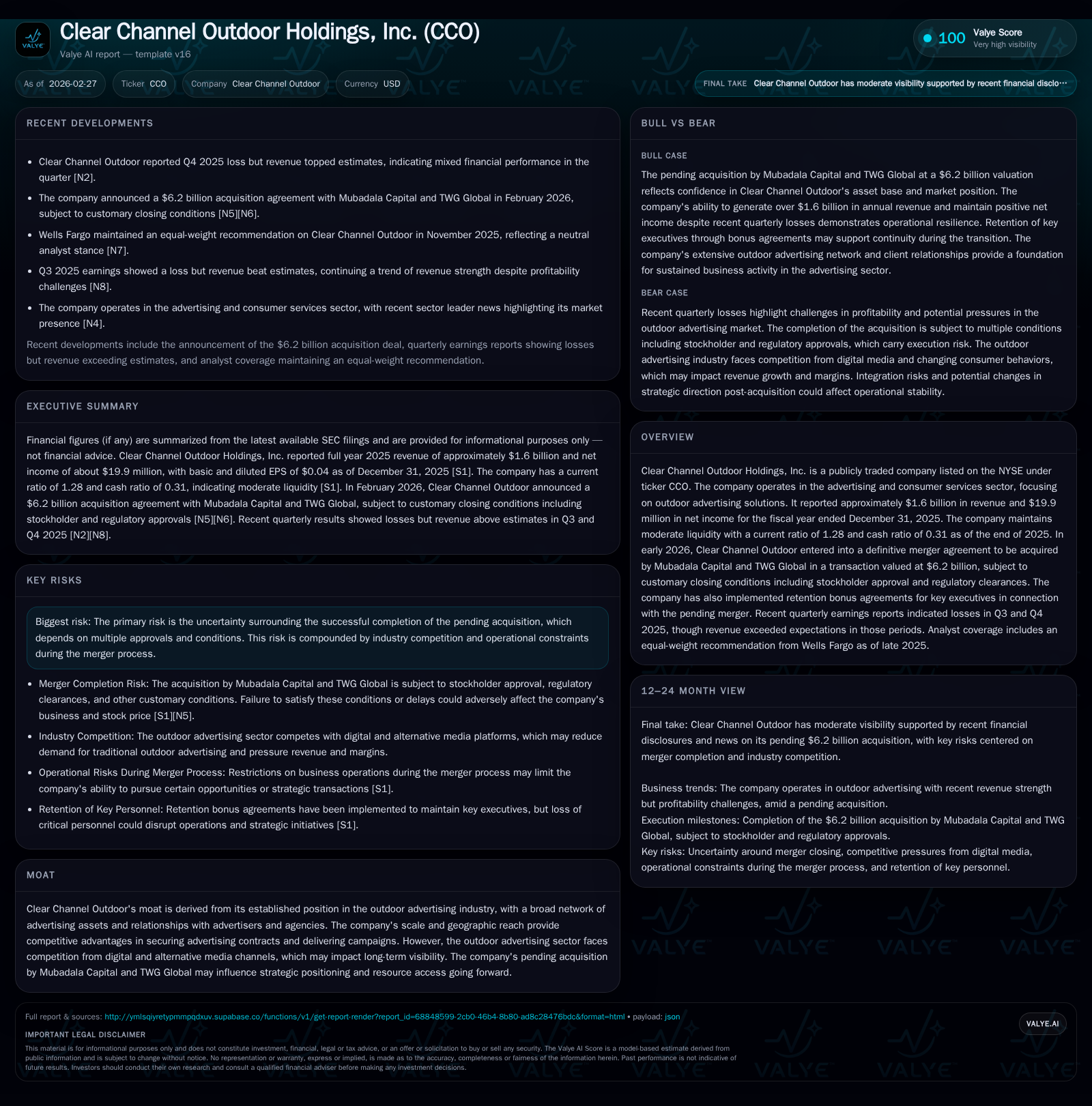

Clear Channel Outdoor’s Financial Turnaround Signals Strategic Inflection Ahead

A rebound in Clear Channel Outdoor's operating performance and a pending $6.2 billion acquisition underscore a pivotal moment for the outdoor advertising giant.

Clear Channel Outdoor Holdings, Inc. delivered a notable improvement in fiscal 2025 financial metrics, reversing prior years' volatility with a strong operating income surge to $311 million on $1.6 billion in revenue. This operational recovery comes as the company agreed to a $6.2 billion acquisition by Mubadala Capital and TWG Global, which hinges on regulatory and shareholder approvals. Capital allocation trends reveal improved free cash flow generation amid declining capital expenditures and an absence of recent dividends or buybacks, reflecting merger-related strategic priorities. The acquisition and ongoing digital disruption in out-of-home advertising set the stage for transformation but carry execution risks tied to integration and market competition.

From Volatility to Growth: Tracing Clear Channel’s Recent Financial Performance

Clear Channel Outdoor Holdings has experienced pronounced fluctuations over recent years before demonstrating a strong turnaround in its fiscal year ended December 31, 2025. Revenue jumped sharply to approximately $1.6 billion in FY2025, up nearly 276% from the prior year’s $427 million figure—reflecting a recovery from steep declines witnessed since FY2022 [F1]. Operating income exhibited an even more pronounced rebound, increasing over twofold year-over-year to approximately $311 million in FY2025 from $100 million in FY2024 [F1]. While net income remained modest at just under $20 million, this marked an important inflection point after losses in both FY2024 (-$17.9 million) and FY2022 (-$96.6 million) [F1].

Operating cash flow also trended upward sharply, rising by 44% year-over-year to reach roughly $115 million last fiscal year, supported by strategic cost containment initiatives and revenue stabilization. Concurrently capital expenditures fell substantially, down almost 42% compared with FY2024 levels, enabling an improved free cash flow position approaching $32 million for FY2025 [F1]. The following table summarizes key annual financial metrics:

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1.6 | 20 | 115 | 311 | +275.9% | +211.5% |

| 2024 | 0.4 | -18 | 80 | 100 | -32.5% | -172.2% |

| 2023 | 0.6 | 25 | 31 | 124 | -74.5% | +125.6% |

| 2022 | 2.5 | -97 | 140 | 232 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) |

|---|---|

| 2025 | 32 |

| 2024 | -63 |

| 2023 | -135 |

| 2022 | -45 |

Source: SEC companyfacts cache [F1].

Note: Fiscal years indexed per calendar year; 'Revenue YoY %' indicates percentage change versus prior fiscal year where available.

This volatility pattern reflects lingering industry challenges coupled with company-specific factors including macroeconomic conditions impacting advertising spending.

Drivers Behind the Fiscal Uplift: Operational Efficiencies and Revenue Expansion

Several forces appear responsible for Clear Channel Outdoor's fiscal rebound in FY2025. On the top-line front, the company leveraged its extensive asset base across billboards, transit shelters, airports, and other out-of-home (OOH) media placements to regain advertising spend traction despite increasing digital competitors [N1][N2]. The scale advantage inherent in Clear Channel’s geographic footprint likely helped secure renewed advertiser commitments and campaign volume.

Operational efficiencies also played a critical role; management highlighted cost reductions along with improved campaign yield driving operating margin expansion despite the sector-wide shift toward programmatic digital buying modalities that fragment demand [S1][N2]. The impact of retention bonus agreements instated for key executives during merger preparations may have bolstered management stability during this transition period [S11][S23], facilitating tighter expense controls.

While still modest relative to revenues, net income positivity signals emerging operational discipline following losses over the previous three fiscal years.

The $6.2 Billion Takeover: Strategic Rationale and Transactional Details

In February 2026, Clear Channel Outdoor publicly announced it had entered into a definitive merger agreement with Mubadala Capital and TWG Global consortium for approximately $6.2 billion in aggregate consideration [N3][N4][S3][S12]. The deal values shares at $2.43 each in cash without interest at closing subject to standard conditions including stockholder approval and regulatory clearances such as under Hart-Scott-Rodino antitrust review and CFIUS scrutiny due to international investor involvement [S14].

Mubadala Capital’s deep pockets and international investment perspective paired with TWG Global's strategic advertising sector knowledge underpin the prospective value creation thesis centered on leveraging Clear Channel’s historic OOH media leadership while investing through digitization of assets and data capabilities [N4]. The agreement contains a “go-shop” provision allowing the company limited time until March-end to entertain superior proposals subject to termination fees clauses [S14][S21].

Capital Allocation Trends: Cash Flow, Dividends, and Shareholder Returns in Transition

Capital deployment strategies reflect Clear Channel’s strategic prioritization of organic recovery alongside merger value maximization. While operating cash flows improved significantly—from approximately $80 million in FY2024 to $115 million in FY2025—capital expenditures retreated sharply from $142 million down to about $83 million over the same period enhancing free cash flow generation (~$32 million) [F1]. This capex reduction likely signals a pause or reprioritization of investments ahead of ownership transition.

Dividend distributions have been minimal or absent recently; last meaningful dividend payments date back several years ago with no comparable dividends declared through the latest reported periods [F1][S7][S24]. Similarly, share repurchases have been sporadic at best during recent cycles indicating preserved capital for strategic transactions rather than returning cash directly to shareholders currently.

Retention bonus payouts totaling hundreds of thousands allocated among senior executives reinforce emphasis on leadership continuity through acquisition completion steps [S11][S23]. Liquidity metrics remain moderate with current ratio at about 1.28 supported by ~$190 million cash balance as of December-end FY2025 although leverage details are less publicly detailed due to transaction context [F1][S8][S9].

Future Growth Path: Integration Challenges, Market Position, and Competitive Risks

While merger approval could unlock new resource influxes fueling growth initiatives especially around digital transformation within OOH platforms, several risks loom large post-closing. Foremost are uncertainties related to successfully satisfying all regulatory clearances without onerous conditions potentially delaying or modifying deal terms [S14][S29]. Moreover, integration execution risks remain given priorities around harmonizing operations between incumbent management structures and consortium objectives.

Externally clear challenges stem from intensifying competition by digital ad formats capturing budget share traditionally earmarked for static outdoor media placements; consumer behavior patterns increasingly favoring mobile-first targeting models impact demand dynamics across urban versus suburban locations [N4][S10]. Maintaining advertiser relationships amid this evolving competitive landscape requires agility around programmatic advertising uptake and data analytics — areas where Clear Channel has been investing but faces legacy integration hurdles.

Watchpoints Ahead: Merger Milestones and Regulatory Approvals

Critical near-term events center around securing affirmative shareholder vote expected through dedicated proxy materials forthcoming post-merger announcement [S14][S15]. Regulatory timelines include waiting period expirations under Hart-Scott-Rodino followed by interagency Committee on Foreign Investment evaluations due to cross-border capital inflows inherent in Mubadala/TWG consortium [N3][N4][S14].

The "go-shop" provision sets March-end deadline for exploring alternative proposals before exclusivity tightens reinforcing urgency around these milestones impacting share price trajectories and operational planning consistency during transition windows.

This analysis is based strictly on publicly available information as of February 27, 2026, including SEC filings and press releases related to Clear Channel Outdoor Holdings’ financial results and pending acquisition transaction documented therein. It does not constitute investment advice or solicitation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments