Capital Maneuvers and Profitability Trends at Columbus McKinnon Corp

An intricate look at how Columbus McKinnon's recent secured debt issuances interplay with its operational gains and liquidity stance.

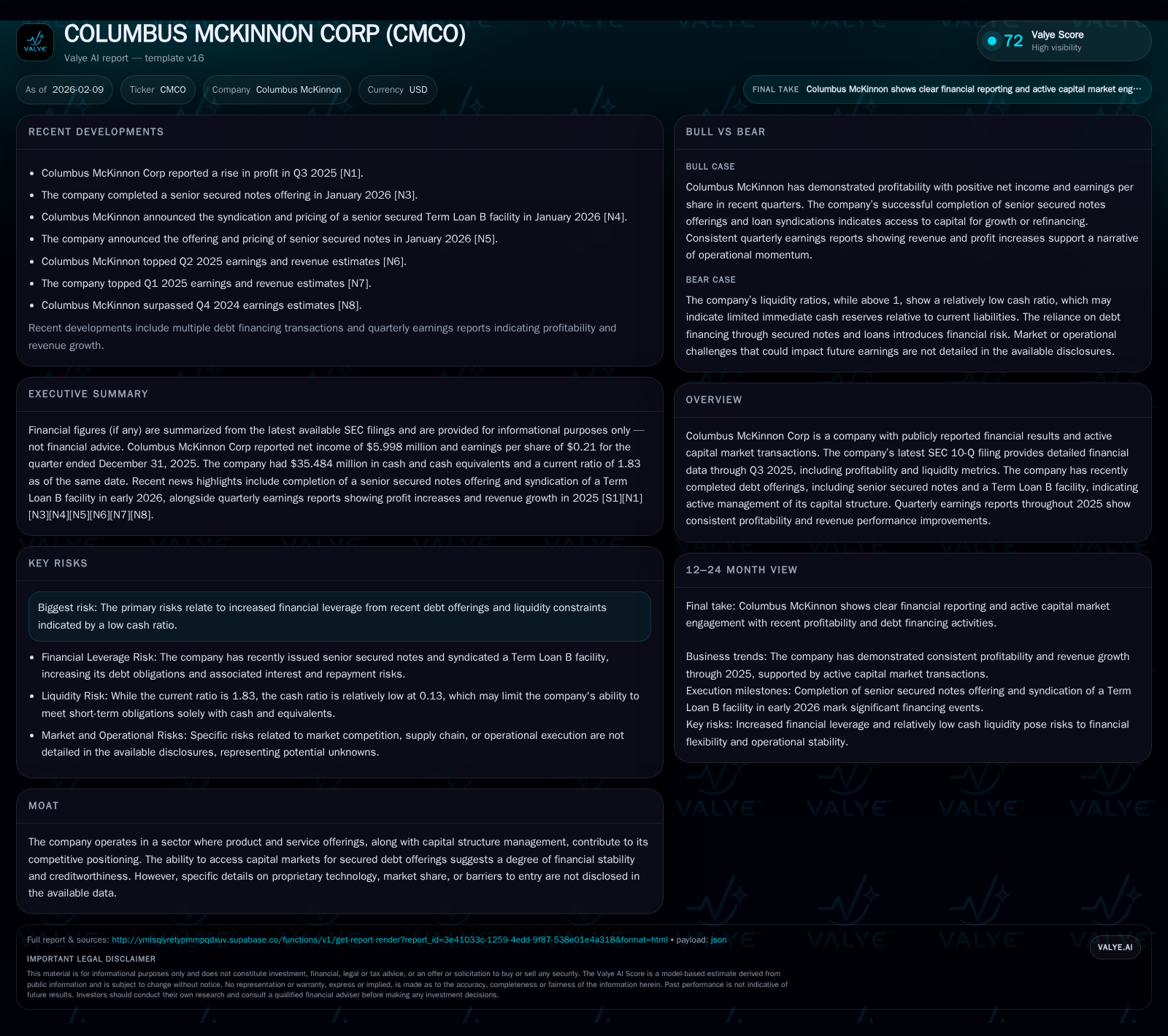

Columbus McKinnon Corp has reported a notable improvement in profitability through Q3 2025 amid strategic capital restructuring via senior secured notes and Term Loan B facilities. While the company’s revenue and net income trends suggest operational momentum, these are juxtaposed against elevated leverage and liquidity pressures that invite a nuanced evaluation of financial resilience. The management commentary underscores a commitment to balancing growth aspirations with disciplined liquidity management in a competitive landscape lacking a pronounced moat.

Profitability Momentum: Diving into Q3 Performance

Columbus McKinnon has demonstrated a steady uptick in its profitability profile through the third quarter of fiscal year 2025. According to reports dated early February 2026, the company recorded meaningful profits that reflect underlying operational improvements [N1]. The financial data consolidates this narrative, with net income reported at approximately $6 million as of the end of December 2025 [F1]. Although detailed quarterly revenue figures are not explicitly itemized for Q3 alone, available disclosures suggest ongoing revenue performance enhancements that buttress profit gains.

This trajectory indicates that despite external headwinds present across industrial segments globally, Columbus McKinnon has managed to refine its cost structures or capture incremental market demand effectively. The Management’s Discussion and Analysis (MD&A) section of the latest 10-Q further elucidates factors contributing to these positive results, including product mix optimizations and targeted operational efficiencies [S2]. Such fundamental progress offers a compelling foundation for understanding the company's capacity to leverage intact demand streams while maneuvering through capital restructuring.

Capital Structure Revisited: New Secured Debt Issuances Explored

Beginning in late January 2026, Columbus McKinnon embarked on a series of secured debt transactions that prominently featured the issuance of senior secured notes alongside a syndicated Term Loan B facility [N3][N4][N5][N6]. These moves mark deliberate actions to reconfigure the company's capital base, enhancing liquidity buffers while potentially optimizing borrowing costs under favorable credit terms.

The senior secured notes offering completed as of January 30 was characterized by robust investor interest and pricing reflective of Columbus McKinnon's credit profile post-transaction [N3]. Complementing this, the Term Loan B syndication finalized around the same period added substantive tranche financing designed to provide both working capital support and longer-term strategic funding flexibility [N4]. The disclosures detail these instruments as having strong collateral pledges, underscoring creditor confidence but simultaneously confirming an elevated total leverage footprint.

From a creditworthiness standpoint, these transactions reveal market acceptance of Columbus McKinnon’s risk-return profile albeit at the cost of increased contractual obligations. Access to secured debt markets affirms operational viability, yet it requires scrupulous stewardship to avoid strain under future economic or sector-specific stress scenarios [S2]. This layered capital structure reflects both proactive financial engineering and an implicit wager on sustained cash flow generation.

Liquidity Under the Lens: Current Ratios and Cash Reserves

Short-term liquidity analysis portrays Columbus McKinnon maintaining a current ratio approximating 1.83 calculated from current assets totaling roughly $482 million against current liabilities near $263 million as of year-end 2025 [F1]. The company's cash and equivalents stand at about $35 million—adequate as a standalone absolute but modest relative to burgeoning debt-related obligations [F1].

This ratio signals generally sufficient working capital coverage but prompts caution given the maturity profiles and covenants embedded within newly issued debt facilities. Management narratives acknowledge this tightrope walk between deploying available cash resources for operational needs versus reserving funds against unforeseen exigencies [S2]. A moderate current ratio coupled with meaningful short-term liabilities demands vigilant cash flow forecasting alongside dynamic liquidity management techniques.

Debt Burden and Leverage Risks: Financial Flexibility Tested

Integral risk factors highlighted within SEC filing Item 1A explicitly describe heightened exposure due to increased financial leverage stemming from recent borrowings [S2]. This magnified indebtedness introduces potential constraints on discretionary spending, investment agility, and buffer capacity amidst volatility.

The tension here hinges on balancing incremental opportunity from enhanced capital availability against the inherent perils of servicing larger debt loads—especially if macroeconomic or industry downturns impede organic earnings growth. While no immediate liquidity crises are disclosed, prudence dictates close monitoring as leverage ratios escalate into more aggressive territories. The senior secured nature of obligations prioritizes creditor recovery rights that could exacerbate challenges if repayment struggles arise.

Ultimately, Columbus McKinnon's approach exemplifies deliberate risk-taking framed within calculated bounds but leaves little room for operational missteps without compromising financial resilience.

Competitive Positioning without a Clear Moat: What Does It Mean?

The valuation snapshot hints at an absence of significant protective economic moats such as proprietary technologies or overwhelming market dominance [valye_report_excerpt]. This nuance suggests that Columbus McKinnon operates within an industry environment where differentiation depends on execution excellence rather than entrenched barriers.

Without explicit technological exclusivity or dominant shareholdings laid out in public filings, competitive advantage may derive instead from product breadth, customer relationships, manufacturing efficiencies, or service responsiveness. However, this landscape raises questions regarding vulnerability to new entrants or price competition over time.

Therefore, strategic attentiveness towards innovation pipelines, customer retention strategies, and supply chain robustness becomes paramount for sustaining relevance amidst industrial peers.

Management Commentary & Strategic Outlook from 10-Q

Management provides candid insights into their forward-looking outlook emphasizing measured growth aligned with capital discipline [S2]. The discussion details steps taken to integrate new financing sources while managing working capital prudently.

Liquidity priorities include safeguarding operational continuity without excessive restriction on strategic investments—a delicate balance explicitly acknowledged by executive commentary. Forecasts incorporate cautious optimism tempered by vigilance concerning economic cycles and sector dynamics impacting demand patterns.

Moreover, management stresses commitment to transparent communication with stakeholders regarding risk mitigation efforts linked to increased indebtedness. This openness enhances interpretative clarity for analysts despite uncertainties inherent in marketplace flux.

Market Response and Investor Sentiment Reflected in Capital Moves

While direct correlations between Columbus McKinnon's equity performance and its recent capital transactions remain opaque given available data sets [valye_report_excerpt], contextual clues suggest investor awareness is shaped partly by broader industrial equity trends rather than isolated corporate events.

For instance, contemporaneous divestments such as Bernzott's sale of Hillenbrand stock allude to shifting investor portfolio reallocations within similar sectors [N2]. Such movements frame a cautious marketplace environment attentive to balance sheet safeguards amid fluctuating growth prospects.

Consequently, Columbus McKinnon's proactive engagement in managing credit facilities likely resonates positively among fixed income custodians while equity investors might adopt a wait-and-see posture influenced by upcoming quarters' performance realities.

Balancing Growth Prospects with Liquidity Constraints

The crux facing Columbus McKinnon lies in reconciling emerging profitability trajectories—reflected in rising net income figures—with tangible pressures emerging from new debt servicing requirements [N1][S2][F1]. Revenue enhancements provide optimism; however, margin sensitivities persist given potential interest expense escalations tied to leveraged positions.

This dichotomy underscores essential trade-offs where investing toward sustaining momentum must be carefully calibrated against rigorous cash management imperatives. Failure to maintain equilibrium risks eroding hard-earned earnings improvements through unexpected liquidity squeezes or covenant breaches.

Operational discipline combined with flexible financial stewardship will therefore define success in harnessing growth potentials without compromising solvency under evolving conditions.

Synthesis: Financial Stability in a Complex Operating Landscape

Ultimately, Columbus McKinnon's evolving financial tapestry reflects an enterprise engaged in deliberate capital structuring amid improving yet still fragile operational performance. The positive earnings signals affirm fundamental business health but must be refracted through a prism acknowledging amplified leverage risks alongside moderate liquidity positions.

Management's evident transparency around strategy and risk contours aids stakeholder comprehension while underscoring themes that transcend simple numeric assessments. In industries lacking overt moats or overwhelming structural advantages, such adaptive financial stewardship may be equally critical as product innovation or market expansion initiatives.

In essence, Columbus McKinnon stands at an inflection point where robust profit delivery intersects tightly with rising debt obligations—the interplay between these forces shaping both near-term stability and long-run strategic latitude.

Disclaimer: This analysis is intended solely for informational purposes based on publicly available data as of early February 2026. It does not constitute investment advice or recommendations regarding securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments