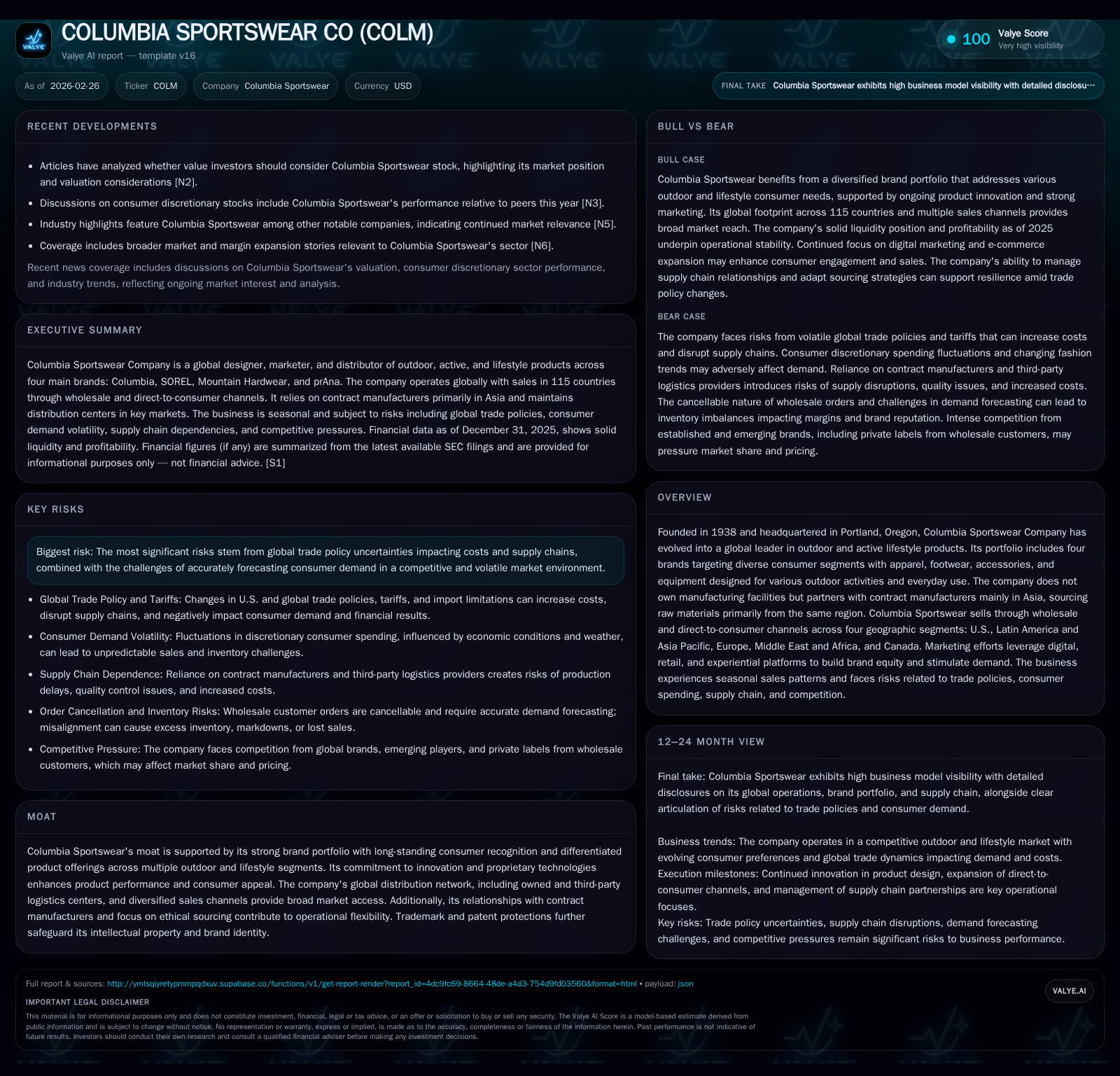

Columbia Sportswear’s Turnaround Path: Balancing Innovation and Tariff Headwinds

Columbia Sportswear confronts a sharp revenue decline shaped by tariff-induced cost pressures while leveraging product innovation and brand strength for recovery.

Columbia Sportswear Company experienced a drastic 69.9% drop in revenue in 2025, driven by trade policy uncertainties and disrupted demand forecasts. Despite this top-line contraction, net income rose due to effective cost controls and margin management. The company’s multi-brand portfolio—featuring Columbia, SOREL, Mountain Hardwear, and prAna—continues to innovate within the outdoor lifestyle segment, bolstering consumer loyalty. Going forward, tariff litigation outcomes, supply chain adaptations, and execution of strategic priorities will be pivotal as Columbia seeks to restore growth and operational resilience.

Financial Trajectory: Navigating the Recent Profitability Decline

Columbia Sportswear Company’s financial narrative in 2025 is marked by a dramatic divergence between top-line contraction and bottom-line resilience. Revenue plunged by approximately 69.9% compared to the prior year [F1], reflecting severe disruptions in consumer demand and wholesale order cancellations influenced heavily by global trade volatility [S1][S2]. Operating income declined by a smaller magnitude (23.5%), reaching $207 million [F1], while net income surprisingly rebounded by 85.1% to $177 million [F1], suggesting aggressive cost management or potentially non-recurring factors supporting profitability.

Operating cash flow also faced headwinds falling by over 42%, settling at $283 million [F1], yet remained sufficient to generate a free cash flow surplus around $254 million after capital expenditure reductions of nearly 77% [F1]. This capex cutback aligns with the company's attempt to preserve liquidity amid uncertain demand.

The above indicates Columbia adopted a defensive posture in operations to weather an unusual revenue shock but retained disciplined capital stewardship despite margin compression. The steep revenue drop contrasts with a relatively moderate decline in operating profit margins, hinting at operational leverage effects being tempered through dynamic expense control [S1]. This financial turbulence sets the context for understanding Columbia’s multifaceted challenges.

Historical performance (annual)

| FY | CFO ($mm) | OpInc ($mm) |

|---|---|---|

| 2025 | 283 | 207 |

| 2024 | 491 | 271 |

| 2023 | 636 | 310 |

| 2022 | -25 | 393 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) |

|---|---|---|

| 2025 | 66 | 201 |

| 2024 | 70 | 318 |

| 2023 | 73 | 184 |

| 2022 | 75 | 287 |

Source: SEC companyfacts cache [F1].

Trade Policy Impact: Tariff Pressures Reshaping Supply Chains and Margins

Integral to Columbia’s recent financial stress has been the rapidly evolving U.S. trade environment, which injected significant cost inflation and supply chain uncertainty. Imported goods face duties and tariffs that have fluctuated unpredictably due to U.S. policy shifts targeting imports mainly from Asia [S1][S25]. The company has been litigating the legality of incremental tariffs paid—approximately $50 million for just 2025—and awaits resolution that could materially impact fiscal results [S1][S3].

Tariffs increased product prices downstream, dampening discretionary consumer spending particularly in apparel and footwear categories sensitive to inflationary hikes [S1][S2]. Wholesale customers felt financial strain causing canceled orders or deferred payments impairing Columbia's sales predictability [S2][S17]. Moreover, Columbia canceled certain product orders ahead of fall and spring seasons due to misaligned demand forecasts exacerbated by trade disruptions [S1][S8].

From a sector perspective, such import duty volatility directly raises landed cost of goods sold (COGS), pressuring gross margins unless offset by price increases—which risk further suppressing volume—or aggressive promotions eroding profitability. These dynamics forced Columbia into heightened promotional activity in the U.S., eroding pricing power amidst competitive pressures [S1].

Multi-Brand Portfolio: Innovation and Market Positioning Across Segments

Columbia Sportswear’s resilience draws upon its diversified brand portfolio that strategically spans from technical outdoor performance to fashion-forward lifestyle goods [S1]. The flagship Columbia® brand anchors high-value outdoor products tailored for varied activities including hiking, snow sports, fishing, and everyday wear.

The SOREL® brand has pivoted towards contemporary urban-lifestyle footwear while retaining rugged heritage appeal. Mountain Hardwear® serves a niche of premium technical apparel for extreme climates favored by climbers and trail athletes. prAna® provides versatile mindful apparel blending style with functionality for active lifestyles.

Innovation is central; proprietary textiles and patented technology sustain differentiation in a saturated outdoor retail space where consumers increasingly seek both performance credentials and versatility [S1][S7]. Maintaining this innovation pipeline is critical for combatting market saturation risks especially when gross sales are challenged.

Regional Sales Footprints: Wholesale vs. Direct-to-Consumer Balance

Geographically segmented into four regions—U.S., Latin America & Asia Pacific (LAAP), Europe/Middle East/Africa (EMEA), and Canada—Columbia boasts broad global reach with distinct channel strategies [S4][S5][S6].

Wholesale distribution encompasses specialty stores, national chains, department stores, internet retailers, plus international distributors especially in EMEA/LAAP where direct operations are limited. DTC channels encompass over 170 U.S., more than 70 European retail stores plus extensive e-commerce platforms supporting each brand’s digital footprint [S4][S5]. This omnichannel approach aims to capture shifting consumer preferences toward online shopping.

Supply chains rely heavily on contract manufacturing partners primarily situated across Vietnam, Bangladesh, Indonesia, India among others with five major manufacturers accounting for about 30% of production volume [S24]. Distribution centers owned across key markets (Portland OR; Robards KY; Ontario Canada; France) support inventory flow but fixed costs add leverage risk during downturns [S6][S18]. Third-party logistics reliance introduces vulnerability given capacity constraints exacerbated by labor unrest or geopolitical conflicts impacting freight costs [S16][S19].

Capital Allocation Review: Dividends, Buybacks, and Return on Equity

Despite operational headwinds, Columbia maintained capital returns with dividends totaling roughly $65 million in 2025—a modest decrease from prior years—and share repurchases worth about $201 million down from $318 million previous year [F1]. The sustainability of buybacks may warrant scrutiny amid shrinking free cash flow margins although current levels suggest cautious continuation.

Return on equity (ROE) calculated at around 10.4% reflects middling returns relative to industry peers but remains supported by disciplined profitability improvements despite revenue contraction [F1]. Lower capex investment underscores prudent capital preservation efforts during uncertainty while preserving balance sheet flexibility with cash equivalents exceeding $440 million affords ballast against near-term volatility [F1].

Future Outlook: Demand Forecasting Challenges and Growth Constraints

Looking ahead, Columbia faces an array of challenges impinging on growth prospects including ongoing trade policy uncertainties that cloud cost assumptions for raw materials sourced notably from China (21%-27%) for spring/fall inventories [S16]. Failure to resolve tariff litigations timely prolongs earnings variability risk.

Compounding these external risks is the inherent difficulty of forecasting consumer demand amidst macroeconomic recessions or inflation-driven discretionary spending contractions impacting both wholesale customers’ financial health and direct orders leading to inventory misalignments [S8][S22][N8][N13]. Tactical cancellation of orders signals caution but could impair full market participation if consumer appetite recovers suddenly.

Growth hinges on successful execution of strategic priorities targeting brand awareness uplift through focused demand creation investments plus enhancement of digital capabilities that improve consumer experience across all touchpoints globally [S20][S21]. Inventory discipline combined with agile sourcing adjustments also crucial amid raw material pricing pressures.

What Investors Should Monitor Next

Monitoring quarterly earnings reports will help gauge whether recent cost controls translate into sustainable profitability amidst still fragile topline conditions. Key focal points include updates on tariff litigation outcomes affecting potential refunds or ongoing duties impacting gross margins.

Wholesale customer credit quality remains vital given exposure concentration risks particularly if broader retail dislocations intensify recessionary impacts. Tracking new product launches from all four brands can indicate innovation pipeline health crucial for market differentiation.

Supply chain adaptations manifested via shifts toward alternative manufacturing countries or logistics providers will reveal how successfully Columbia manages its operational flexibility versus rising input costs. Investor scrutiny should also extend to inventory turnover rates indicating balance between supply/demand alignment.

In sum, Columbia Sportswear Company's path forward requires balancing tactical maneuvers addressing headwinds from tariffs while reinforcing core strengths rooted in brand innovation and distribution network optimization amid evolving consumer patterns.

This analysis synthesizes publicly available filings and documented disclosures without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments