Chicago Rivet & Machine Confronts Liquidity and Demand Headwinds Despite Cost Cuts

Q1 2026 results show tighter cost controls but persistent revenue pressure and going concern risks.

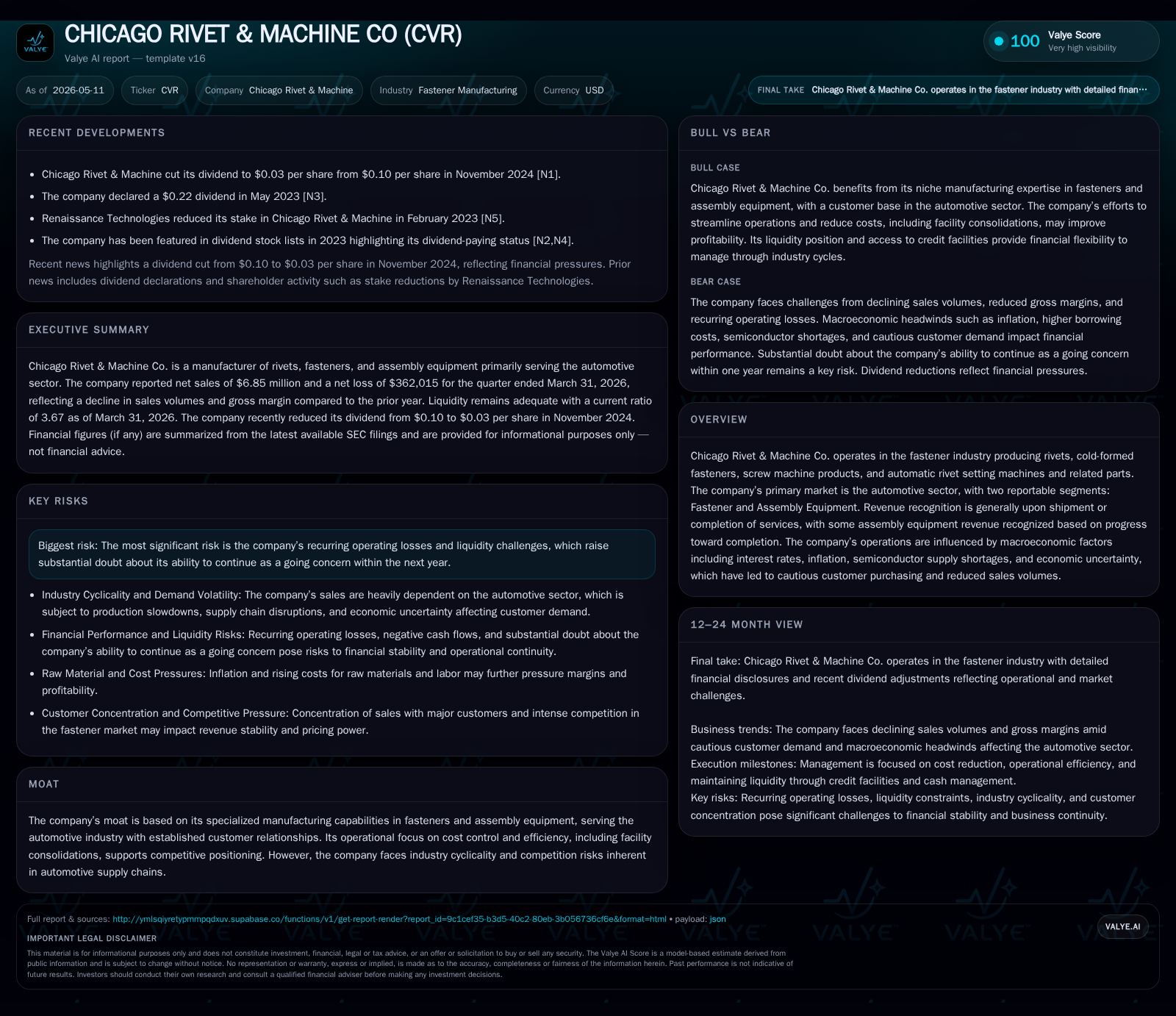

Chicago Rivet & Machine Co. reported Q1 2026 selling and administrative expenses down 15.6% year-over-year, reflecting ongoing efficiency efforts. However, revenues remain pressured by automotive industry softness, contributing to recurring operating losses and liquidity constraints, with the company relying on a $2.5 million revolving credit line. Strategic actions including asset sales and renewed sales efforts aim to stabilize operations amid continued macroeconomic uncertainty.

Latest Operating Update

Chicago Rivet & Machine Co.'s Q1 2026 filings reveal continued efforts to navigate a challenging environment characterized by industry cyclicality and macroeconomic headwinds. Selling and administrative expenses decreased to approximately $1.34 million for the quarter ended March 31, 2026, a 15.6% reduction from $1.59 million in the year-ago quarter, driven primarily by lowered salaries along with reduced outside consulting and accounting fees [S2]. These cuts lowered overhead burden from nearly 22% of sales in Q1 2025 to under 20% in Q1 2026.

Despite these expense reductions, the company remains challenged by declining top-line volumes tied closely to its core automotive customer base. The primary business segments—Fasteners (rivets, cold-formed products) and Assembly Equipment—have struggled with reduced demand amid broader automotive sector softness attributed to weakening consumer spending, global semiconductor supply issues, inflation-driven costs, and geopolitical trade tensions such as tariffs [S13]. Revenue recognition practices adhere largely to shipment or service completion timing except for certain assembly equipment contracts recognized on labor-based progress milestones [S2].

Liquidity remains constrained but not critical: as of March 31, 2026, Chicago Rivet held about $1.45 million cash against current liabilities near $3.55 million, yielding a current ratio of roughly 3.67 [F1]. Importantly, there was $1 million outstanding on its $2.5 million revolving credit facility established in early 2025 [S3]. The one-year $3 million credit agreement (including a non-revolving component that expired at year-end 2025) is renewable annually with interest at prime plus one percent subject to a seven percent floor [S2], [S5]. Financial covenants for minimum profitability and tangible net worth were breached during late 2025 and early 2026 but have been waived by lenders up through May 2026 [S5].

To shore liquidity further, the company sold its Albia manufacturing facility assets for net cash proceeds of approximately $678,000 in February 2025—a process initiated after consolidating Albia operations into its Tyrone facility which improved economies of scale and cost structure [S2], [S19], [S20]. Additional asset sales totaling $179,254 were classified as held-for-sale at December 31, 2025 and March 31, 2026 as part of ongoing strategic initiatives intended to improve cash flow and operational focus [S2].

Management continues boosting sales capabilities with targeted hires including James T. Tanner as Senior Vice President of Sales & Marketing in May 2025 who brings decades of fastener industry experience [S8]. This bolstered team is tasked not only with serving existing customers but also aggressively pursuing new contracts to reverse declining order trends observed through late 2025 into early 2026 [S13]. Yet despite these efforts and efficiency improvements announced post-Albia consolidation, recurring operating losses persisted—with an operating loss of over $381K reported for Q1 2026 versus an operating income of about $410K in the comparable quarter last year—fueling ongoing concerns about the company's going-concern status within one year post-filing date [S7], [S5].

Business Model

Chicago Rivet & Machine generates revenue primarily through manufacturing rivets and related fasteners predominantly serving original equipment manufacturers (OEMs) in the automotive sector—a market known for high volume but cyclical demand dynamics. Secondary revenue stems from producing assembly equipment such as automatic rivet setting machines which integrate with customers' production lines.

Revenue drivers are a function of shipment volumes tied to OEM production schedules combined with contract pricing structures that can include price adjustments based on raw material costs or inflation indices, though often with lag effects that compress margins during inflationary periods [S17]. Given capital requirements for specialized machinery and tooling along with rigorous quality standards mandated by automotive clients, switching costs are moderate but development cycles tend to be lengthy.

The company's revenue recognition conforms predominately to standard shipping or service completion milestones but resolves complex assembly equipment contracts using percentage-of-completion methods tied to labor inputs—reflecting long lead times on capital products [S2]. This introduces some variability in timing relative to cash collections.

Margins face pressure from fluctuating input costs (steel prices), labor wages influenced by inflationary trends persisting beyond transitory cycles,[S17] logistical challenges impacting outsourced processing fees,[S17] plus fixed cost absorption problems when volume declines reduce manufacturing utilization particularly notable at subsidiaries such as H & L Tool where over four-fifths of revenue are automotive contract-based [S17].

In response to margin compression due to lower throughput combined with inflationary input cost increases not immediately offset by pricing adjustments,[S17] management has focused on consolidating facilities (notably Albia into Tyrone) to streamline workflows and increase capacity utilization while trimming overhead across selling/admin lines.[S20]

Industry Structure and Competitive Position

The automotive supply chain for fastening systems is highly competitive yet dominated by firms able to provide precision-engineered parts meeting exacting durability standards under tight delivery timelines—the kind Chicago Rivet specializes in with decades-long relationships forming a core moat.

That said, the sector's inherent cyclicality tied closely to vehicle production volume swings exposes companies like Chicago Rivet to sharp demand fluctuations amplified by emerging threats such as semiconductor shortages limiting new vehicle production elsewhere downstream.

Competition arises from both large global fastener manufacturers offering integrated product suites under OEM contracts as well as smaller niche producers focusing on specialized components or regional distribution advantages.

Chicago Rivet's additional niche lies in its proprietary assembly equipment which adds value through customized solutions enabling customers' manufacturing automation—however this segment remains relatively small and susceptible to longer project cycles congested by economic uncertainties.

Pricing power is limited given the commoditized nature of many fastener products but augmented somewhat through relationship-derived repeat orders plus incremental assembly systems innovations. Customer retention hinges on quality reliability backed by on-time delivery amidst rising demands for just-in-time inventory syncs.

Growth Drivers

Growth prospects hinge structurally on recovery or expansion within the North American automotive manufacturing ecosystem where Chicago Rivet's majority revenue derives.

Key drivers include:

- Automotive Production Volumes: Increases would lift order backlogs directly.

- New Product Awards: Winning customer contracts for next-gen vehicle platforms could ramp volumes starting mid-to-late fiscal periods.[S13]

- Pricing Adjustments: Gradual pass-through of inflationary cost pressures improves gross margin conversion.

- Operational Efficiencies: Facility consolidations like Albia/Tyrone enhance margins via economies of scale.

- Sales Force Expansion: Leveraging seasoned executive hires for market penetration could aid top-line stability.

Expansion beyond automotive—such as industrial machinery markets—or diversification within assembly equipment may present longer-term growth avenues if developed successfully given competitive pressures.

Risks / Watchpoints / Growth Constraints

The dominant risk profile centers on:

- Going Concern Doubts: Recurring operating losses alongside liquidity strain raise fundamental viability questions despite short-term lender waivers.[S5]

- Automotive Cyclicality: Exposure leaves revenues vulnerable to downstream OEM production cuts or shifts in sourcing strategies.

- Inflationary Costs vs Pricing Lag: Persistently elevated input costs squeezing margins before contractual pass-throughs take effect.[S17]

- Credit Reliance: Ongoing reliance on revolving credit facilities with expiring maturities necessitates refinancing or alternative capital raises.

- Customer Concentration: Dependence on few large OEM clients increases vulnerability.

- External Macro Factors: Tariffs, semiconductor constraints, economic volatility could suppress demand unpredictably.

- Competitive Pressure: Larger producers' scale advantages could erode pricing leverage or limit market share expansion.

Adverse movement on any frontline growth drivers coupled with failure to implement ongoing strategic actions would likely exacerbate financial distress.

What To Watch Next

Important upcoming indicators will include:

- Q2 / H1 Earnings Reports: To gauge traction of sales efforts amid evolving demand signals.

- Order Backlog Trends: Whether order intake progresses toward pre-downturn levels per management commentary.[S13]

- Financing Developments: Renewal status or amendments of credit agreements post-August maturity.

- Asset Sales Execution: Progress on disposal of classified assets for liquidity enhancement.[S2]

- Margin Trajectory: Impact of price realization vs input costs over time.

- Customer Wins / Losses: New contract announcements or cancellations affecting projected volumes.

- Macroeconomic Environment: Changes in tariff policies or supply chain disruptions influencing demand causally.

Close attention should be paid to management disclosure surrounding these milestones given substantial doubt status persists.

Financial Profile Summary

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $1446794 | |

| 2026-03-31 | ||

| Current assets | $13mm | |

| 2026-03-31 | ||

| Current liabilities | $4mm | |

| 2026-03-31 | ||

| Current ratio | 3.67x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As of Q1 2026: Year-end total debt stood at zero per last available data but revolving credit draws reflect operational funding needs.[F1], [S3] Declining revenues have recently resulted in operating losses (over $380k loss Q1 ’26), underscoring margin challenges despite expense discipline improvements.[F1], [S7] Strategic asset sales contributed non-recurring gains ($339k) earlier but won’t sustain recurring operational cash flow indefinitely.[S19]

The company’s liquidity situation remains fragile though mitigated somewhat by high current ratios; liquidity enhancement via credit lines coupled with asset dispositions will need continuation along with successful demand uplift execution.[F1], [S2], [S3]

Disclaimer: This analysis is based solely on publicly filed financial data and disclosures without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments