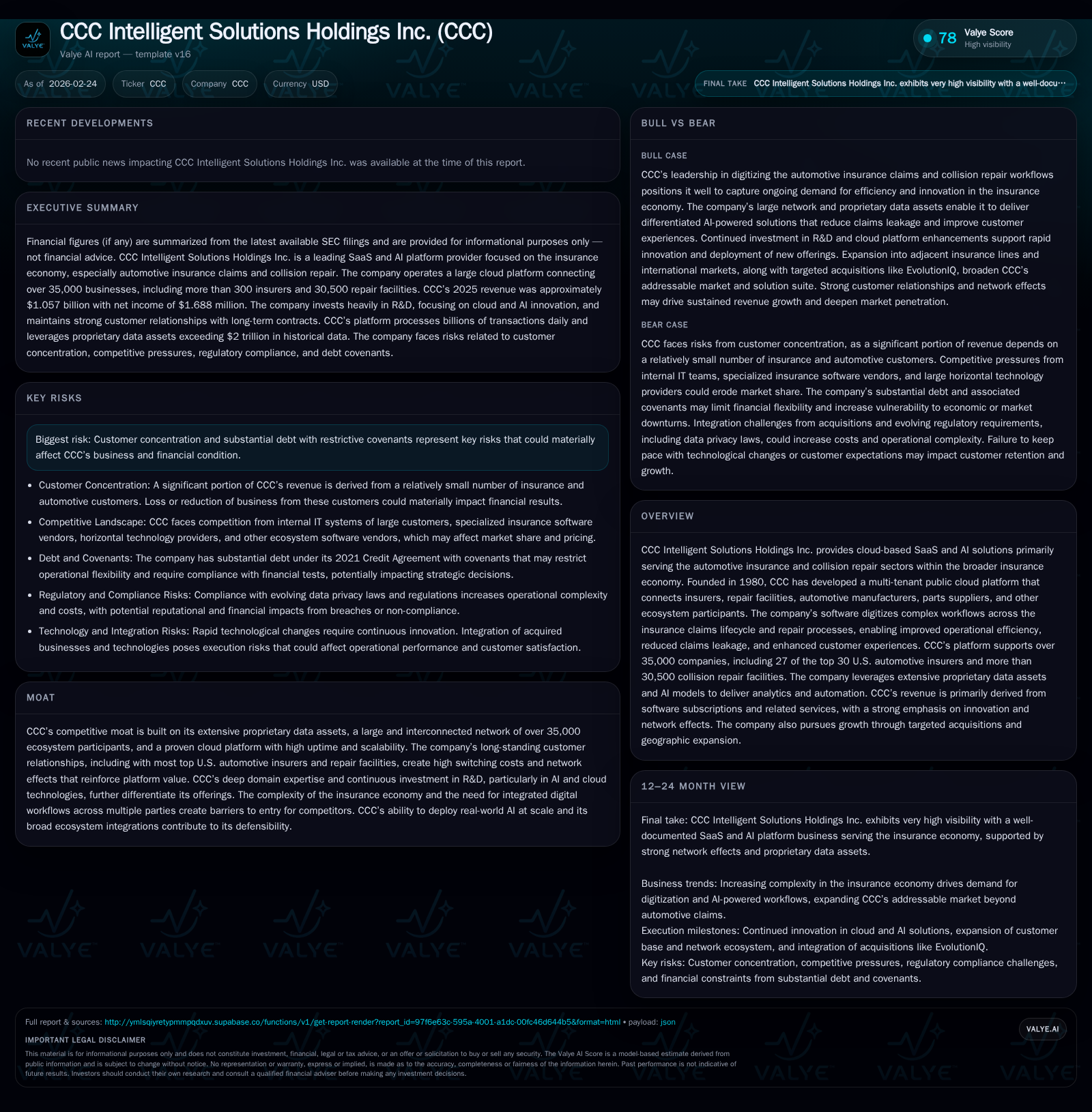

CCC Intelligent Solutions’ Revenue Growth and AI Leadership Spur Industry Influence

CCC drives digital transformation in automotive insurance through AI-powered SaaS, leveraging proprietary data and a vast ecosystem amid financial and customer concentration challenges.

CCC Intelligent Solutions Holdings Inc. has evolved into a vital cloud-based SaaS provider for the interconnected automotive insurance economy, connecting over 35,000 businesses through its proprietary data-driven platform. The company’s AI integration and network effects underpin robust revenue growth, with 11.9% top-line expansion in 2025, despite profit volatility due to operational leverage and debt-related expenses. Customer concentration and covenant-restricted capital allocation constrain financial flexibility, but continued R&D investment aims to deepen competitive differentiation while expanding into adjacent insurance lines. Key metrics to watch include contract renewals with large insurers, AI adoption rates, and covenant compliance.

Decades of SaaS Evolution Driving Growth in the Insurance Economy

Founded in 1980, CCC Intelligent Solutions has matured into a cloud-centric SaaS powerhouse specifically tailored for the automotive insurance claims and collision repair ecosystem [S1], [S4]. The firm's multi-tenant public cloud platform strategically addresses the “many-to-many” problem intrinsic to these industries by seamlessly connecting insurers, repair facilities (over 30,500), OEMs (14 of top 15 U.S.), parts suppliers (6,000+), and others within an extensive network exceeding 35,000 companies [S4], [S16]. This breadth creates a powerful Direct Repair Program (DRP) network effect: more insurers attract more shops which reciprocally amplify platform value.

Financially, CCC's historical performance reflects consistent top-line growth driven by deepening SaaS adoption across its segments. Revenue rose from approximately $782 million in FY2022 to about $1.06 billion by FY2025 representing a compound annual growth rate around double digits (roughly +11.9% YoY in FY2025) [F1]. Operating income showed a sharp uplift from a loss position (-$24 million) in FY2023 back into positive territory of $93.8 million in FY2025 (+17.1% YoY), suggesting improving operating leverage from recurring subscription revenues and scale efficiency [F1]. However, net income fluctuated significantly culminating in only $1.7 million by FY2025 (-94.6% YoY), influenced by elevated financing costs linked to CCC’s substantial debt load [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1057 | 2 | 315 | 94 | +11.9% | -94.6% |

| 2024 | 945 | 31 | 284 | 80 | +9.1% | +134.7% |

| 2023 | 866 | -90 | 250 | -24 | +10.7% | -334.5% |

| 2022 | 782 | 38 | 200 | 52 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 601 | 255 | |

| 2024 | 0 | 231 | |

| 2023 | 0 | 328 | 195 |

| 2022 | 0 | 152 |

Source: SEC companyfacts cache [F1].

*Latest full year data as of December 31, 2025 [F1].

Note: "OpInc" = Operating Income; "CFO" = Operating Cash Flow; Capex includes both maintenance and growth investments.

Customer retention is strong with average relationships exceeding a decade among leading insurers who represent the majority of CCC’s revenue [S4]. This stability underpins recurring revenue but also exposes CCC to risks should contract dynamics shift abruptly.

Proprietary Data and AI: The Core of CCC’s Competitive Moat

CCC’s platform is distinguished by its mammoth proprietary dataset capturing over $2 trillion in historical transaction volume processed through its systems [S4], combined with cutting-edge application of artificial intelligence across this data set [S26]. The scale of data enables precise event-specific modeling incorporating geographic variables and historical trends — essential for combating claims leakage that can reach sizable proportions in P&C insurance workflows.

More than 400 advanced AI models operate at enterprise scale within CCC’s environment; these models optimize numerous processes from damage estimation via image analytics (handling ~800 million photos annually) to predictive insights for claim outcomes [S4], [S26], [S27]. The underlying technology stack features hyperscale infrastructure supporting billions of daily transactions with robust security protocols yielding consistent system availability exceeding industry norms at about 99.9% uptime since January 2021 [S27].

The multi-tenant cloud architecture supports seamless integration with legacy insurer systems via APIs employing SDKs or HTML5 interfaces tailored for mobile use cases [S23]. Such design permits rapid deployment cycles — average implementations complete within three months — critical for maintaining agility amid fast-evolving regulatory and market demands [S23].

This technical foundation coupled with expansive DRP network effects fosters high switching costs: new entrants face steep barriers given the intertwining insurer-shop relationships required to establish similar ecosystems.

Customer Concentration and Contract Dynamics Impacting Revenue Stability

Despite a broad customer base numerically, a relatively small group of large insurer customers accounts for a disproportionate share of revenue though none exceeded individual revenue contributions above the critical threshold of 10% as of FY2025 [S1], [S7]. Contracts typically span three to five years but can be canceled or non-renewed on relatively short notice post-term expiry [S7].

Large insurers wield meaningful negotiating leverage influencing pricing terms negatively affecting average selling prices, gross margins, and potentially increasing contractual liability risks that CCC must prudently manage [S7]. Pressure from customers demanding customized feature sets or additional integration complexity adds sales cycle friction and cost burdens impacting margin profile.

While long-standing relationships mitigate some risk — with carrier contracts averaging over ten years historically — evolving competitive landscapes including internal insurer technology buildouts pose ongoing threats to client retention or renewal terms [S1], [S27]. Moreover, disputes occasionally arise impacting counterparties' willingness to maintain engagements on existing contractual terms.

Continued vigilance around maintaining brand reputation along with proactive adaptation based on detailed customer feedback loops are crucial strategies deployed by CCC to counterbalance these structural risks [S7].

Financial Trajectory: From Robust Revenue Gains to Earnings Volatility

CCC's financial journey evidences strong topline momentum — nearly doubling revenue since FY2022 at a CAGR near double digits — reflective of successful SaaS subscription expansion into core insurance economy verticals plus adjacent lines added through acquisitions like EvolutionIQ focused on disability claims solutions [F1], [S16].

Operating income showed marked improvement recovering from losses during transitional phases due partly to operating leverage realized as fixed costs spread across rising recurring revenues; however, net income depicts stark volatility primarily attributable to increased interest expenses incurred on substantial term debt alongside amortization charges relating to intangible assets acquired during growth initiatives [F1].

Operating cash flow increased steadily (+11.1% in FY2025), indicating robust underlying cash generation capacity supporting operational needs alongside capital reinvestment commitments especially R&D-directed expenditures contributing towards innovation leadership [F1].

The divergence between net income near breakeven levels versus positive operating results reflects non-cash charges plus financing costs; this nuance underscores the importance of assessing multiple profitability proxies beyond GAAP net income when evaluating SaaS businesses reliant on significant tech investments amid leverage funding structures.

Capital Allocation: Cash Flow Strength Coupled with Significant Buybacks But No Dividends

Strong free cash flow generation—calculated as operating cash flow minus capital expenditures—reached approximately $255 million in FY2025 underpinning active capital return policies despite dividend suspensions post-FY2022 attributed directly to restrictive covenants embedded within the company’s credit agreement governing dividend pay-outs and leverage thresholds [F1], [S6], [S9].

Notably, FY2025 saw aggressive share repurchases totaling over $600 million reflecting management’s confidence in long-term intrinsic value despite cautious distribution constraints imposed externally by lenders.[F1]

Debt structuring includes approximately $1.29 billion outstanding Term B Loan imposing customary affirmative/negative covenants limiting further indebtedness incurrence or asset disposals without lender approval thus constraining strategic flexibility somewhat during uncertain macroeconomic environments or opportunistic acquisition pursuits.[S6]

Liquidity buffers remain adequate given cash balances above $110 million paired with undrawn revolver capacity approximating $249 million enhancing resilience.[F1],[S9]

It is important to note that specific Return on Equity (ROE), dividend yield figures are not directly available from provided tags; however approximate ROE based on latest net income over equity stands at roughly 0.1%, indicating muted equity returns given earnings volatility [F1].

Innovation and R&D Investment as Levers for Future Growth

CCC dedicates substantial resources towards research & development encompassing roughly one-quarter of revenues when accounting for amortized internal-use software capitalization (~27%) highlighting its commitment toward sustaining technological superiority particularly around AI capabilities ported into production environments rapidly reflecting continuous iteration cycles.[S11]

Recent launches such as Medhub targeting Medicaid/insurance integration bottlenecks, Pay Workflow enhancing payment automation within collision shops, OEM Link Network enabling certified repairer marketplaces for automotive manufacturers exemplify broadening functionality aimed at deepening ecosystem entrenchment while capturing incremental wallet share.[S11],[S26]

This investment pattern also aligns with escalating capex outlays which increased approximately +15% YoY signaling expanding infrastructure capacity needs supporting hyperscale compute power requisite for growing AI model deployments at enterprise scale.[F1],[S11]

Marketing efforts focus on consultative sales engagement strategies emphasizing data-driven decision support tools illustrating how CCC proposes tangible reductions in overhead processing costs combined with superior customer experience enhancements driving further software subscription expansions.[S11],[S24]

Evaluating Risks: Debt Covenants and Market Concentration Challenges

The dual challenges posed by concentrated revenue sources alongside considerable leverage remain principal concerns warranting close monitoring going forward.[S1],[S6],[S8],

Although no individual customer exceeded the materiality threshold (>10%), aggregate reliance on top insurers creates vulnerability to adverse contract outcomes provoking sudden revenue declines or downward pricing adjustments undermining margin sustainability.[S7]

Further complicating matters are restrictive debt covenants curtailing dividend resumption or acquisitions absent lender consent that may inhibit strategic flexibility needed during volatile market cycles or emerging competitive disruptions.[S6][S9]

On regulatory fronts heightened scrutiny regarding data privacy compliance laws such as GDPR or CCPA adds layers of operational risk given lifecycle management of sensitive consumer information processed via cloud platforms.[S8], Although robust security controls ensure baseline compliance the dynamic landscape imposes continuous cost burdens that may impact returns if not efficiently managed.

Legal proceedings currently have no material adverse impact but remain an inherent risk vector given complex inter-party contractual interdependencies inherent within multi-vendor platforms spanning diverse geographies.[S15]

Forward-Looking Indicators and Milestones to Watch

Absent explicit forward guidance published recently,[N/A] critical metrics warrant monitoring including:

- Contract renewal rates particularly with top-tier insurers who anchor sizeable portions of recurring revenue;

- Adoption velocity metrics relating to newly rolled-out AI-enabled modules among repair shops influencing usage frequency;

- Progression towards margin expansion reflecting operating leverage realization balancing R&D spending against revenue gains;

- Covenant compliance snapshots reported quarterly serving as early warning signals for liquidity strain or refinancing needs;

- New product launches or strategic partnerships extending into adjacent insurance verticals that broaden addressable market estimates;

- System uptime maintenance at or above current levels signifying platform reliability pivotal for customer trust retention;

- Responses by competitors deploying off-the-shelf AI suites or agentic AI solutions that may erode differentiation over time.

Tracking these indicators will provide clarity regarding sustainability of CCC’s growth trajectory amid evolving macroeconomic backdrop plus sector-specific structural transformations.

Disclaimer: This analysis is intended solely as an informational memorandum summarizing recent publicly available financial reports and SEC filings pertaining to CCC Intelligent Solutions Holdings Inc., illustrating company operations within its specific business context without offering investment recommendations or price predictions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments