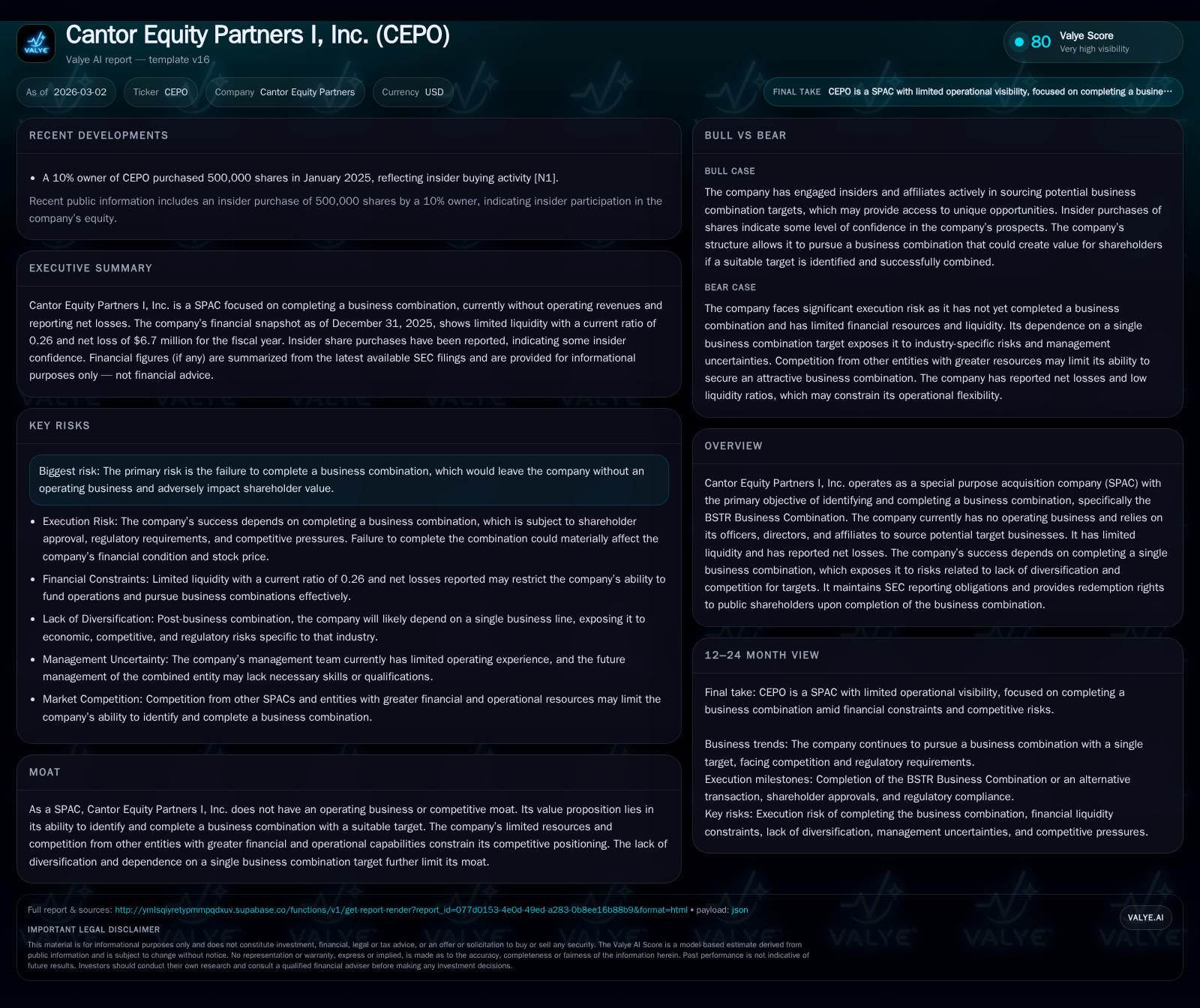

Cantor Equity Partners I’s Growth Hinges on BSTR Business Combination Execution

A SPAC with no operating business, CEPO’s future depends on completing a single business combination amid limited liquidity and competitive pressures.

Cantor Equity Partners I, Inc. (CEPO) functions as a special purpose acquisition company (SPAC) focused on executing the BSTR Business Combination. Historically, it has recorded net losses and limited operational activity due to its structure and mission. The company has minimal cash outside its Trust Account, with financial performance reflecting mostly pre-combination expenses. Its growth prospects wholly depend on consummating the targeted business combination; failure to do so would lead to liquidation and shareholder redemption at roughly the Trust Account value. Capital allocation is centered on completing the business combination using cash held in Trust, with no dividends or buybacks planned. CEPO faces significant competition from other SPACs and acquisition entities with greater resources.

Company Overview

Cantor Equity Partners I, Inc. (ticker: CEPO) operates as a special purpose acquisition company (SPAC) incorporated in the Cayman Islands. It exists solely to effectuate a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination (the "Business Combination") with one or more businesses, specifically targeting the so-called BSTR Business Combination [S1]. Until such a transaction closes, CEPO maintains no operating business or assets aside from those held in its trust account.

Historical Performance and Financial Results

Reflecting its SPAC structure and status as a public shell company awaiting combination, CEPO's historical performance shows minimal operating activity but consistent net losses attributable mainly to general and administrative expenses.

According to recent filings through fiscal year-end December 31, 2025, the company incurred net losses of approximately $6.66 million for FY2025 versus just $84 thousand loss in FY2024 — a steep increase relative to inception period levels reflecting increased costs related to pursuing its target transaction [F1]. Operating income for FY2025 was negative by about $974 thousand.

Cash flow from operations turned modestly positive in FY2025 at $52,578 after negative operational cash flow of -$134 thousand in FY2024; however this remains low given absence of any core revenue-generating activities [F1].

The balance sheet reveals highly constrained liquidity: current assets stood near $212 thousand by December 2025 against current liabilities approximating $800 thousand — translating to a current ratio around 0.26 [F1]. Earlier quarterly reports indicated about $275 thousand cash & equivalents as of Q1 2025.

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | Net YoY |

|---|---|---|---|

| 2025 | -7 | 52578 | -7787.2% |

| 2024 | 0 | -134240 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 39.7 |

| 2024 | 103.4 |

Source: SEC companyfacts cache [F1].

Net income worsened sharply in 2025 mainly due to increased pursuit and administrative costs associated with the Business Combination process.

Future Growth Prospects

Future growth for CEPO critically hinges on successfully completing the BSTR Business Combination or alternatively another suitable target within its allowed combination period [S1][S16]. If consummated:

- CEPO transitions from an empty shell into an operating entity.

- Access to ongoing revenue generation and growth pathways becomes viable through the acquired business.

However, no operational revenues or growth drivers exist currently since CEPO's asset base is primarily cash reserved for the deal funding held in trust.

If the BSTR combination fails:

- The company may consider business combinations with other targets that were previously evaluated by affiliated Cantor-sponsored SPACs.

- Failing any combination by deadline leads to mandatory liquidation and redemption of Public Shares at approximately $10.53 per share based on Trust Account balances plus accrued interest less potential claims [S7][S9][S13].

This all-or-nothing setup exposes shareholders to concentration risk absent diversification. Competing SPACs with deeper pockets or more experienced sponsors also constrain CEPO's competitive positioning in securing desirable deals [S26].

Forecasts and Milestones

Explicit guidance regarding timing for completion of the BSTR Business Combination has not been disclosed beyond statutory deadlines placed on the SPAC structure under SEC rules [S12].

Key upcoming milestones include:

- Shareholder meeting(s) for approval of the Business Combination if required,

- Execution of redemption rights process for Public Shareholders,

- Closing of financing tranches supporting the transaction including any private placement investments as disclosed,

- Transition into an operating company post-close.

Market filings indicate planned issuance of Class A ordinary shares post-combination along with convertible notes and preferred stock linked to private placement investments financing parts of the deal consideration [S25][N/A].

Analysts should track proxy statements proxy filing dates closely having implications for shareholder votes and redemptions [S8][S14][S27].

Returns and Capital Allocation

Due to lack of ongoing operations or earnings-generating businesses pre-combination, traditional profitability metrics like ROE are not meaningful outside anomalous accounting effects from accumulated losses.

Nonetheless by dividing FY2025 net income by equity (-$6.66 million / -$16.78 million), one derives an approximate 39.7% ROE figure; this is mathematically interesting but practically irrelevant given negative book equity largely reflecting unrealized expenses rather than substantive profit [F1].

CEPO does not pay dividends nor have any share repurchase programs prior to consummation of its Business Combination — all capital allocation is dedicated toward deal-related expenses and preservation of cash held primarily within its Trust Account earmarked for shareholder redemptions or transaction financing support [S4–S18].

Sponsor arrangements ensure founder shares are excluded from redemption rights while private placement shares contribute capital but lack guarantees if liquidation occurs [S7][S13].

The ability for sponsor affiliates or officers/directors to purchase Public Shares privately exists as mechanism to reduce redemptions thereby facilitating completion — though no current plans exist for such transactions [S11].

Post-business combination capital strategy will depend heavily on acquired entity's operating cash flows and strategic plans which have yet to materialize.

Risks Summary

CEPO faces substantial risks typical for SPAC vehicles:

- Failure to complete any qualifying business combination triggers mandatory dissolution leading to return of funds less transaction costs,

- Competition from better-capitalized SPACs constrains target access,

- Limited liquidity outside escrowed funds restricts flexibility,

- Potential claims against Trust Account assets could diminish per-share redemption values,

- Dependency on founder/sponsor voting commitments introduces governance risk,

- Market volatility and regulatory uncertainties around SPAC structures may impact deal economics.

Additionally governance and fiduciary duties during transition periods require careful navigation given potential conflicts inherent between sponsor interests and public shareholders [S12][S19–20].

Industry Context (Analysis)

While industry specifics are undeclared for CEPO itself as a non-operating shell entity focused purely on M&A execution, the broader SPAC sector is undergoing regulatory scrutiny post recent market influxes across multiple sectors including technology, investment vehicles face tightening rules around redemption rights and disclosures. This backdrop tightens timelines for transaction completion while increasing due diligence complexity for sponsors like Cantor Equity Partners I.

Conclusion

Cantor Equity Partners I stands at a decisive inflection point reflective of its pure-play SPAC identity: success entirely dependent upon sealing the targeted BSTR Business Combination within prescribed timelines. Historical financial performance underscores inherent challenges without operational revenues; capital allocation remains conservatively anchored toward consummating this single transformational event. Monitoring proxy filings, redemption tenders, sponsor transactional activities alongside competitor movements offers key insight paths into CEPO’s trajectory over coming months.

This analysis is prepared solely for informational purposes referencing publicly available filings up to March 2, 2026. It contains no investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments