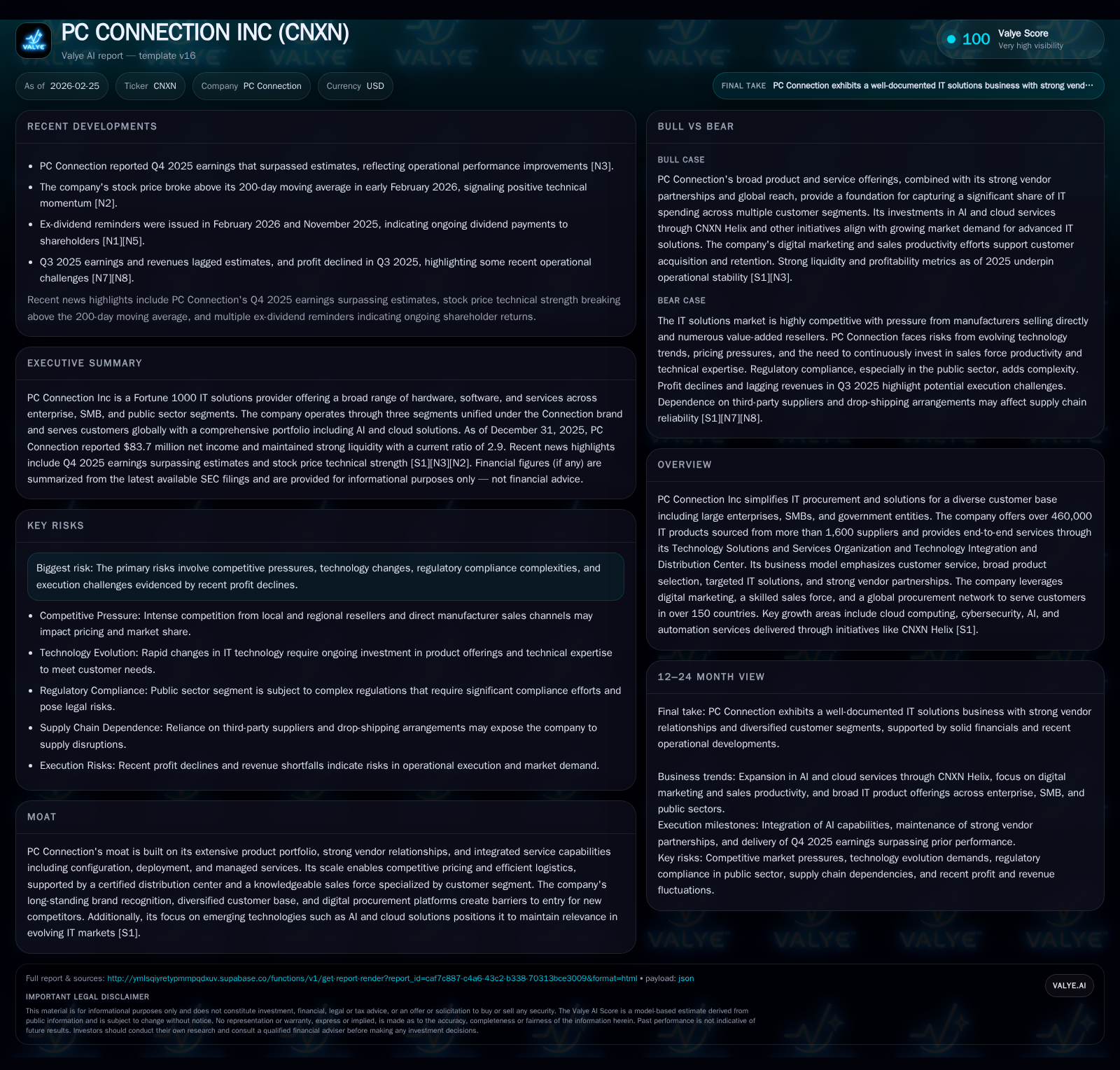

PC Connection’s Strategic Pivot: Balancing Scale and Innovation for Sustainable Growth

PC Connection Inc. leverages its broad IT product portfolio and integrated services to sustain competitive advantages amid evolving technology demand and margin pressures.

PC Connection Inc. operates a vast IT procurement ecosystem, providing over 460,000 products and comprehensive technology solutions across enterprise, SMB, and public sector markets. While recent years show steady revenue with moderate operating income growth but slight net income contraction, challenges in margin compression and working capital management have emerged. The company's strategic emphasis on cloud, AI, and cybersecurity initiatives like CNXN Helix aims to fuel future growth. Capital allocation remains disciplined, balancing dividends and opportunistic share repurchases amid volatile operating cash flows. PC Connection’s moat is underpinned by strong vendor partnerships, a certified distribution center, an experienced sales force, and integrated managed services that help counter increasing competition and regulatory complexities.

Evolution of PC Connection’s Growth Trajectory and Underlying Drivers

PC Connection Inc., a Fortune 1000 global IT solutions provider, demonstrated relatively stable top-line performance across recent fiscal years ending December 31 from 2023 through 2025. Although explicit total revenue figures across all years are not fully disclosed within available companyfacts [F1], the company reported operating income of $103.2 million in FY2023 which slightly decreased to $97.1 million in FY2024 before ticking up again to $99.3 million in FY2025—registering a modest +2.3% increase from FY2024 to FY2025 [F1]. Net income deviated slightly more; it rose from $83.3 million in FY2023 to $87.1 million in FY2024 before retreating by -3.9% to $83.7 million in FY2025 [F1]. This divergence indicates growing cost or non-operating pressures that partially offset operational gains.

Year-over-year fluctuations reflect underlying market complexity including margin compression caused by heightened competitive pricing dynamics as well as investments into emerging technology capabilities [N1][S20]. The deceleration of net profits despite modest operating income improvement underscores the balance PC Connection seeks between expanding service offerings and managing execution risks.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 84 | 65 | 99 | -3.9% |

| 2024 | 87 | 174 | 97 | +4.6% |

| 2023 | 83 | 198 | 103 | -6.7% |

| 2022 | 89 | 35 | 121 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Capex, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 15 | 76 | 9.2 |

| 2024 | 11 | 12 | 9.6 |

| 2023 | 8 | 5 | 9.9 |

| 2022 | 9 | 10 | 11.6 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures unavailable for inclusive table; Capex data for earlier years omitted due to data insufficiency.

Commercial Segments and Client Mix Impacting Revenue Composition

The company segments its IT procurement into three distinct markets: Enterprise Solutions serving large corporations; Business Solutions targeting small- to medium-sized businesses (SMBs); and Public Sector Solutions focused on government and education institutions [S1][S5][S10]. In the fiscal year ended December 31, 2025, medium-to-large businesses contributed approximately 44.6% of total net sales while SMBs accounted for roughly 37.7%, with government/education comprising the remaining 17.7% [S5][S10]. This client segmentation illustrates a diversified customer profile that mitigates concentration risk since no individual customer exceeded a single-digit percentage of total revenues.

Within each segment, PC Connection applies specialized sales teams supported by a dedicated technical solutions group to address unique operational needs [S13]. The Enterprise segment emphasizes custom web-based procurement portals such as MarkITplace™ enabling large corporate customers streamlined sourcing options combined with negotiated pricing leverage [S8]. Business Solutions employ a blend of inside sales complemented by online platforms facilitating rapid order placement for SMB clients [S10]. Public Sector Solutions navigate complex federal regulations through targeted expertise critical for government contracts compliance [S23]. This tailored approach supports differentiated go-to-market strategies enhancing cross-segment resilience.

Technological Focus: Cloud, AI, and Cybersecurity as Growth Catalysts

PC Connection's strategic agenda pivots towards leveraging emerging technologies within their expansive catalog exceeding 460,000 products sourced from over 1,600 suppliers [S1][S4]. Their Technology Solutions and Services Organization (TSSO) orchestrates end-to-end services spanning design-to-deployment lifecycle assistance including configuration services provided at their certified Technology Integration & Distribution Center (TIDC) [S4][S18].

Particularly noteworthy is the CNXN Helix platform initiative—an integrative effort launched in 2023 aimed at advancing AI-driven automation solutions alongside cloud computing adoption [S18][N1]. PC Connection offers workshops on AI infrastructure design while scaling consulting capacity through alliances within its vendor ecosystem targeting multi-industry horizontal applicability [S18]. Cloud expertise is reinforced by Microsoft Azure Expert Managed Service Provider status—a designation that signals rigorous third-party validation of service competencies critical for enterprise-grade environments [S17]. This technology-focused progression is coupled with digital marketing amplification encompassing remarketing campaigns, Google Shopping integrations, social media outreach, video promotions, webinars, all finely tuned by advanced analytics to drive solution adoption among healthcare, retail, finance, manufacturing verticals [S6][S18].

Such integrated managed services enable shift beyond hardware/software reselling towards higher-margin IT service offerings responding to client demand for complex infrastructure transformations emphasizing cybersecurity safeguards amid growing threat landscapes.

Operating Margin Trends, Profitability Challenges, and Margin Drivers

Margins have shown sensitivity given intensifying price competition stemming from both direct manufacturer sales channels (e.g., Apple, Dell) and larger national distributors like CDW or SHI Enterprises becoming increasingly aggressive [S20][N2][S22]. Despite this backdrop, PC Connection's scale affords some pricing leverage along with volume-driven cost efficiencies realized through supply chain operations supporting just-in-time logistics along with pre-configuration capabilities at TIDC.

Yet margin drivers remain challenged by product mix evolution favoring cloud subscriptions or software licenses that typically carry lower gross margins compared to hardware sales [F1][N2]. Supply chain volatility also influenced profitability as a late-year DRAM/NAND memory shortage generated capacity constraints potentially inflating procurement costs [S27]. These aspects underscore why operating income saw only incremental growth (+2.3%) year-over-year even while investing heavily in innovation platforms delivering longer-term growth potential.

Working Capital Management and Cash Flow Volatility Dynamics

Working capital management has proved a headwind recently evidenced by an elongation of PC Connection's cash conversion cycle to approximately 45 days at the end of December 31, 2025—up from around 40 days the year prior—with increases concentrated notably in days sales outstanding (DSO) rising from roughly 72 to 76 days alongside days inventory outstanding (DIO) expanding significantly from approximately 15 to 23 days [S26][F1]. Days payables outstanding also grew moderately offsetting some effects but not sufficiently enough to neutralize net cash impact.

These shifts contributed materially to the year-over-year drop of roughly $108 million (-62%) in net cash provided by operating activities down to $65 million in FY2025 from near $174 million previously despite stable net income trends [F1][S1]. Inventory accumulation stemmed largely from customer rollout requirements necessitating earlier purchases plus tighter supply conditions [S1][N2]. Similarly higher DSO reflects changed timing around customer deliveries impacting liquidity profile requiring vigilant monitoring moving forward.

Capital Allocation Strategy: Dividend Policy, Stock Buybacks, and Investment

PC Connection pursues a balanced capital deployment approach emphasizing shareholder returns amid prudent investment in operational capabilities [F1][N3]. In FY2025 dividend payments increased meaningfully to about $15.3 million representing steady annual growth relative to prior years ($10.5 million in FY2024), reflecting growing comfort in cash flow stability despite working capital cycles [F1][N3]. Share repurchases accelerated substantially totaling $76 million during the same period compared with roughly $12 million previously indicating opportunistic buyback execution leveraging excess liquidity on hand now augmented by credit facility expiration without replacement debt obligations supporting conservative leverage stance [F1][S15].

Capital expenditures remained moderate at approximately $7.4 million focused primarily on IT infrastructure enhancements underpinning e-commerce platforms plus internal software development supporting TIDC scalability consistent with evolving strategic emphasis on digital transformation [F1][S26]. Resulting return on equity derived from reported metrics approximates about 9.2%, validating measured profitability adjusted for reinvestments amidst margin variability challenges [F1].[

Competitive Moat: Vendor Relationships, Logistics, and End-to-End Services

PC Connection fortifies its market position via entrenched partnerships with over 1,600 technology vendors including industry leaders such as Microsoft Corporation (16%), HP Inc., Dell Inc., Ingram Micro Corp., TD Synnex among top suppliers accounting collectively for a sizeable portion of product purchases annually [S24][S27]. These strategic relationships permit preferential access to new technologies first-to-market product variants combined with cooperative marketing arrangements aiding gross margin enhancement potential.

Their certified Technology Integration & Distribution Center located in Wilmington Ohio operates under ISO 9001:2015 SOC2 Type2 standards bolstering reliability while executing more than half a million configurations annually ranging across personal computing devices through networking hardware emphasizing streamlined logistics meeting expedited delivery demands as fast as overnight shipments available for urgent customer needs evidencing logistic sophistication rivaling larger competitors yet preserving nimbleness characteristic requisite for global solutions providers servicing clients across over150 countries via GlobalServe offerings [S4][S28].

The company's value-added reseller model pairs expert technical solution architects embedded within the TSSO fostering industry-specific insights communicated directly through segmented account managers ensures superior comprehension of client operational challenges facilitating tailored IT environment deployments elevating switching costs vs pure-play commodity resellers thus solidifying barrier against emergent entrants despite highly fragmented marketplace conditions [S19][S6].

Risks from Market Competition, Regulatory Compliance, and Execution

Competitive intensity ramps up continuously as both established distributors like CDW Corporation & SHI Enterprises expand solution portfolios alongside large manufacturers increasingly selling direct thus shrinking intermediated market share opportunities [S22][N2]. Technological disruption pace renders legacy hardware-centric models less profitable forcing ongoing adaptation toward cloud subscription models prone to narrower margins potentially constraining future profitability if scale economies do not compensate adequately accompanied by execution complexity related to upskilling sales forces into consultative technology advisors at par with regional VARs or systems integrators such as Accenture or IBM complicating growth trajectories further.

Regulatory complexity escalates notably within the Public Sector Solutions domain where multiple federal laws including FAR compliance mandates plus data privacy statutes such as CCPA/CALPA create substantial overhead burdens necessitating rigorous internal controls lest risk costly litigation or contract loss scenarios arise adversely impacting financial results or reputation integrity particularly when technology procurements often involve sensitive cybersecurity environments subject to breaches or compliance audits highlighting the imperative for sustained investment into governance frameworks [S20][S23][N2].[ Legal proceedings have not materially impacted recent financial outcomes but require ongoing vigilance considering sector-wide exposure levels.[S21]

Key Performance Metrics to Track: Future Milestones and Market Sentiment

With limited formal forward guidance explicitly issued per public disclosures post Q4 FY2025 earnings release [N1] investors should closely monitor forthcoming quarterly filings for signs of stabilization or improvement in gross margins reflecting successful CNXN Helix uptake alongside operating cash flow recovery essential given recent volatility documented in working capital components.[N4] Trading behavior following earnings surprises will also offer directional market sentiment clues regarding confidence in management's strategic transformation initiatives centered on cloud integration plus AI service expansion.[S2] Core metrics such as days sales outstanding trends versus inventory turns will be early indicators of improved liquidity management effectiveness while margin expansions will signal tactical pricing power preservation amidst competitive headwinds shaping near-term earnings quality.[ Sales productivity improvements measured through average revenue per account manager tied against SG&A expense controls remain vital levers underpinning bottom-line enhancement prospects consequently requiring detail orientation during conference call disclosures assessing progress on personnel training impacts driving consultative selling approaches forming foundation for enhanced solution-service uplift opportunities.[N2]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments