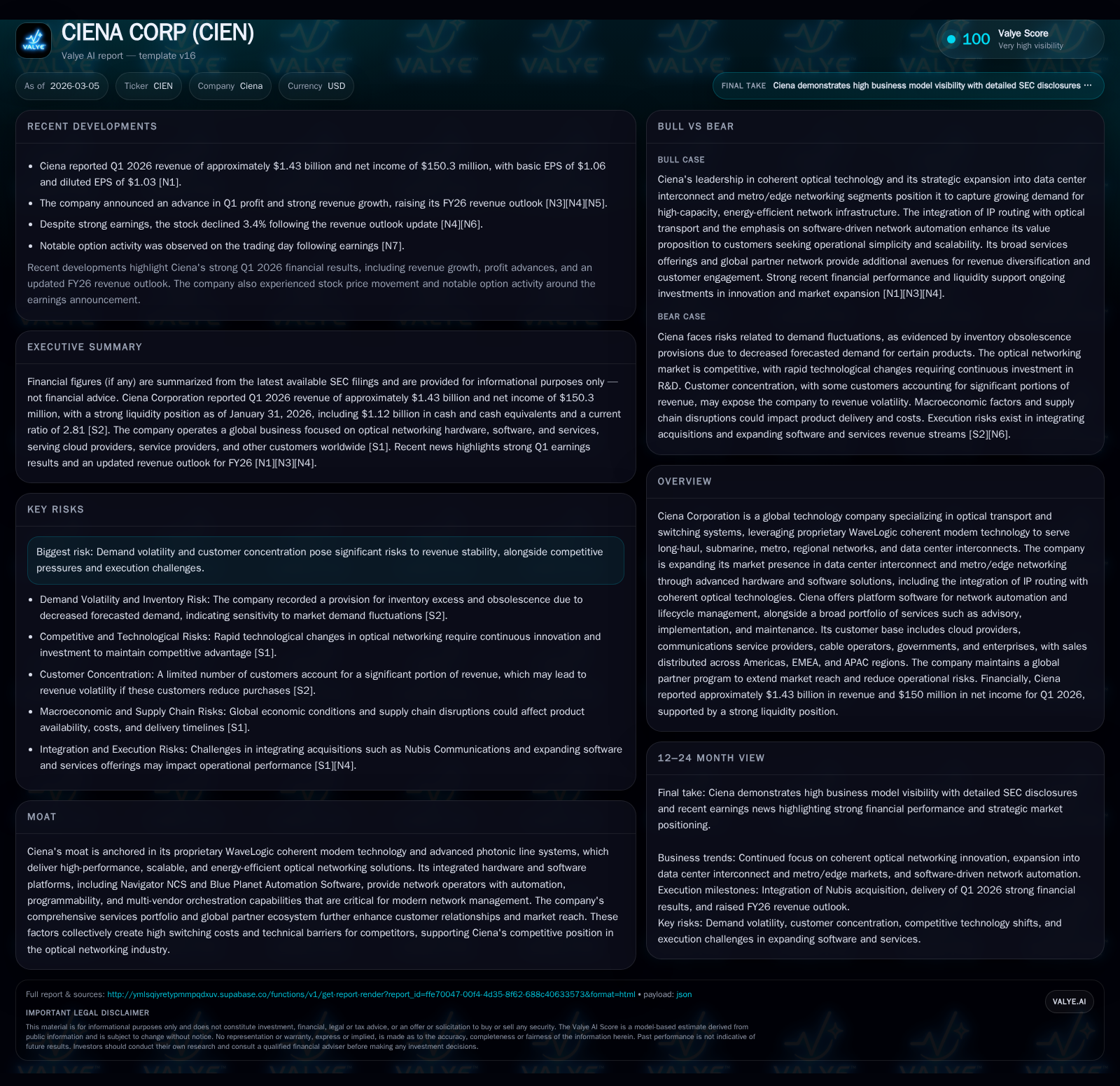

CIENA Corp Advances Optical Networking Growth with WaveLogic Innovation

Ciena demonstrates a strong financial rebound supported by its proprietary WaveLogic coherent optical technology and expanding presence in cloud and edge networking markets.

CIENA Corp achieved significant revenue growth and profit improvement in fiscal 2025, driven by advances in its WaveLogic modem technology and strategic expansion into metro and data center interconnect markets. The company’s solid cash flow generation has underpinned ongoing share repurchases while it navigates risks posed by demand volatility and competitive pressures. Looking ahead, enhanced network automation software and multi-vendor orchestration solutions position CIENA to capture evolving opportunities in optical transport and switching systems.

Financial Performance Recovery: An Analysis of FY2025 Earnings

Ciena Corp demonstrated a noteworthy rebound in fiscal year 2025, building upon prior years' fluctuations with an 18.8% year-over-year (YoY) uplift in revenue to approximately $4.77 billion [F1]. Operating income improved proportionally by 18.6%, reaching nearly $198 million, while net income posted an outsized gain of nearly 47%, reflecting operational gearing and margin enhancements amid steady cost controls [F1]. Operating cash flow (CFO) was particularly robust at over $806 million—a leap of roughly 57%—underscoring enhanced conversion efficiencies possibly linked to better working capital management or higher-margin sales mix [F1]. Capital expenditure (capex) spending remained disciplined at about $141 million, up modestly by around 3%, reflecting selective investment aligned with product development priorities [F1]. Collectively, these metrics point to a pivotal inflection where CIENA sustained growth momentum without compromising cash generation.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 4.8 | 123 | 806 | 198 | +18.8% | +46.9% |

| 2024 | 4.0 | 84 | 515 | 167 | -8.5% | -67.1% |

| 2023 | 4.4 | 255 | 168 | 358 | +20.8% | +66.7% |

| 2022 | 3.6 | 153 | -168 | 223 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 335 | 665 | 4.5 |

| 2024 | 255 | 378 | 3.0 |

| 2023 | 242 | 62 | 8.9 |

| 2022 | 501 | -259 | 5.6 |

Source: SEC companyfacts cache [F1].

The above table summarizes CIENA's annual financial evolution highlighting recovery paths following the dips experienced around FY2023.

Drivers Behind Revenue Growth: WaveLogic Technology and Market Expansion

At the core of CIENA's resurgence lies its proprietary WaveLogic coherent modem technology—an advanced photonic line system architecture that delivers scalable capacity enhancements with energy efficiency improvements critical for modern networks [S1], [N1]. This technology suite supports a variety of deployments spanning long-haul terrestrial fiber, submarine cables, metro aggregation layers, regional networks, and increasingly vital data center interconnect applications where low latency and high bandwidth are paramount [N1], [N4], [S1]. The integration of coherent optics with IP routing capabilities facilitates converged IP-optical architectures fostering densification without proportional power or footprint increase—a valued proposition among cloud providers managing hyperscale infrastructure [S1], [N1]. Furthermore, Ciena's blueprints toward software-driven automation through its Blue Planet Automation platform enable lifecycle management that simplifies orchestration across multi-vendor environments—a growing requirement as network topologies become more heterogeneous [S1]. Together these elements have propelled organic top-line growth by delivering differentiation amid competitive optical networking dynamics.

Customer Concentration Dynamics and Regional Sales Highlights

Revenue concentration remains highest within the Americas region which accounted for approximately $1.12 billion in Q1 fiscal 2026 alone—a substantial increase from $795 million a year earlier—highlighting strong demand from U.S.-based cloud providers and service operators [S6], [S7]. Notably, two large cloud customers contributed collectively over $490 million in revenue during this quarter alone, underscoring their strategic importance but also raising dependency concerns [S6]. The Americas dominance is complemented by steady expansions in EMEA and APAC regions; however, each is markedly smaller in scale relative to the U.S. market [S7]. Such geographic dispersion coupled with a global partner ecosystem broadens market reach but does not eliminate customer concentration risks intrinsic to the sector given the scale of individual buyers.

Strategic Product Integration in Metro and Data Center Interconnects

Ciena has strategically advanced its offering portfolio by intersecting hardware innovations with software-led management solutions tailored for metro edge networks and data center interconnect scenarios [S1]. The expansion into integrated stacks featuring IP routing alongside coherent optics promises greater operational agility when accommodating next-generation workloads such as AI-driven compute clusters demanding fast cross-data-center transfers with minimal latency impact [S1]. Blue Planet Automation Software plays a pivotal role here as it extends beyond simple automation into full network orchestration supporting multi-domain lifecycle management—critical for operators sourcing from multiple vendors yet requiring unified control planes. This positioning entails a technical moat formed by combined hardware-software superiority hard to replicate at scale.

Growth Constraints and Competitive Pressures in Optical Networking

Despite robust top-line advances, risks emanate from inherent demand volatility linked to capital spending cycles among major customers who can steer spending substantially based on economic or competitive factors . Moreover, sizable customer concentration injects revenue predictability challenges should purchasers slow acquisitions or pivot supplier relationships. Meanwhile, competition from peers innovating aggressively on pricing or alternative technologies persists as an industry constant that could cap growth levers if CIENA fails to maintain differentiation or execution focus. While no explicit numeric forecast details are available currently, these qualitative headwinds warrant prudent assessment alongside optimistic signals.

Outlook and Investor Guidance Post Q1 2026 Results

Following a stronger-than-expected first fiscal quarter ending January 31, 2026 with revenue surpassing estimates [N3], Ciena raised its full-year revenue outlook—anchored on accelerating growth trajectory particularly visible within Q2 commentary citing sustained demand momentum [N4]. Despite this positive update, the stock experienced downward pressure attributed primarily to broader market dynamics rather than company fundamentals alone according to analyst conversations captured during that period [N9]. Going forward, monitoring forward bookings trends alongside operating margin sustainability will provide early indicators regarding the quality of growth gains.

Capital Deployment: Robust Cash Flow, Buybacks, and Shareholder Returns

The surge in operating cash flows generating roughly $806 million annually has empowered Ciena to maintain disciplined capex budgets near $141 million while actively executing share repurchase programs totaling approximately $335 million last fiscal year—a notable increase relative to prior years [F1]. Capital allocation emphasizes prioritizing shareholder returns balanced against sustained investment in R&D essential for preserving technological leadership especially around WaveLogic product evolution [F1]. Return on equity remains moderate at approximately 4.5%, reflecting balances between reinvestment needs and payout strategies amidst cyclical earnings patterns [F1].

Service Offerings Enhancing Customer Stickiness and Lifecycle Management

Beyond hardware-software platforms, CIENA’s comprehensive services portfolio—including consulting advisory, implementation support, multi-vendor migration assistance, maintenance contracts, and learning modules—forms an important value-added dimension that fosters stronger client relationships , [S25]. Embedded network lifecycle management tools through Blue Planet Automation Software augment these services by enabling operators to automate provisioning workflows and orchestration tasks yielding faster deployments with lower operational expenditures [S1]. This consultative relationship model raises switching costs for customers thereby reinforcing recurring revenue streams while expanding total addressable markets into transformation engagements.

This analysis synthesizes data extracted directly from Ciena Corporation's SEC filings complemented by recent earnings call transcripts and news reports without speculative extrapolation. Readers should consider external macroeconomic conditions alongside company disclosures when forming views related to CIENA's business trajectory or financial prospects.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments