Cantor Equity Partners V Strengthens Board While Seeking Initial Business Combination

Latest quarterly update confirms stable pre-combination status as CEPV bolsters its governance with a strategic board appointment.

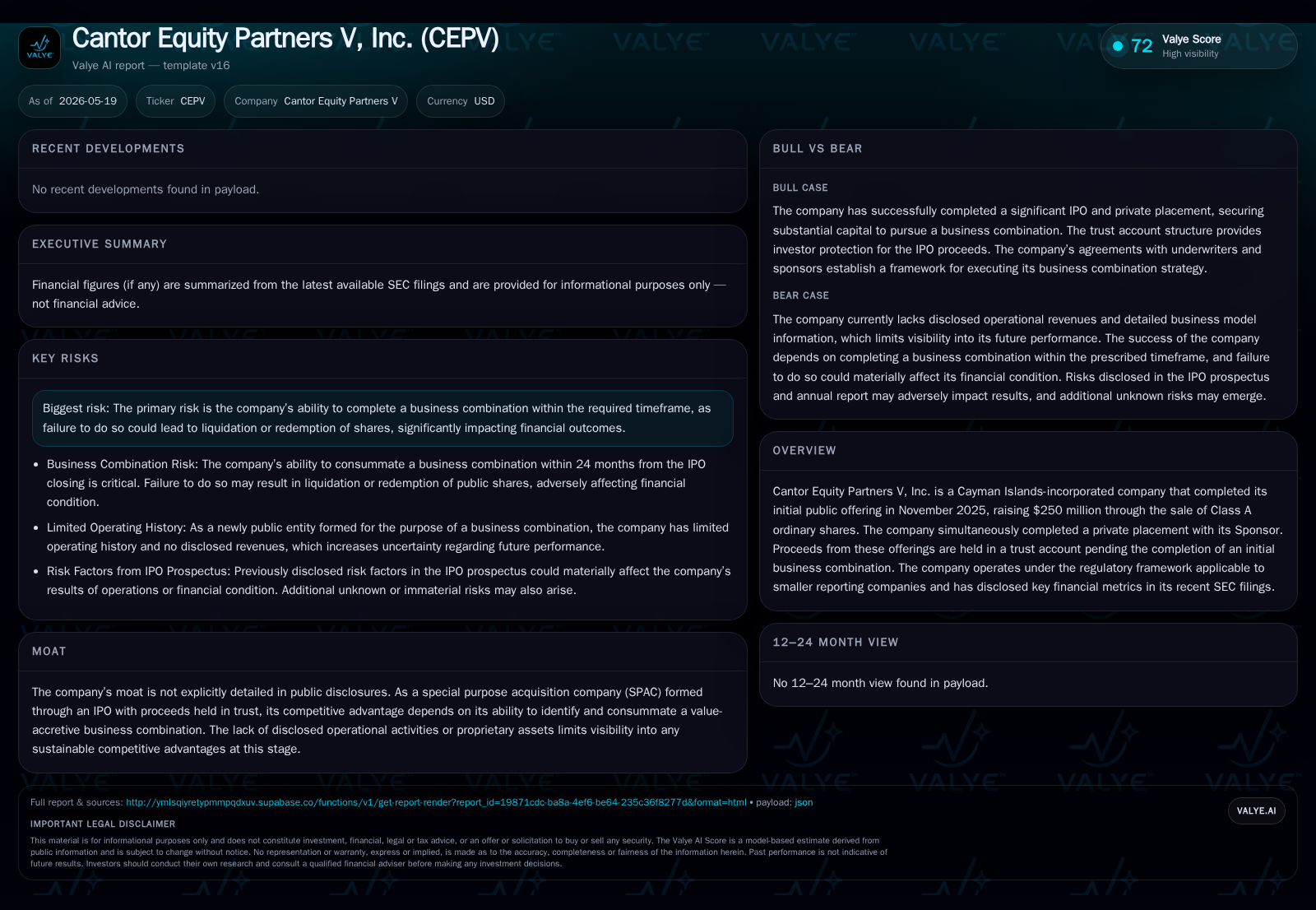

Cantor Equity Partners V, Inc. (CEPV), a Cayman Islands-based SPAC, remains on track toward completing its initial business combination following its November 2025 IPO that raised $250 million. The company’s latest 10-Q filing as of May 2026 reports no material changes in risk factors or operational status, with IPO proceeds securely held in trust. Recent governance enhancements include the appointment of marketing and luxury sector veteran Charlotte Blechman to the board, signaling strengthened oversight as CEPV pursues merger opportunities in targeted sectors including fintech and technology. While the SPAC structure inherently hinges on successful deal consummation within prescribed timelines, CEPV leverages Cantor’s financial services ecosystem for sourcing and vetting acquisitions.

Latest Operating Update: Quarterly Filing Signals Stable Pre-Combination Status

Cantor Equity Partners V, Inc.’s May 14, 2026 10-Q filing offers a snapshot of steady operational footing ahead of its critical milestone—the completion of an initial business combination. As a smaller reporting company under SEC Rule 12b-2, CEPV is relieved from comprehensive risk factor disclosures but affirms that there are no material changes in risks disclosed at IPO or in its annual report filed March 31, 2026 [S2]. Moreover, the company maintains its initial public offering proceeds securely in a U.S.-based trust account pending transaction execution—a typical SPAC safeguard preserving shareholder capital until merger completion [S9]. This static operating posture underlines CEPV's current role solely as an acquisition vehicle without active operating revenues or expenses beyond administrative costs.

Corporate Structure and SPAC Business Model Overview

Incorporated as a Cayman Islands exempted company in April 2021, Cantor Equity Partners V is a "blank check" entity focused on effecting an initial business combination primarily within financial services, digital assets, healthcare, real estate services, technology, and software industries [S1]. The $250 million gross proceeds from the November 2025 IPO alongside $5.4 million from the Sponsor’s private placement are held in trust pending investment deployment [S7]. CEPV’s executive leadership is anchored by Brandon G. Lutnick as Chairman and CEO since February 2025 and Jane Novak as CFO since October 2017; both bring substantial experience within Cantor’s network emphasizing financial markets and accounting policy expertise.

The business model centers on identifying an attractive private company for public listing via merger while offering early investors the option to redeem shares before consummation. Revenue generation post-combination will hinge on its selected target's operations rather than from standalone activities during this pre-combination phase. Margins remain non-existent until an operating company is acquired. This SPAC structure inherently creates an incentive alignment focused on deal completion but carries an embedded risk if no suitable transaction is consummated within the stipulated timeframes.

Governance Enhancements Through Strategic Board Appointments

March 2026 saw Cantor Equity Partners V augment its board capabilities by appointing Charlotte Blechman as a Class I director, concurrently assigning her roles on the Audit and Compensation Committees [S3]. Ms. Blechman brings deep expertise in marketing, branding, digital/social marketing, and luxury lifestyle sector consulting—skills which complement traditional financial acumen within the boardroom context [S16]. Her previous leadership roles at luxury brands such as Tom Ford Retail LLC and Barneys New York combined with advisory experience across several Cantor-affiliated SPACs position her to contribute meaningful oversight particularly around communications strategies that could be pivotal post-business combination. This board strengthening suggests heightened focus on governance quality as CEPV progresses through the deal-sourcing phase.

Competitive Landscape of SPACs and Peer Context in Financial Ecosystem

CEPV operates within the crowded but specialized SPAC niche sponsored by affiliates of Cantor—an established diversified firm with strong footholds across financial brokerage (CF&Co.), electronic market-making (BGC Group), and commercial real estate services (Newmark Group) [S1]. This interconnected ecosystem facilitates robust deal-sourcing channels but also introduces complexity regarding management attention allocation among multiple Cantor-sponsored vehicles concurrently seeking business combinations. To address potential conflicts among affiliated SPACs competing for overlapping targets, CEPV adheres to internal protocols guiding fair opportunity distribution based on IPO timing and explicit permissions—reflecting an effort to balance synergy capture against dilution risks or deal cannibalization.

Without distinctive proprietary assets or operating history pre-merger, CEPV’s competitive edge lies largely in its access to Cantor expertise and network rather than standalone scalability or differentiated product offerings.

Growth Drivers Anchored in Business Combination Execution and Target Industry Focus

The foremost growth catalyst for Cantor Equity Partners V is successfully negotiating and closing an initial business combination that offers accretive value creation for shareholders [S1]. Target sectors such as fintech/digital assets leverage high growth trajectories driven by structural shifts towards decentralized finance solutions and technology-enabled services. Healthcare remains resilient amid demographic trends while real estate services integrate increasingly with technology platforms creating digitization demand. Post-combination value creation depends critically on selecting businesses with scalable models capable of leveraging capital markets access through public listing.

The availability of $250 million plus sponsor contributions provides a solid capital foundation enabling broad transactional flexibility; however, ultimate growth hinges entirely on patterning strategy execution through the business combination milestone rather than organic operational initiatives during the blank check phase.

Risks and Challenges Surrounding Time-Constrained Business Combination Goals

CEPV's primary risk revolves around the regulatory deadlines inherent to SPAC structures: failure to close a qualified business combination within approximately two years triggers liquidation or redemption mechanisms which could result in return of capital at less favorable terms or extinguishing investor stakes entirely [S2]. Additional uncertainty emerges from evolving market environments which may constrain deal pipelines or valuation frameworks adversely impacting negotiation leverage.

Redemption rights granted to public shareholders introduce dilution complexity if significant redemption activity occurs post-announcement thereby altering deal economics unfavorably. Moreover, competition among affiliated Cantor-sponsored SPACs necessitates vigilant conflict management lest overlapping pursuits dissipate focus or precipitate suboptimal asset allocation.

Key Milestones and Monitoring Points Before Combination Deadline

Market participants should closely watch for discrete events signaling progress toward merger closure including:

- Formal announcement of identified acquisition targets,

- Proxy materials detailing terms of proposed combinations,

- Scheduled shareholder votes approving mergers,

- Redemption rates following proxy announcements,

- Subsequent quarterly filings providing updated guidance or risk disclosures,

- Possible further board appointments enhancing strategic capacity. These milestones represent tangible markers differentiating execution momentum from inertia impacting valuation visibility.

Brief Financial Profile: Cash Position and Asset Considerations

Financially, CEPV remains conservatively positioned with approximately $25,000 in cash and equivalents as of March 31, 2026 after segregating IPO proceeds into trust arrangements dedicated exclusively for future business combinations [F1]. Current assets stand around $218.7 million reflecting cash plus nominal non-cash components typical in pre-operating entities. Operating income figures are negative attributable primarily to administrative expenses standard across blank check companies prior to transaction completion reported at approximately -$187 thousand at end-2025 [F1]. Net income figures reflect non-operating gains consistent with trust interest accruals but do not indicate ongoing operating profitability absent completed deals. Overall liquidity posture is adequate for near-term obligations supporting sustained search efforts supplemented by sponsor arrangements.

This analysis strictly summarizes known facts from recent regulatory filings without speculative commentary on prospective transactions or target specifics beyond evidentiary disclosures. Cantor Equity Partners V remains fundamentally a capital-raising vehicle contingent upon external acquisition execution whose success derives heavily from sponsor expertise within targeted industries.

Financial position in context

As of 2026-03-31, companyfacts shows $25,000 in cash and equivalents [F1]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments