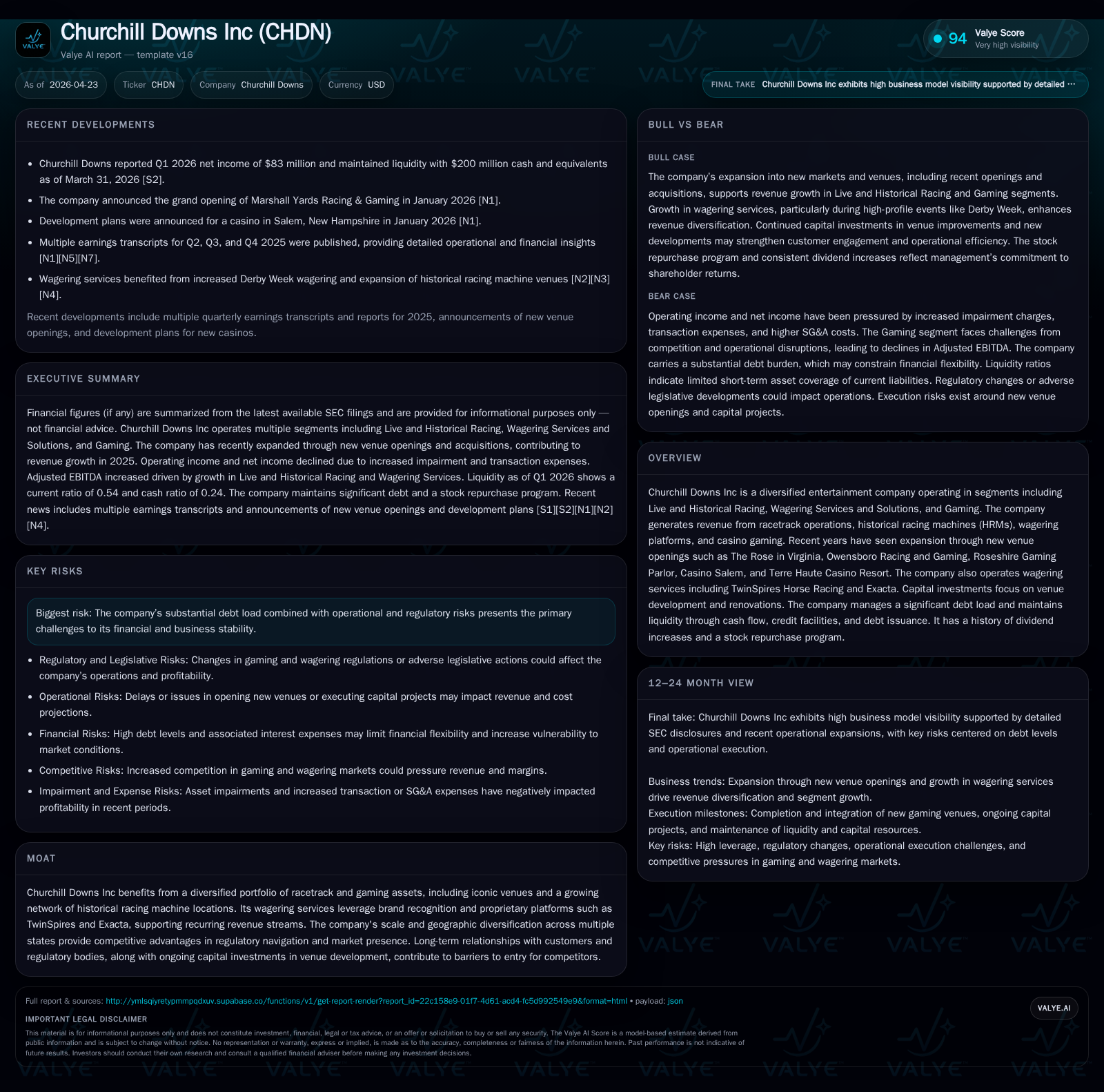

Churchill Downs Expands Venue Portfolio While Managing Elevated Debt and Competitive Pressures

Strong revenue growth from new venue openings contrasts with margin pressure amid rising impairment charges and financial leverage.

In its latest quarterly filing, Churchill Downs Inc (CHDN) highlighted ongoing expansion with new venue openings that boosted revenue notably. However, the company faces margin compression from increased impairment expenses, especially related to Chasers' gaming rights, and a significant debt burden that shapes liquidity strategies. Its diversified business model spans live racing, historical racing machines, wagering platforms, and casino gaming—anchored by iconic venues and digital services like TwinSpires. Growth drivers include geographic expansion and wagering growth but are constrained by regulatory complexities and fixed cost structures. Upcoming milestones focus on execution of capital projects and debt management amidst evolving consumer demand patterns in leisure and gaming.

Recent Operating Update

Churchill Downs Incorporated's latest quarterly filing dated April 22, 2026 [S2][S3] portrays a company actively expanding its footprint while grappling with financial pressures. Revenue growth continues to be fueled by recently opened venues such as The Rose in Virginia (Nov 2024), Owensboro Racing and Gaming (Feb 2025), Roseshire Gaming Parlor (Sept 2025), Casino Salem (Aug 2025), and Terre Haute Casino Resort (April 2024). These assets collectively enhanced the Live and Historical Racing segment revenues significantly.

However, the reported operating income reflects headwinds primarily from an increased impairment expense of $43.6 million mostly tied to the gaming rights of the Chasers Poker Room—an adjustment that notably depresses profitability [S1]. Additionally, transaction expenses rose by roughly $17 million, alongside incremental selling, general & administrative (SG&A) costs. Despite operational gains at new venues and wagering service platforms like TwinSpires during key events such as Derby Week, these factors weighed on overall margin performance.

Liquidity remains supported by stable cash flow from operations supplemented by a sizable revolving credit facility ($1.2 billion capacity) and ongoing access to capital markets through senior notes [S4–S7]. The company is actively managing debt maturities extending through 2031 amid volatile market conditions.

Business Model Overview

Churchill Downs Inc operates across three major segments:

Live & Historical Racing: This segment encompasses traditional racetrack operations complemented by historical racing machines (HRMs) deployed broadly across multiple states. HRMs serve as a steady cash flow source less sensitive to weather or seasonality than live events.

Wagering Services & Solutions: Through proprietary platforms like TwinSpires Horse Racing and Exacta wager services, CHDN caters to a growing online betting demographic. These digital offerings hinge on brand loyalty cultivated via major live events like the Kentucky Derby.

Gaming: The company manages casinos featuring slot machines and table games including recently acquired properties such as Casino Salem. This segment benefits from cross-promotional opportunities with racing venues but faces competitive pressures from regional casinos.

Revenue generation mixes live event attendance fees, pari-mutuel wagering commissions, HRM payouts/net machine revenue splits, subscription/vendor fees for wagering technology solutions, and net casino win.

The presence of brand equity associated with flagship properties—most notably Churchill Downs Racetrack—offers intense customer loyalty advantages that underpin recurring revenue models. Additionally, multi-state geographical reach allows CHDN to diversify risk related to state-specific regulatory changes or economic fluctuations.

Industry Structure & Competitive Position

The racing and gaming industry is fragmented with several regional operators competing for discretionary entertainment dollars amid regulatory oversight that varies materially by jurisdiction. Churchill Downs’ competitive strengths lie in:

- Scale & Geographic Diversification: Operations span different states allowing mitigation of localized economic downturns or regulation shifts.

- Iconic Brand & Signature Events: The Kentucky Derby stands unique globally as both a sport spectacle and a wagering magnet driving online betting traffic year-round.

- Proprietary Digital Wagering Platforms: TwinSpires provides cost-effective customer acquisition plus retention mechanisms critical in an industry leaning heavily toward online betting channels.

- Integrated Venue Network: Synergies between racetracks, casinos, HRM locations enable cross-promotion enhancing customer spend per visit.

Nevertheless, competition intensifies from newly legalized sports betting in adjacent markets and purely digital sportsbooks requiring constant innovation. Also noteworthy are fluctuating consumer preferences amid younger generations shifting away from traditional horse racing towards other forms of entertainment.

Growth Drivers & Constraints

Growth Drivers:

- Venue Expansion & Renovations: Substantial capital allocation toward developing new properties (e.g., Roseshire) fuels incremental market share gains.

- Digital Wagering Uptake: Increasing consumer acceptance of online betting supports top-line growth particularly during marquee race weeks.

- Cross-Selling Opportunities: Integrated offerings spanning live events to casino gaming optimize lifetime customer value.

Growth Constraints:

- Regulatory Complexity: Compliance across multiple state jurisdictions requires costly legal infrastructure limiting rapid scaling.

- Operational Leverage Impacted by Fixed Costs: Weather dependence affects attendance at live races causing variability in event-day revenues despite fixed overhead commitments.

- Debt Servicing Burden: Elevated leverage constrains free cash flow availability for reinvestment or strategic acquisitions [F1][S4–S8].

- Impairment Risks: Asset valuations affected by shifting market dynamics require periodic write-downs impacting reported earnings fidelity.

What To Watch Next

Investors should monitor several operational milestones including:

- Execution progress on venue expansions scheduled for completion over the next twelve months;

- Quarterly wagering volume trends during peak periods like Kentucky Derby week that indicate consumer engagement;

- Regulatory developments potentially altering permissible gaming activities or taxation;

- Refinancing activity around large senior note maturities scheduled from 2027 onward impacting interest expense profiles;

- Impairment reviews related to underperforming assets like Chasers’ gaming rights signaling potential asset reallocation needs.

Digital platform user base growth rates will also serve as early indicators of sustainable organic expansion beyond brick-and-mortar venues.

Financial Profile Summary

Based on the data available up to full-year 2025 ([F1], [S1]):

Historical performance (annual)

| FY | Net ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|

| 2025 | 383 | 684 | -10.3% |

| 2024 | 427 | 709 | +2.3% |

| 2023 | 417 | 564 | -5.0% |

| 2022 | 439 | 322 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 31 | 428 | 37.9 |

| 2024 | 29 | 186 | 39.4 |

| 2023 | 27 | 56 | 46.7 |

| 2022 | 26 | 175 |

Source: SEC companyfacts cache [F1].

Key observations:

- Revenue grew strongly in 2025 driven primarily by recent venue openings contributing over $169 million incrementally [S1].

- Operating income declined modestly due to impairments and transaction-related expenses despite underlying operational improvements.

- Net income dropped more sharply reflecting increased non-cash impairments alongside higher interest expenses attributable to growing debt levels [S1][F1].

- Operating cash flow remains healthy supporting capital expenditure programs focused on strategic growth initiatives.

- Capital allocation shows sustained shareholder returns through dividends (15th consecutive year of increases) coupled with significant share repurchase activity signaling confidence in long-term value creation [S9][F1].

Liquidity metrics remain constrained with a current ratio below unity (~0.54), suggesting tight short-term obligations relative to current assets at quarter end [F1]. Debt maturities peak significantly post-2027 requiring continued access to credit markets or internal cash generation for refinancing needs [S5–S7].

Conclusion

Churchill Downs Incorporated’s recent quarterly disclosures reveal a dynamic phase of investment-led growth reinforced by long-standing brand strength within horse racing and gaming entertainment sectors. Yet challenges persist from margin pressures tied primarily to impairment write-downs and heavy financial leverage amplified by aggressive capital deployment.

The firm’s multi-channel revenue streams rooted in physical venues augmented by proprietary wagering technologies position it favorably versus regional competitors amid evolving consumer habits toward digital betting platforms. Regulatory complexity alongside seasonal attendance volatility represent persistent headwinds necessitating continual operational vigilance.

Key upcoming execution points will be vital in assessing management’s ability to balance expansion ambitions with disciplined financial stewardship while maintaining customer engagement at historic events that anchor their ecosystem.

Disclaimer: This analysis is for informational purposes only based on publicly available filings and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments