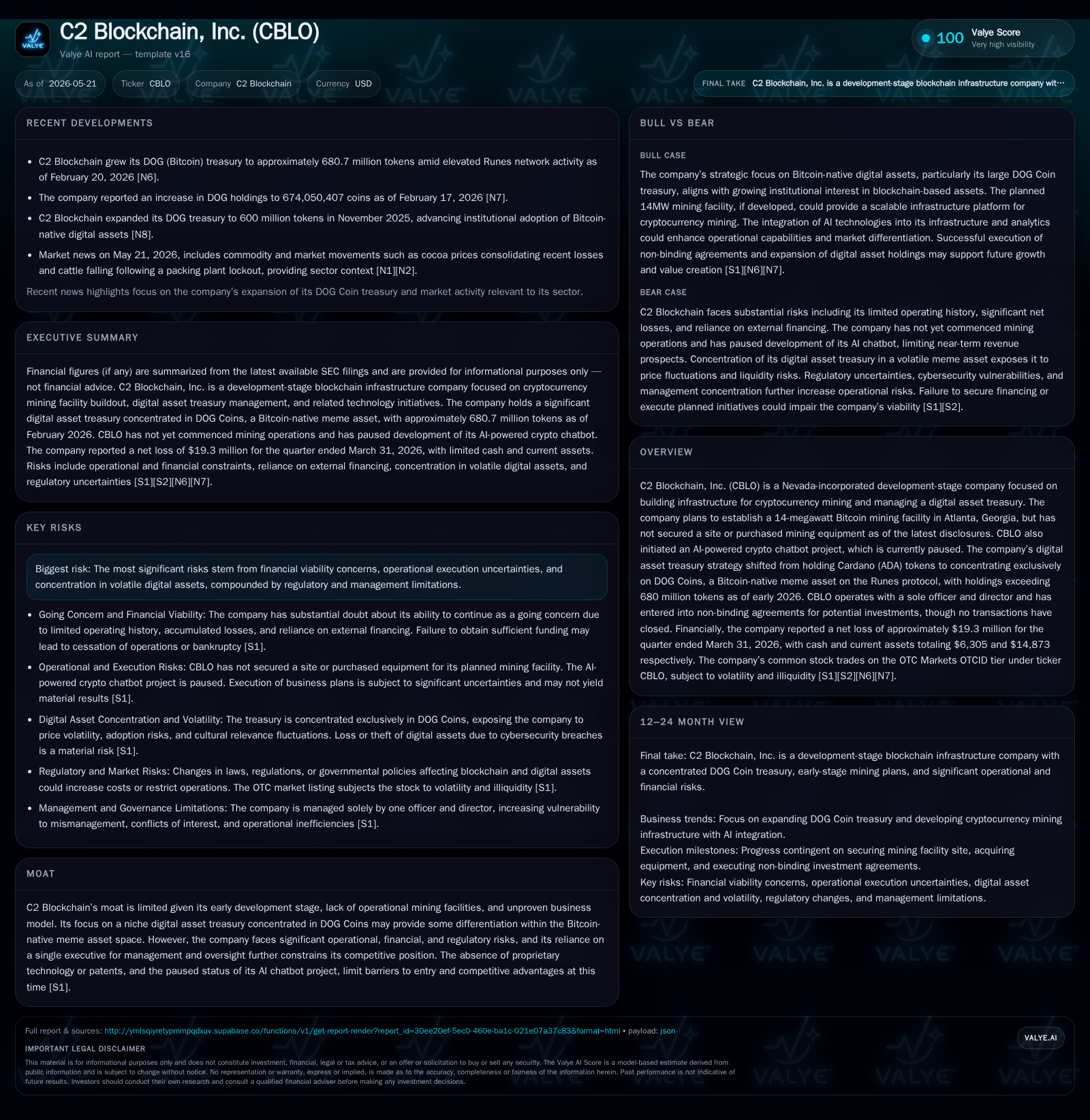

C2 Blockchain's Development Stage Poses Execution and Capital Challenges

The latest quarterly update reveals C2 Blockchain’s slow transition from a shell to an operational crypto miner, highlighting capital needs, incomplete infrastructure, and volatile asset exposures.

C2 Blockchain remains a development-stage company aiming to build a 14-megawatt Bitcoin mining facility in Atlanta, yet it has not secured a site or acquired mining equipment as of the May 2026 quarter. The company’s digital asset treasury strategy shifted from Cardano to a concentrated position in DOG Coins, exposing it to niche Bitcoin-native meme token volatility. Recent convertible note financing indicates ongoing capital constraints with critical execution milestones still pending. The paused AI crypto chatbot project further limits near-term revenue opportunities. Overall, CBLO faces significant operational and financial risks inherent in its early stage and concentrated digital asset approach.

Latest Quarterly Operational Update and Why It Matters

C2 Blockchain’s most recent Form 10-Q filed May 20, 2026, reinforces its status as an early-stage development company with ambitious but unrealized Bitcoin mining infrastructure plans [S2]. The Company continues targeting a 14-megawatt mining facility in Atlanta, Georgia due to favorable electricity costs and environmental factors, yet has not finalized site acquisition nor purchased any mining hardware as of the latest disclosures. This inability to secure foundational resources underlines significant execution challenges [S1][S2].

Financially, CBLO issued a convertible promissory note on April 23, 2026, raising $100,000 in gross proceeds under non-public terms emphasizing reliance on accredited investors without general solicitation [S3][S28]. This capital infusion underscores ongoing funding needs vital for progressing infrastructure developments.

Simultaneously, the company’s strategic pivot in digital asset holdings away from Cardano (ADA) toward DOG Coins marks a shift in treasury risk exposure. Having fully divested ADA at a realized loss roughly equal to an earlier impairment charge ($12,668), CBLO now holds over 680 million DOG Coins — a meme-native cryptocurrency operating on the Bitcoin blockchain via Runes protocol [S1]. This positions the treasury within a highly volatile niche digital asset class.

Additionally, the proprietary AI-powered crypto chatbot launched experimentally in mid-2025 is currently paused with no generated revenues reported [S1]. This pause delays any near-term scaling of subscription-based analytics products tied to blockchain market data.

Collectively, these developments showcase C2 Blockchain’s early progress while reiterating substantial milestones yet unmet and critical dependence on financing for tangible operational advancement.

Business Model Overview and Product/Service Quality Considerations

C2 Blockchain’s business model centers primarily on developing cryptocurrency mining infrastructure coupled with managing a digital asset treasury intended as both investment reserve and strategic growth element [S1]. Mining revenue potential derives from establishing operational Bitcoin mining rig capacity—projected at 14 MW—which at full deployment could generate earnings tied to Bitcoin price levels, power costs, and equipment efficiency benchmarks. However, without any machines purchased or sites secured thus far, revenue generation remains speculative.

The company's temporary venture into AI-powered crypto analytics via its chatbot aimed to leverage machine learning combined with real-time blockchain data to provide trading insights for retail and institutional customers [S1]. Though this product introduced a subscription revenue model, its development halt diminishes short-term prospects for recurring income unrelated to mining.

On the treasury side, moving away from ADA tokens in favor of DOG Coins signals a deliberate concentration in a Bitcoin-native meme token ecosystem rather than more established altcoins. While this could differentiate the treasury profile within bitcoin-focused assets, it also exposes CBLO to greater price swings inherent in meme coin markets that often lack liquidity depth compared to mainstream cryptocurrencies.

Notably absent are any proprietary technologies or intellectual property rights that could create barriers against competitive encroachment; the company openly holds no patents or copyrights related to its AI chatbot or other initiatives [S1]. Therefore, defensibility depends largely on execution speed in infrastructure buildout and strategic flexibility.

Competitive Environment and Industry Position

The cryptocurrency mining industry is highly competitive with dominant players benefiting from scale economies, favorable power purchase agreements, advanced cooling systems, and regulatory compliance expertise. Operating costs are heavily influenced by geographic electricity prices and regulations surrounding energy consumption.

As an unestablished miner without physical facilities or hardware deployments, C2 Blockchain currently resides at the earliest stage of the value chain—planning and capital sourcing—contrasting starkly with integrated miners running tens or hundreds of megawatts worldwide. This immaturity limits pricing power and exposure to economies of scale.

Moreover, although treasury management is common among miners diversifying income sources through digital assets holdings or staking rewards, CBLO’s specialization in DOG Coins—a niche Bitcoin-network meme token—is atypical versus many peers that prefer more liquid mainstream coins like BTC or ETH [S1]. This exclusivity could reduce comparable valuation metrics but potentially attract investors interested in novel digital assets.

Governance structure amplifies competitive headwinds; sole executive control diminishes oversight robustness common among peer firms employing broader management teams and independent directors [S1]. Additionally, regulatory environments governing crypto infrastructures remain uncertain especially regarding environmental policies affecting energy-intensive miners.

Key Growth Drivers Supporting Future Development

Progress toward operational Bitcoin mining stands as CBLO’s primary growth lever. Securing a viable physical site within Atlanta would validate project feasibility given local energy cost advantages. Following this milestone will be procurement of efficient ASIC mining hardware (e.g., Antminer S19 XP series), installation completion, then ramp-up of mining activity generating sustainable revenues over time [S1][S2].

Capital is integral: recent issuance of a $100k convertible promissory note illustrates ongoing necessity for external funding to support these phases [S3][S28]. Success attracting further equity or debt financing directly impacts timeline adherence.

Beyond mining operations growth derives from digital asset treasury appreciation—principally from DOG Coin price movements—and possible monetization strategies such as selective portfolio reallocations depending on market conditions [S1].

Resumption of the AI-driven crypto chatbot project could diversify revenue streams if redevelopment occurs; reintroducing subscription services blending blockchain analytics with machine learning could enhance engagement with retail/institutional sectors that favor data-driven trading tools.

While all growth drivers are conditional upon clearing critical execution hurdles (site acquisition, financing closings), their realization would mark material advances towards operational maturity.

Risks and Constraints Impacting Execution and Financial Viability

CBLO faces profound risks inherent in nascent business stages: absence of production facilities results in zero material revenues while ongoing expenses generate operating losses highlighting funding pressures [F1][S1][S2]. Low cash reserves ($6.3k) paired with modest current assets ($14.9k) underscore tight liquidity requiring near-term capital inflows to avoid operational stagnation [F1].

The concentrated holding of DOG Coins exposes the company balance sheet directly to extreme volatility characteristic of meme coin markets which may amplify unrealized losses affecting equity valuations and financing conditions [S1]. Prior divestment of ADA tokens resulted in an impairment loss evidencing susceptibility.

Operational risks also include securing suitable locations properly zoned for high-power consumption industrial use—a process complicated by regulatory scrutiny aimed at balancing environmental impact versus economic benefits [S1]. Delays or failures here could defer entire mining project viability.

Managerial concentration poses governance weaknesses; sole officer/director model limits checks/balances which may impede responsive decision-making capacity during crises or scaling phases [S1]. Absence of independent oversight raises fiduciary challenges uncommon among peers who maintain multi-person leadership teams.

Finally, unclosed non-binding agreements suggest uncertainties surrounding expansion via acquisitions or investments which temper growth outlook clarity and potential synergies [S1][S9].

Milestones and Indicators to Watch Next

Key milestones serve as tangible markers indicating whether CBLO advances beyond concept stage:

- Announcements regarding acquisition or contractual rights over Atlanta-area mine sites will substantiate core infrastructure planning progress [S2].

- Confirmation of first large-scale mining equipment orders/purchases will evidence tangible capex deployment aligning with stated strategies [S2][S3].

- Developments related to AI chatbot project (reactivation or shelving decisions) would clarify secondary product initiative prospects impacting diversified revenue potential.

- Closure or cancellation updates on non-binding investment agreements including those involving CoinEdge Inc. or A.R.T Digital Holdings Corp., elucidate external validation of business expansion strategy [S1][S9].

- Market price trends in DOG Coins may disproportionately affect balance sheet strength — fluctuations here serve as indirect proxy indicators of treasury health.

- Further fundraising efforts beyond existing convertible notes identify whether requisite capital is realistically attainable under favorable conditions [S28][S3]. These metrics collectively provide empirical checkpoints assessing operational execution momentum amid high uncertainty.

Supporting Financial Snapshot from Latest Quarter

C2 Blockchain reported cash & equivalents totaling approximately $6,305 as of March 31, 2026 along with total current assets near $14,873 reflecting limited working capital available for development activities ([F1]). Revenues remain negligible at $185 for the most recent annual data point ending June 30, 2025 while net losses exceed $235k underscoring unprofitable status consistent with development-stage classification ([F1]). The filings reveal no specific mention of debt beyond convertible note details indicating an absence of sizable outstanding liabilities which can be interpreted as limited leverage exposure ([S3]). Nonetheless liquidity constraints persist given small cash buffers relative to capital-intensive ambitions.

This financial backdrop complements operating observations pointing toward urgent need for fresh capital infusion supporting continued infrastructure development alongside managing volatility risks embedded within concentrated digital asset holdings.

Disclaimer: This analysis is based solely on publicly available SEC filings up through May 2026 and does not constitute investment advice or research views. All forward-looking statements reflect management expectations subject to risks described herein.

Financial position in context

As of 2026-03-31, companyfacts shows $6305 in cash and equivalents [F1]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments