Compass, Inc. Consolidates Market Reach with Key Acquisition and Expanding Agent Network

Following its acquisition of Anywhere Real Estate, Compass broadens scale and brand portfolio while expanding its technology-enabled agent platform.

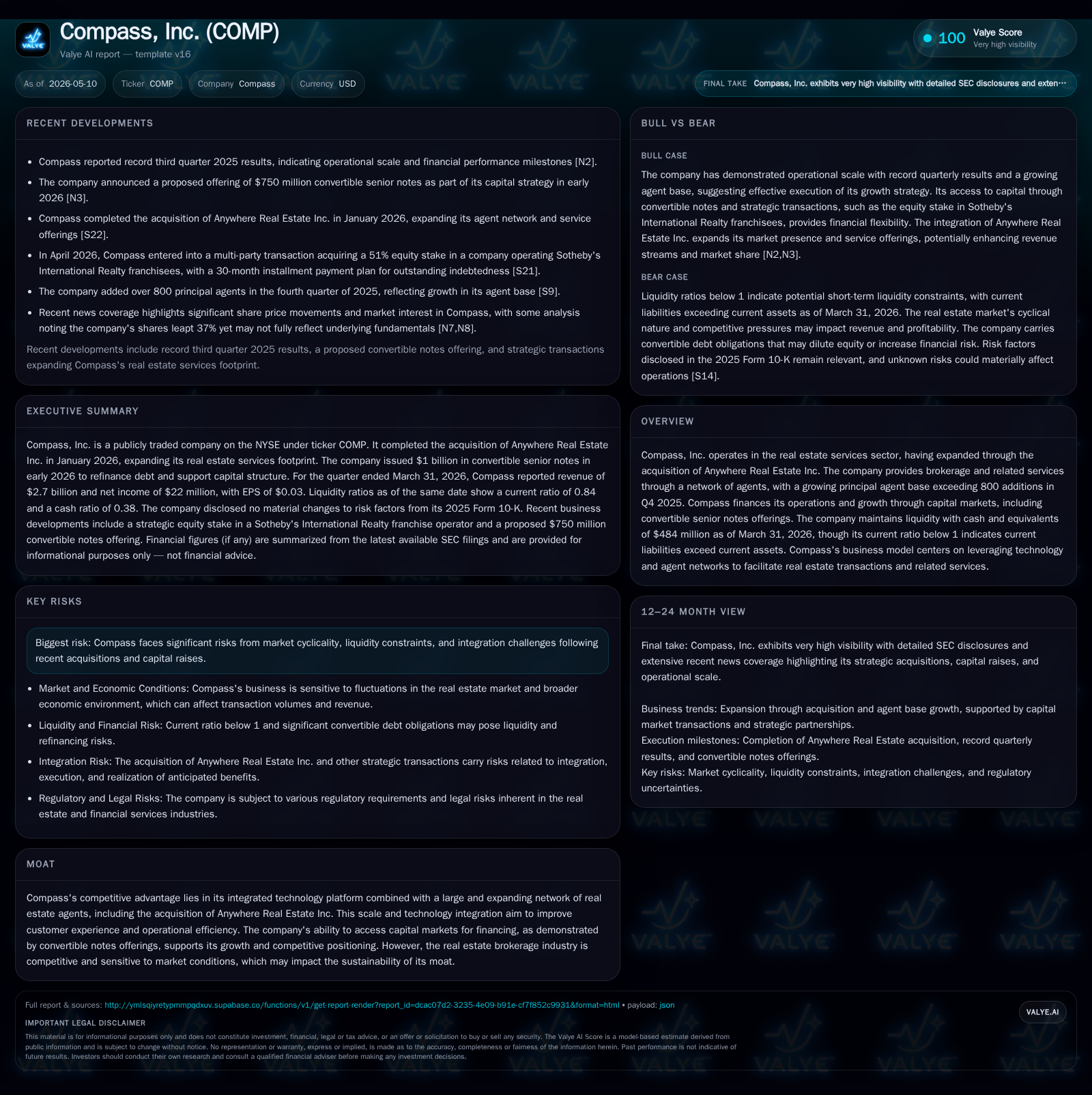

Compass, Inc. completed its acquisition of Anywhere Real Estate in January 2026, integrating a substantial franchise and brokerage footprint into its platform. In Q4 2025, the company added over 800 principal agents, signaling strong network growth that supports transaction volume expansion. Compass's business model leverages an integrated technology platform combined with a diversified brand portfolio to capture commission revenue alongside ancillary real estate services. However, cyclical real estate market risks and tight liquidity (current ratio below 1) amid a $3.15 billion debt load present ongoing challenges. Near-term execution on integration and agent retention will be critical for validating synergy expectations and sustaining growth momentum.

Latest Operating Developments: Acquisition Completion and Agent Base Expansion

Compass marked a pivotal corporate milestone with the completion of its acquisition of Anywhere Real Estate Inc. on January 9, 2026 [S1][S16]. The merger significantly broadens Compass's footprint beyond its established owned-brokerage operations under the Compass brand to incorporate franchises operating under names like Coldwell Banker and Sotheby’s International Realty. This expanded reach now spans every major U.S. city plus approximately 120 countries worldwide [S1].

Complementing scale gains from the acquisition, Compass achieved notable organic expansion in late 2025 by adding over 800 principal agents in Q4 alone to its owned-brokerage roster [S4]. As of December 31, 2025, this translates to over 37,000 agents across 39 states plus Washington D.C., illustrating robust recruitment effectiveness that directly feeds transaction volume potential [S1][S4].

These developments reposition Compass as a more diversified player combining broad geographic exposure with enhanced brand depth and an enlarged agent network. Such scale provides avenues for operational synergies and cross-brand referrals but also raises integration execution demands.

Compass’s Business Model: Integrated Brokerage and Technology-Driven Services

Compass generates primary revenue through commission sharing arrangements with independent contractor real estate professionals who affiliate their licenses with the company [S1]. These agents utilize Compass’s proprietary technology platform designed to improve lead generation, client management, listing marketing, pricing analytics, and operational workflows. Revenue mechanics rely largely on capturing a portion of gross sales commissions earned when homes close transactions facilitated by these agents.

Beyond brokerage commissions, Compass expands monetization opportunities via complementary integrated services—title and escrow services provided directly or through joint ventures (including title underwriting acquired from Anywhere), mortgage origination via a minority-owned joint venture with Guaranteed Rate, Inc., relocation services added through the merger—and franchise royalties [S1]. This diversified service mix acts as a multiplier effect enhancing overall customer lifetime value while deepening ecosystem lock-in dynamics.

The agent model hinges on maintaining productivity through advanced technological enablement coupled with a flexible contractor relationship that appeals to a wide range of real estate professionals seeking platform efficiencies without traditional employment constraints.

Industry Positioning: Competitive Dynamics and Scale Advantages

Following the merger with Anywhere Real Estate—the former parent of prominent brands including Coldwell Banker—the combined entity commands one of the largest real estate professional rosters globally at more than 340,000 across owned-brokerage and franchise operations [S1]. This breadth situates Compass distinctly above smaller regional brokerages within an industry characterized by fragmentation.

Cross-branding among iconic franchises (Century 21, Better Homes & Gardens Real Estate) along with owned-brokerage prestige labels like Sotheby’s International Realty offers differentiated consumer appeal across diverse market segments [S1]. Agent switching costs are heightened by proprietary technology tools integrated into daily workflow — competing platforms lag in replicating this seamless experience at scale.

Regulatory nuances affect expansion strategies; compliance demands differ per region impacting new market entries. The merger serves as a deliberate scale-building step aimed at building moats through extensive agent networks combined with tech innovation—two levers that can reduce customer churn and enable premium commission structures.

Growth Drivers: Technology Leverage, Agent Network Synergies, and Service Diversification

Agent recruitment rates serve as leading indicators of future transaction volume growth; Q4's addition of over 800 principal agents represents sustained momentum following post-pandemic recovery phases [S4][S2]. Enhanced productivity enabled by ongoing investments in digital tools can nudge operating margins favorably over time by lowering incremental cost per transaction.

Synergistic opportunities arise from integrating Anywhere’s service platforms extending title underwriting capabilities alongside relocation services that broaden customer engagement touchpoints [S1]. Mortgage joint ventures dovetail into homebuyer financing needs forming an interconnected value chain that could boost wallet share per closing.

Technology also facilitates data-driven pricing strategies and market intelligence dissemination improving closing ratios for affiliated agents while enabling dynamic commission models aligned with local market elasticity. The cumulative effect enhances long-term retention among high-performing agents thus stabilizing recurring revenue flows.

Risks and Constraints: Market Cyclicality, Liquidity Profile, and Integration Challenges

Compass operates within the inherently cyclical U.S. residential real estate market whose volume is highly sensitive to variables such as mortgage rates (notably averaging low-6% range recently), economic growth patterns, housing inventory levels, consumer confidence fluctuations, and regulatory changes influencing affordability [S1]. Transaction count decreases cascade directly into commission revenue erosion.

Balance sheet metrics expose capital structure risks; as of March 31, 2026 cash & equivalents stand at $484 million against total debt nearing $3.15 billion with net debt approximating $2.66 billion [F1]. The current ratio of 0.84 signals current liabilities surpass current assets highlighting working capital pressures [F1]. High leverage constrains flexibility amid capital-intensive integration activities needed post-acquisition.

Legal risks persist especially relating to historical antitrust litigation associated with Anywhere although settlements have received final approval subject to appeals [S1]. Retaining agent productivity during integration phases remains an operational watchpoint given elevated competition for top talent nationally.

Outlook and Key Monitoring Points

Investor attention should focus on tracking quarterly net agent additions sustaining above historical baselines as a barometer for successful organic growth post-integration [S2][N1]. Quarterly filings will also reveal margin trajectories reflecting benefits from scaling shared technology infrastructure.

Synergy realization disclosures following Anywhere merger execution will provide clarity on cost savings and revenue cross-sell capture progress—which underpin longer-term profitability enhancement expectations [S2][S3].

Broader economic indicators including Fed policy pronouncements affecting mortgage rates will continue dictating near-term transaction volumes shaping Compass’s top-line performance visibility.

Financial Snapshot: Capital Structure and Liquidity Overview

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $484mm | |

| 2026-03-31 | ||

| Total debt | $3.1bn | |

| 2026-03-31 | ||

| Net debt | $2.7bn | |

| 2026-03-31 | ||

| Current assets | $1063mm | |

| 2026-03-31 | ||

| Current liabilities | $1262mm | |

| 2026-03-31 | ||

| Current ratio | 0.84x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Compass’s sizable debt load relative to cash reserves highlights financial leverage risks amid ongoing integration funding needs [F1][S2]. Annualized revenue approximates $7 billion underscoring sizeable scale despite negative operating income noted previously [F1]. Balancing growth investments against improved operational profitability remains central to near-term strategy execution.

This analysis synthesizes publicly filed SEC materials up to May 8, 2026 combined with corroborating news insights without offering any investment recommendation or valuation perspective. Readers should consider disclosed risks carefully when evaluating Compass's evolving business landscape.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments