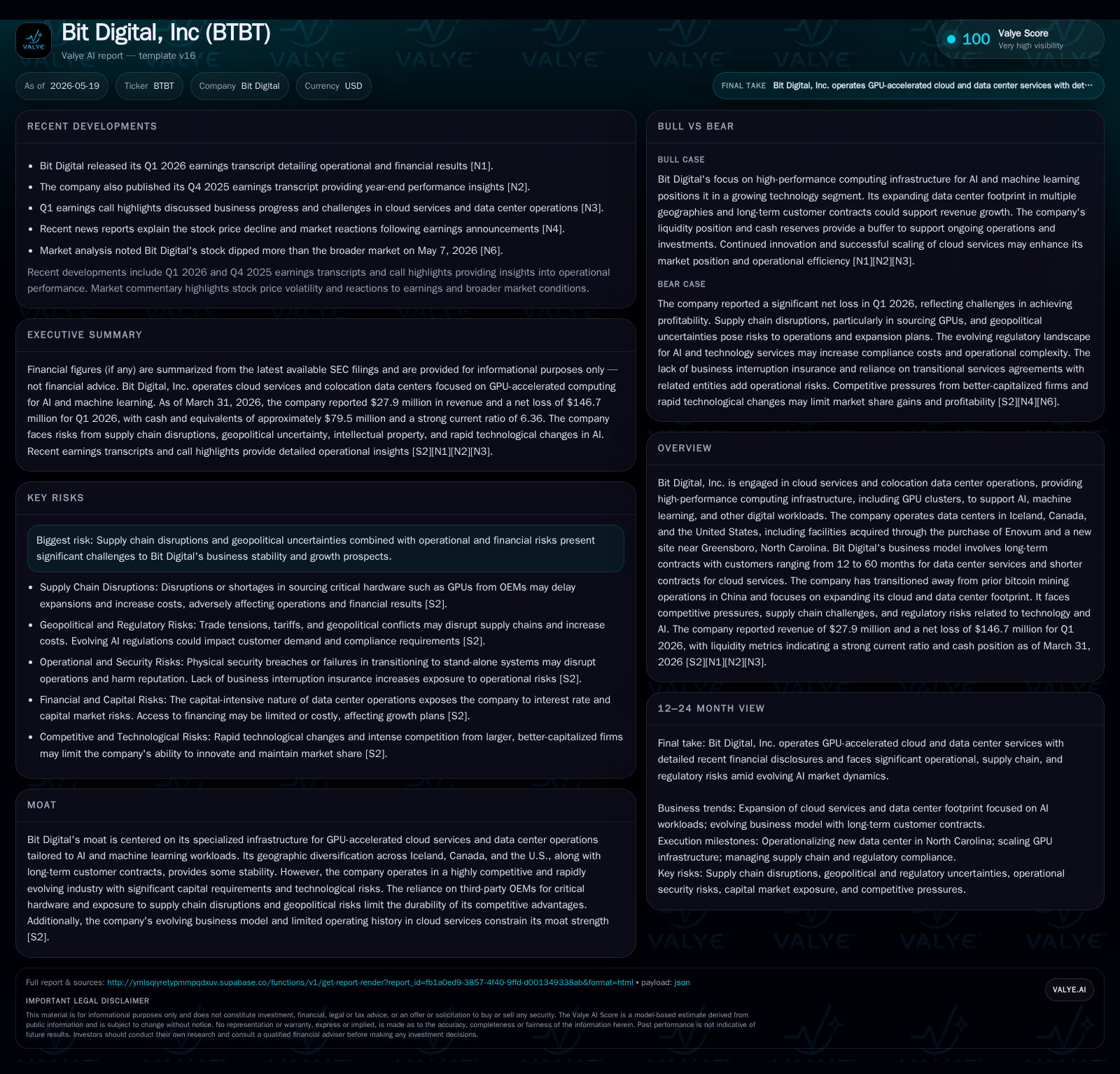

Bit Digital's May 2026 quarterly filing highlights its transformation from legacy cryptocurrency mining toward AI-centric cloud services and HPC data center operations across Iceland, Canada, and the U.S. leveraging long-term customer contracts. Despite revenue growth linked to these services, the company continues to incur significant operating losses amid supply chain challenges, evolving technology demands, and geopolitical uncertainties impacting its capital-intensive infrastructure business. Its competitive position rests on specialized GPU-accelerated computing infrastructure, but risks include hardware supply limitations, regulatory volatility, and integration costs following acquisitions. Going forward, execution on contract expansions and managing industry headwinds will be key growth determinants.

Latest Operating Update

Bit Digital’s most recent quarterly filing dated May 15, 2026 [S2] marks an important checkpoint in its strategic pivot away from legacy bitcoin mining towards becoming a provider of high-performance computing (HPC) infrastructure tailored to artificial intelligence (AI) workloads. The company reported $27.9 million in revenue during the first quarter of 2026 [N1], reflecting revenue recognition predominantly from its colocation data center services and associated cloud offerings under long-term contracts. Despite revenue growth momentum driven by customer adoption of GPU-accelerated compute solutions in facilities spanning Iceland, Canada, and the United States—including recent acquisitions such as Enovum Data Centers—the company posted a net loss reflecting ongoing investments in capacity expansion and operational maturity [S2].

This quarterly update confirms Bit Digital’s full transition out of bitcoin mining operations previously concentrated in China—a structural shift explained in its annual report [S1]—and focuses on growing WhiteFiber Inc.’s cloud services business where it holds approximately 70.5% ownership post-IPO [S1]. New data center developments near Greensboro, NC enhance geographic diversification aimed at capturing growing North American AI demand.

Business Model Overview

Bit Digital operates through ownership stakes primarily in WhiteFiber Inc., which manages high-performance GPU-accelerated data centers providing colocation and cloud computing services optimized for AI workloads. Customers engage via long-term contracts ranging from one year up to five years (12-60 months), securing predictable revenues tied to committed capacity usage [S1]. These contracts typically involve clients such as AI developers needing scalable access to GPU clusters without heavy capital expenditure.

Revenue mechanics depend on factors including contracted capacity volumes, pricing arrangements based on contracted terms or usage intensity, mix shifts toward higher-margin cloud services versus pure colocation rents, and contract renewals or expansions. Margins are affected by hardware acquisition cost pressures (notably GPUs), energy expenses—especially relevant given sites in Iceland benefiting from renewable energy—and operational efficiencies realized post-integration of acquired data centers like Enovum [S1], [S2].

WhiteFiber’s public listing has introduced transitional service agreements with Bit Digital; however, as WhiteFiber develops standalone IT infrastructure replacing shared corporate functions (e.g., finance systems, legal support), operating costs may increase temporarily due to duplication or inefficiencies during this build-out phase [S19]. This evolution impacts consolidated financial results until full independence is achieved.

Industry Structure & Competitive Positioning

The global market for AI-focused cloud infrastructure is growing rapidly with estimates projecting an increase from $60.5 billion in 2024 to over $360 billion by 2030 at a CAGR exceeding 35% [S1]. This explosive growth stems from escalating AI adoption across sectors demanding massive computational power largely served via GPU-centric compute clusters hosted by third-party providers.

Bit Digital’s competitive strength lies in:

- Geographic diversification across stable jurisdictions with favorable energy costs (Iceland’s renewable grid) and proximity to key North American customers.

- Specialized HPC infrastructure tailored for AI/ML use cases emphasizing GPU acceleration.

- Long-term contractual relationships yielding some revenue visibility amid evolving market dynamics.

However, its moat is moderate rather than strong due to several mitigating factors:

- High capital intensity requiring continuous investment to maintain cutting-edge hardware.

- Dependence on OEM suppliers for GPUs facing global supply constraints.

- Exposure to geopolitical risks impacting supply chains between China, Taiwan (chip origin), US-Mexico (component manufacturing), and Canada-US relations [S24].

- Rapid technological change requiring agile platform upgrades to stay relevant.

- Limited operating history independently as WhiteFiber post-spinoff introduces transitional operational risk.

Peers range from mega-cloud providers with expansive ecosystems plus vertical integration advantages to smaller HPC-focused operators competing on price or niche specialization.

Growth Drivers

Several drivers underpin near-to-medium term growth prospects:

- AI Demand Surge: Widespread digital transformation accelerates client demand for scalable GPU compute power enabling larger models and real-time inference capabilities.

- Cloud Migration: Customers favor offloading capital-intensive compute investments toward flexible consumption models based on white-labelled or proprietary clouds like those operated by WhiteFiber.

- Geographic Footprint Expansion: Recent acquisition of Enovum Data Centers strengthens Canadian presence while facility development near Greensboro broadens U.S. market access.

- Contract Backlog & Renewal Rates: Long-duration contracts reduce churn risk; winning multi-year renewals supports stable revenue base.

- Vertical Integration Potential: Opportunities exist to layer value-added managed services or proprietary software atop base infrastructure creating differentiation.

- WhiteFiber IPO Benefits: Access to capital markets facilitates financing for further capacity additions supporting scaling ambitions [S1], [S11].

Maintaining alignment between contract pricing strategies amidst hardware cost inflation will remain crucial alongside continuing investment into systems resilience given no current insurance coverage for business interruption [S23]

Risks & Growth Constraints

Key risks include:

- Supply Chain Disruptions: Persistent chip shortages or trade restrictions could delay hardware deployments essential for expanding capacity or upgrading existing clusters [S24].

- Geopolitical Volatility: Tensions among U.S., China, Taiwan region impact component sourcing; conflicts affecting Red Sea trade routes may increase logistics costs materially impacting overall operations [S2].

- Regulatory Uncertainties: Retroactive liabilities linked to previous Chinese mining activities remain possible despite exit over two years ago; extended statute limitations could trigger fines or penalties [S2].

- Operational Transition Challenges: WhiteFiber’s separation requires system builds that risk temporary business interruptions increasing expense loads before stabilizing at scale [S19].

- Lack of Business Interruption Insurance: Current uninsured status against physical or cyber disruptions exposes earnings vulnerability should key facilities suffer outages [S23].

- Legal Proceedings: Ongoing litigation against Blockfusion may involve damages exceeding $5 million; uncertain outcomes could influence financial flexibility [S1].

- Technological Evolution Pace: Advances like open-source AI models potentially reduce compute requirements or alter demand fundamentals posing forecasting challenges [S25].

These constraints necessitate prudent capital management while vigilantly adapting business strategy vis-à-vis emerging market trends.

What to Watch Next

Important upcoming developments influencing Bit Digital’s trajectory include:

- Quarterly SDS releases disclosing contract wins/losses velocity within core cloud/HPC businesses signaling commercial traction or headwinds.

- Milestones related to full operational independence of WhiteFiber critical IT functions removing reliance on transitional arrangements impacting profitability metrics.

- Supply chain health indicators concerning availability/prices of GPUs influencing capex pacing decisions.

- Integration progress of Enovum assets alongside announced facility near Greensboro providing evidence of successful expansion execution.

- Regulatory updates concerning prior China mining compliance issues that might affect capital allocation or legal provisions.

- Any strategic announcements targeting managed service offerings layered over base infrastructure enhancing product mix quality.

Monitoring these milestones will provide insights into whether Bit Digital can convert growth opportunities into sustainable profitability amid complex external pressures.

Financial Profile Snapshot

As of March 31, 2026 quarter-end [F1]:

Bit Digital holds a robust liquidity buffer with cash & equivalents totaling approximately $79.5 million while sustaining only low reported debt levels around $3 million recorded end 2022—a figure unchanged recently per available disclosures—resulting in net cash positioning supported by a strong current ratio of around 6.36 indicating healthy short-term asset coverage over liabilities.

This analysis is based solely on publicly filed SEC documents dated through May 15, 2026; no investment research views are made.

Financial position in context

As of 2026-03-31, companyfacts shows $80mm in cash and equivalents [F1]. Current assets of $500mm and current liabilities of $79mm imply a current ratio near 6.36x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments