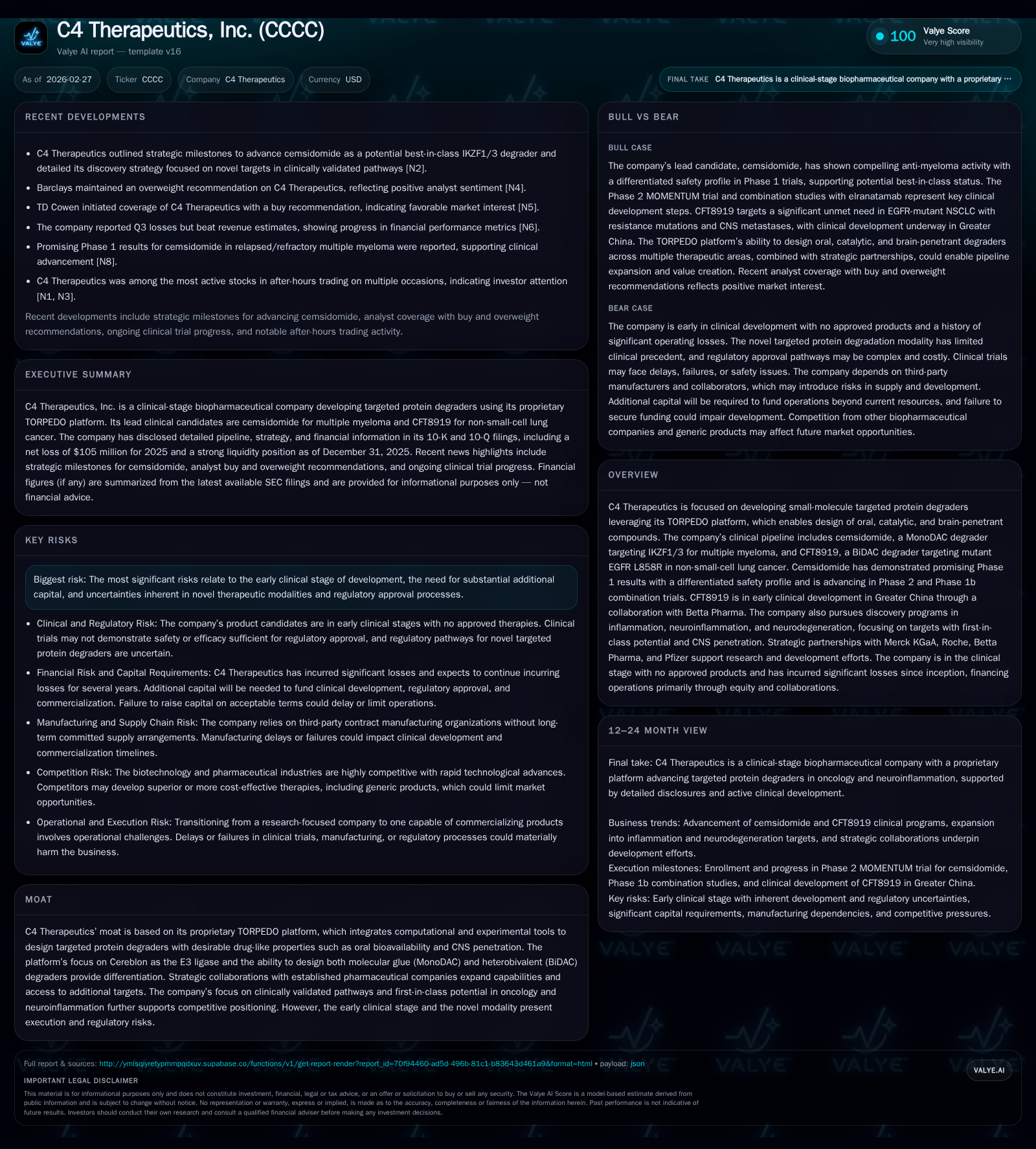

C4 Therapeutics Harnesses TORPEDO Platform in Pursuit of Oncology and CNS Breakthroughs

Clinical-stage biotech C4 Therapeutics leverages its proprietary protein degradation platform to advance oncology and CNS programs amid capital-intensive operations.

C4 Therapeutics operates at the forefront of targeted protein degradation with its TORPEDO platform facilitating oral, catalytic, and CNS-penetrant degraders. The company’s lead candidates, cemsidomide for multiple myeloma and CFT8919 for mutant EGFR-driven lung cancer, are advancing clinical stages supported by promising early data and strategic partnerships. Financially, C4 faces persistent operating losses fueled by heavy R&D spends typical of early-stage biotechs, balanced by a robust cash position and collaborations that enhance pipeline breadth. Investors should monitor upcoming Phase 2/1b trial readouts, ongoing development milestones, and regulatory pathways given the novel modality’s uncertainties.

Growth Journey: From Platform Foundations to Clinical Milestones

C4 Therapeutics has established itself as a clinical-stage biopharmaceutical company focused on its proprietary TORPEDO platform—a computationally powered engine enabling design of catalytic small-molecule protein degraders that are orally bioavailable and capable of penetrating the blood-brain barrier. This platform supports both molecular glue (MonoDAC) degraders like cemsidomide and bifunctional (BiDAC) degraders such as CFT8919.

Financially, the company's operating income reflects substantial but somewhat stabilizing losses: -$115.2 million in FY2025 compared to -$119.6 million in FY2024, marking a modest improvement of approximately 3.7% year-over-year [F1]. Net losses remained largely flat at about -$105.0 million versus -$105.3 million prior year. Operating cash flow outflows increased to -$98.7 million in FY2025 from -$65.2 million in FY2024 [F1]. Capital expenditures were minimal ($607 thousand), underscoring focus on research rather than fixed assets.

This financial profile aligns with expectations for an early-stage biotech prioritizing clinical advancement over commercialization; notably, C4 has not yet generated product revenue [S1]. Progress is driven by advancing cemsidomide beyond Phase 1 safety trials into Phase 2 expansion and Phase 1b combination studies [N1], setting the stage for potential future growth.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -105 | -99 | -115 | 1 | +0.3% |

| 2024 | -105 | -65 | -120 | 0 | +20.5% |

| 2023 | -132 | -107 | -139 | 2 | -3.4% |

| 2022 | -128 | -106 | -130 | 5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 193000 | -99 | -40.9 |

| 2024 | 194000 | -65 | -48.8 |

| 2023 | 110000 | -109 | -53.8 |

| 2022 | -111 | -44.3 |

Source: SEC companyfacts cache [F1].

Table notes: Figures approximate; sourced from company filings [F1].

Overall, these results illustrate a continued commitment to R&D investments underpinning pipeline progression.

Pioneering Protein Degradation: Leveraging MonoDAC and BiDAC Modalities

C4's scientific differentiation centers on the TORPEDO platform which integrates computational design with experimental validation to generate advanced protein degraders using targeted protein degradation (TPD). The platform focuses on Cereblon-mediated ubiquitination enabling both molecular glue (MonoDAC) degraders—small molecules that facilitate proximity between Cereblon E3 ubiquitin ligase and target proteins—and bifunctional Chemically Induced Proximity (BiDAC) degraders linking two ligands to target proteins simultaneously.

MonoDAC compounds like cemsidomide employ a catalytic mechanism allowing repeated degradation without stoichiometric binding, often translating into better efficacy at lower doses clinically observed [N1]. This enhances drug-like properties while minimizing adverse effects—a critical innovation targeting IKZF1/3 transcription factors involved in multiple myeloma pathology.

BiDAC compounds such as CFT8919 enable engagement of challenging targets like mutant epidermal growth factor receptor (EGFR) variants seen in non-small cell lung cancer (NSCLC). CFT8919 is an orally bioavailable allosteric degrader selective for EGFR L858R mutations including resistance-conferring variants like T790M-C797S [S1]. Targeting an allosteric site may reduce resistance risks common to kinase inhibitors.

Strategically, C4 emphasizes CNS penetration within degrader designs to expand beyond oncology into inflammation and neurodegeneration indications where intracellular pathogenic proteins are difficult to target with conventional therapies [N1]. Achieving blood-brain barrier permeability while maintaining catalytic activity represents a significant technical advancement.

Clinical Pipeline Spotlight: Cemsidomide and CFT8919 Progress

Two lead oncology candidates illustrate C4's modality breadth:

Cemsidomide is an orally bioavailable MonoDAC degrader targeting IKZF1/3 transcriptional regulators crucial for multiple myeloma cell survival and immune evasion [S1]. In Phase 1 monotherapy trials combined with dexamethasone, it demonstrated a differentiated safety profile relative to prior immunomodulatory drugs alongside notable anti-myeloma activity in heavily pretreated patients [N1]. These results have led to Phase 2 monotherapy expansions and Phase 1b combination studies exploring synergy across therapy lines.

CFT8919, developed via collaboration with Betta Pharma for Greater China markets [S1], is an innovative BiDAC allosteric degrader targeting mutant EGFR L858R driving NSCLC resistant to first-generation inhibitors due to acquired mutations including T790M-C797S [S1]. Preclinical studies showed strong antiproliferative activity across mutation combinations indicating potential against drug-resistant tumors [N1]. Early clinical data remain pending; outcomes will significantly influence valuation.

These programs address large unmet needs within validated oncologic pathways combining biological rationale with novel modality advantages highlighting C4’s therapeutic innovation capacity.

Navigating Future Prospects and Regulatory Hurdles

Key upcoming inflection points include progression of cemsidomide through Phase 2/1b readouts assessing efficacy signals with acceptable toxicity profiles across combination regimens indicative of commercial viability [N1]. Concurrent developments from CFT8919’s China-based trials will inform global expansion strategies contingent on partnering arrangements.

Beyond oncology, inflammation-related indications leveraging brain-penetrant degraders offer substantial growth opportunities but carry elevated scientific risk given limited precedent for TPD in these areas [N1]. Regulatory pathways pose challenges due to evolving FDA guidelines requiring biomarker characterization and long-term safety monitoring for novel modalities [S4],[S5],[S6]. Reimbursement frameworks are also evolving slowly complicating market access.

Execution risks include managing complex clinical trial scale-up while defending intellectual property amidst competitive therapeutic landscapes featuring modalities like PROTACs and RNA therapies competing for regulatory attention [S12],[S16],[S21]. Government agency funding variability may further delay approvals impacting capital efficiency metrics [S7],[S22].

Financial Health and Capital Deployment: Losses, Cash Buffers, and Shareholder Returns

As of FY2025 year-end, C4’s financial position typifies early-stage biotech investing heavily in R&D without commercial revenues. Net loss stood near -$105 million—stable versus prior year reflecting controlled cost management amid expanding activities [F1].

Operating cash flow outflows grew substantially to nearly -$99 million driven by intensified clinical trial activities requiring outsourced services plus internal staffing increases aligned with pipeline scaling efforts [F1]. Capital expenditures remained minimal (~$607k), consistent with a model focusing on research assets rather than infrastructure ownership.

Cash & equivalents totaled approximately $74.6 million at December 31, 2025 offsetting current liabilities around $33 million yielding a strong current ratio near 7.8—a healthy liquidity buffer reflecting prudent treasury management amid volatile equity markets impacting fundraising during periods without product revenues [F1].

Equity contracted relative to past years consistent with sustained net loss accumulation producing an approximate return on equity near negative ~41%, underscoring ongoing capital consumption absent dividends or material share repurchases given lack of profitability [F1].

This financial snapshot highlights reliance on capital markets access alongside collaborations as critical lifelines preserving runway through key biological validation phases.

Strategic Collaborations Driving Pipeline Expansion

C4 expands discovery reach via curated alliances enhancing scientific depth and geographic presence:

- Partnership with Merck KGaA supports joint oncology/non-oncology programs sharing risk/reward;

- Collaboration with Roche deepens inflammation-related degrader exploration beyond oncology focus;

- Betta Pharma partnership delegates regional development responsibilities for CFT8919 unlocking Greater China access while easing internal resource demands;

- Pfizer collaboration leverages complementary expertise underscoring pharma incumbents’ interest in protein degradation platforms [N1],[S1].

These alliances diversify pipeline enrichment while externalizing costs buffering solo cash burn enhancing validation credentials crucial during early-stage biotech valuation.

What Investors Should Watch Next: Key Catalysts and Risk Factors

Upcoming catalysts pivotal for valuation shifts include:

- Data from cemsidomide Phase 2 monotherapy expansions plus combinational arms probing additive synergy;

- Initial efficacy outcomes from Betta Pharma-led CFT8919 trials informing Chinese launch prospects and global regulatory strategies;

- Milestones from exploratory inflammation/neurodegeneration programs employing CNS penetrant MonoDAC/BiDAC compounds potentially unlocking first-in-class status;

- Capital raises necessitated by negative free cash flow near $99 million constraining runway absent partnering or licensing revenues;

- Navigating FDA approval complexities tied to novel TPD modalities involving long-term safety monitoring, payer reimbursement variability, and evolving IP landscapes limiting competitor encroachment ,,.

Together these elements balance scientific promise against execution risks inherent to capital-intensive biotechnology investments.

Disclaimer: This analysis summarizes publicly available information as of February 2026 without providing investment advice or recommendations regarding securities trading or portfolio allocation concerning C4 Therapeutics.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments