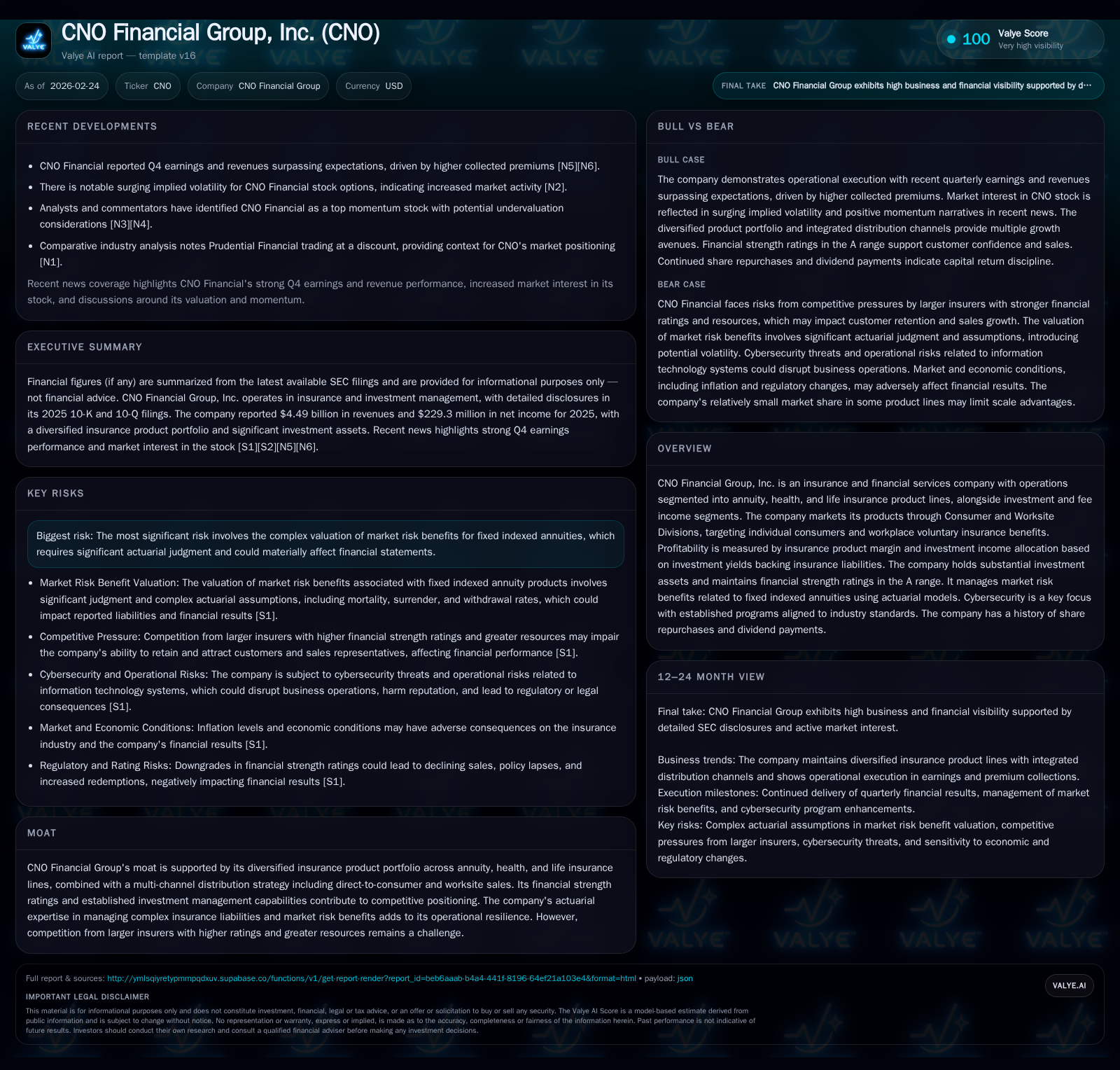

CNO Financial’s Tradeoff Between Stable Margins and Market Risk Complexity

CNO Financial Group balances steady insurance product margins with the complexity of managing fixed indexed annuity market risks in a competitive landscape.

CNO Financial Group has exhibited modest revenue growth and operating income stability over recent years, fueled by diversified insurance product lines and disciplined capital management. The company faces a key challenge in the actuarial complexities of fixed indexed annuities, which require significant judgment and could materially affect financial results. Despite this, CNO maintains strong investment income and consistent shareholder returns via dividends and share repurchases. Future growth hinges on effective management of market risk benefits, technology investments, and regulatory compliance, while litigation risks remain notable.

Company Overview and Business Segments

CNO Financial Group operates primarily as an insurance and financial services provider segmented into annuity, health insurance, life insurance product lines, alongside investment and fee-income segments. The firm's multi-channel distribution model incorporates both consumer direct sales and worksite voluntary benefits marketing. Profitability metrics focus heavily on insurance product margins, which consolidate underwriting earnings with net investment income allocated based on book yields backing liabilities.[S15]

The company manages its exposure to complex market risks embedded in its fixed indexed annuities (FIA), products that offer guaranteed minimum returns plus upside linked to market indices such as the S&P 500. These products incorporate embedded derivatives whose fair value depends on long-term assumptions about index returns, participation rates, policyholder behavior, and interest rates.[S26] Managing these actuarial inputs demands rigorous expertise and represents a material judgment area affecting earnings volatility.

CNO maintains financial strength ratings in the A range from major rating agencies—a competitive advantage facilitating agent retention and consumer trust. However, the firm faces competition from larger insurers with higher credit profiles and broader resources.[N6][S19]

Historical Performance Summary

Over the past four fiscal years ending December 31, 2025, CNO's revenue trajectory has been moderately positive with some fluctuations: after rising from $973.6 million in FY2022 to peak at $1.17 billion in FY2023, revenues softened slightly before rebounding to $1.14 billion in FY2025 (+4.2% YoY vs FY2024). Operating income doubled between FY2022 ($357 million) and FY2025 ($553 million), reflecting underwriting improvements and disciplined cost management; however net income was volatile—peaking at $166 million in FY2024 before dropping sharply to $93 million in FY2025 largely due to higher actuarial reserves adjustments and impairments.[F1][S27]

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1143 | 93 | 676 | 553 | +4.2% | -44.1% |

| 2024 | 1097 | 166 | 628 | 551 | -6.3% | +357.6% |

| 2023 | 1171 | 36 | 583 | 460 | +20.2% | -16.4% |

| 2022 | 974 | 43 | 495 | 357 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 66 | 331 | 3.5 |

| 2024 | 68 | 300 | 6.6 |

| 2023 | 68 | 166 | 1.6 |

| 2022 | 65 | 190 | 3.1 |

Source: SEC companyfacts cache [F1].

Note: Capital expenditure data is not available from provided filings.

Cash flow from operations demonstrated consistent growth supporting dividends and aggressive share repurchases—with buybacks increasing from $190 million in FY2022 to over $330 million in FY2025.[F1][S12]

Key Financial Drivers & Future Growth Prospects

The primary engine behind future growth remains the annuity segment bolstered by fixed indexed annuities that continue to attract customers seeking downside protection paired with participation in equity markets.[N1] Growing premiums collected in health and life insurance product lines complement this base.[N2]

Investment income allocation is critical since interest yields underpin product margins—the company reported rising net investment income linked largely to fixed maturity assets averaging near or above historic yields of approximately ~4%, aided by mortgage loan yield expansion (up to $161 million net income contribution versus prior years).[S16]

Capital allocation toward share repurchases balances shareholder returns with maintaining regulatory surplus requirements; a recent board-authorized repurchase of up to $500 million signals continuing shareholder confidence.[S12]

However, actuarial risk assumptions pertaining to FIA embedded derivatives represent significant uncertainty; policyholder behavior changes or index volatility can cause material swings in valuation reserves affecting quarterly earnings.[S26] Additionally, legacy business impairments linked to exited fee-service lines introduce non-recurring charges impacting comparability.[S27]

Technology initiatives like the TechMod platform aim to replace legacy systems but entail budgetary risk; delays or overruns could impair operational efficiency or elevate compliance costs.[S18]

Regulatory scrutiny remains elevated across sales practices, complaint handling, policyholder dispute resolution, especially around life products originated before enhanced consumer protections tightened rules.[S4][S20] Vigilant management of these factors is essential for sustained growth.

Capital Structure & Returns Profile

CNO's debt comprises senior unsecured notes including a $700 million tranche maturing in June 2034 bearing a coupon of approximately 6.45%, along with $500 million due May 2029 at approximately 5.25%, complemented by subordinated debentures of $150 million at a coupon of approximately 5.125% due in 2060.[S22][S25] Variable rate borrowings through FHLB collateralized lines approximate $2.44 billion supporting asset purchases tied predominantly to fixed maturity securities valued at roughly $3.48 billion.[S17]

At year-end FY2025 stockholders' equity reached $2.64 billion resulting in an approximate return on equity (ROE) of about 3.5%, given depressed net income for the year—and despite healthy operating cash flows exceeding net earnings by over sevenfold—likely influenced by reserve builds and non-cash impairments.[F1]

Dividend payouts remain modest relative to free cash flow (~$66 million declared), sustained through gradual quarterly increases since early-2023 indicating confidence in steady cash generation.[F1][S12] Share repurchase programs have grown appreciably with nearly $332 million spent in FY2025 signaling management’s preference for returning capital amid limited reinvestment alternatives.

Regulatory & Legal Risks

The firm contends with protracted litigation including class-action suits alleging breaches on historical life insurance premium provisions under alter ego theories; trials extending into late-2025 resulted in partial verdicts favoring plaintiffs but contingent on further judicial rulings that may take years including appeals.[S6][S7]

Additionally, regulatory examinations focus on sales conduct, underwriting practices, claims handling processes exposing potential liabilities including penalties or mandated remediation efforts that could affect profitability or reputation.[S20]

Guaranty fund assessments have been stable but represent ongoing expense pressure related to state-level insurance insolvency protections.[S20]

Cybersecurity & Operational Considerations

CNO prioritizes cybersecurity aligned with frameworks such as NIST’s Cybersecurity Framework aiming to mitigate risks associated with data breaches that previously compromised personal information but never materially impacted business continuity.[S18]

Legacy infrastructure maintenance entails rising costs; success of TechMod initiative is pivotal for reducing long-term technology risks though execution uncertainties loom.[S18]

Outsourcing third-party vendor dependencies heighten operational volatility especially amid evolving regulatory standards governing service provider oversight.[S19]

Industry Context (Analysis)

The U.S. individual annuity market is characterized by heightened competition from large-cap insurers commanding higher credit ratings enhancing agent channel access; CNO competes via niche worksite voluntary benefits combined with core retirement-focused annuities offering guarantees well suited for conservative customers seeking downside protection amid persistent market volatility.

Interest rate environments shape yield curves impacting new business economics as well as reinvestment rates backing existing blocks—strategic asset liability matching remains vital as duration mismatches can exacerbate earnings sensitivity.

Increasingly insurer balance sheets are challenged by more complex embedded derivative accounting under GAAP attributed especially to FIA designs combining guarantees with option-like features necessitating sophisticated modeling tools.

Conclusion & Monitoring Points (Analysis)

CNO Financial Group exhibits controlled top-line growth balanced by rigorous actuarial management of complex FIA portfolios which constitute both an operating leverage opportunity and a source of earnings variability.

Key areas warrant close surveillance include:

- Evolution of actuarial assumptions impacting FIA embedded derivatives valuations,

- Progress on TechMod system modernization projects,

- Developments in ongoing litigation outcomes,

- Regulatory investigations outcomes,

- Trends in premium collections reflective of consumer purchasing power,

- Investment portfolio yield environment,

- Share repurchase cadence versus liquidity needs.

This comprehensive approach positions CNO for continued operational resilience while managing inherent tradeoffs associated with its product portfolio complexity.

This report is intended solely for informational purposes based on publicly available information as of early-2026; it does not constitute investment advice or recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments