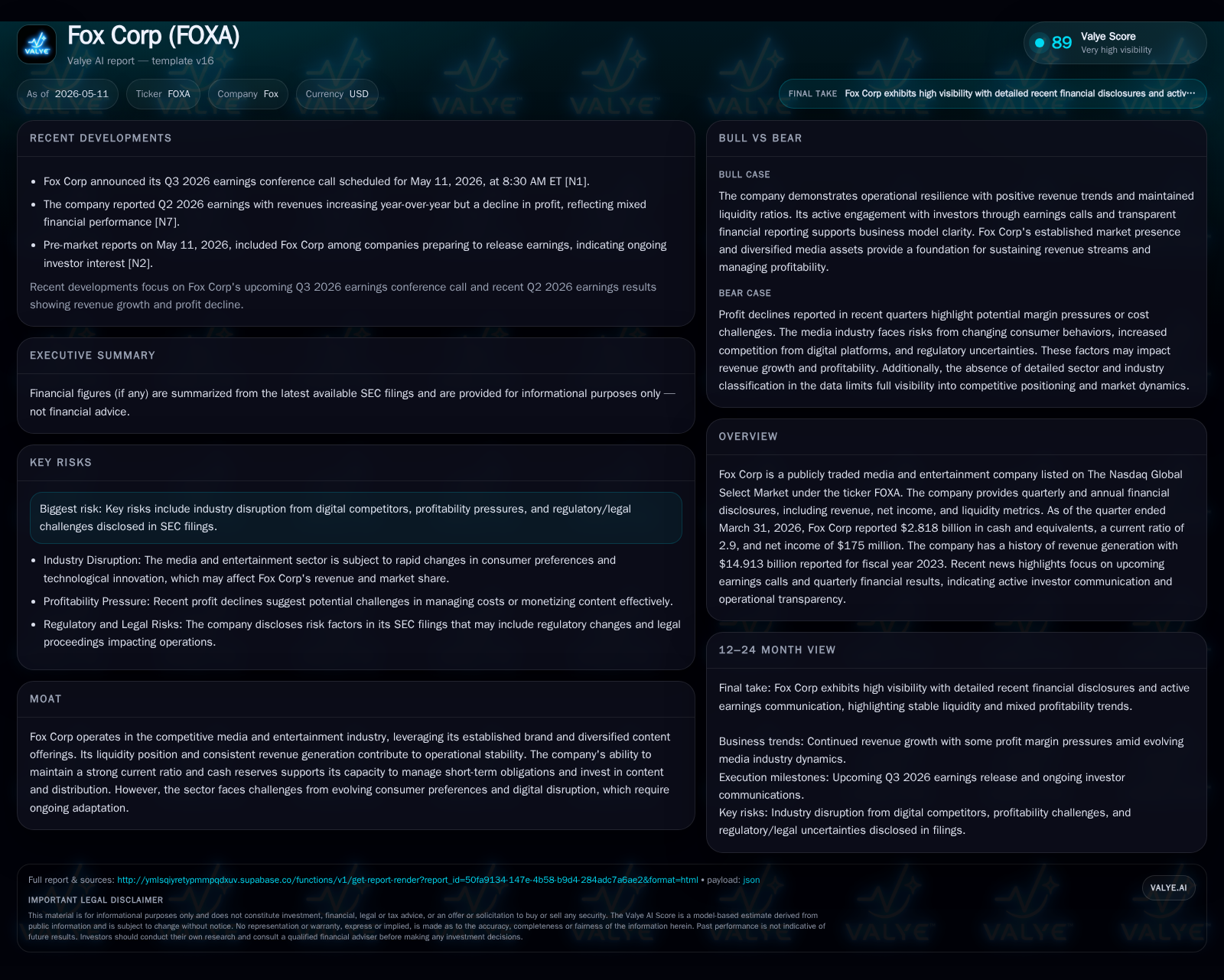

Fox Corp's Q3 2026 Financial Update Highlights Operating Resilience and Strategic Challenges

Fox Corp’s latest quarterly results underscore its solid liquidity and ongoing revenue generation within a rapidly evolving media landscape.

In Q3 2026, Fox Corp demonstrated stable operational performance marked by $175 million in net income and a robust current ratio of 2.9, supported by $2.8 billion in cash and equivalents. Despite these strengths, the company faces strategic challenges from shifting consumer habits, digital competition, and regulatory pressures that temper near-term profitability growth. Fox Corp’s entrenched brand and diversified content portfolio anchor its competitive position, while growth levers include political advertising cycles and digital initiatives. The outlook hinges on successful navigation of industry disruption and maximizing emerging digital revenue opportunities.

Q3 2026 Operating Highlights and Why They Matter

Fox Corporation’s Q3 2026 quarterly filing (10-Q dated May 11) reveals a net income of $175 million alongside healthy liquidity metrics including $2.818 billion in cash and equivalents and a current ratio of 2.9 [S2][F1]. This financial stability underscores the company’s resilience amidst an industry grappling with digital transformation.

The quarter’s financial results reflect ongoing revenue generation predominantly from its core media assets — broadcast TV networks, cable channels, and notably political advertising revenues — even as overall earnings showed some contraction pressure consistent with sector-wide trends [N14]. The accompanying 8-K filing confirms no unexpected material events disrupting operations but highlights active management focus on streamlining costs while investing selectively in content and distribution initiatives [S3].

This operative snapshot is crucial given the entrenched competitive pressures facing Fox Corp, where steady cash flow supports both day-to-day functioning and strategic transitions towards digital platforms.

Fox Corp’s Business Model: Content, Distribution, and Monetization Mechanics

Fox Corp operates through multiple vertically integrated segments centered on content production and rights ownership, cable network operation, broadcast station ownership, and live sports media rights. Revenue arises primarily from advertising sales—both national and local—carriage fees from pay-TV operators for network distribution, and licensing agreements.

Advertisers constitute the primary paying customers, attracted by Fox’s extensive audience reach across linear TV combined with growing digital offerings. CPM (cost per thousand impressions) pricing remains a fundamental metric underpinning revenue mechanics; premium content such as live sports or politically significant programming commands higher CPMs due to enhanced viewership engagement [S1].

Political advertising introduces a highly cyclical revenue input that significantly spikes in election years, representing a lumpy but lucrative component that bolsters annual top-line figures intermittently [S1][N2].

Outgoing contracts with affiliates typically sustain volume stability though overall viewing hours show signs of shift due to consumer preference changes toward OTT (over-the-top) services. Fox’s brand recognition and integration across multiple sports franchises create switching costs that support pricing power despite these headwinds.

Competitive Dynamics and Industry Structure in Media & Entertainment

The U.S. media ecosystem pits legacy broadcasting entities like Fox against consolidating peers (Disney/Warner Bros Discovery), emergent streaming giants (Netflix, Amazon), and nimble digital ad platforms (Google, Meta). Advertising spend—a critical substrate for Fox’s model—is highly contested with shifts favoring programmatic digital formats over traditional linear buys [S1][N4][N6].

Fox retains competitive advantages through exclusive sports broadcasting rights (e.g., NFL games), live event coverage, and news programming which are less susceptible to time-shifted viewing-induced monetization loss. However, cross-platform fragmentation dilutes broadcaster market share over time.

Regulatory frameworks including FCC ownership rules affect station holdings and must be navigated carefully amid potential consolidation attempts [S7]. Syndication rights handling adds complexity in content monetization strategy as Fox balances direct distribution benefits against licensing fees.

Overall market structure incentivizes scale economies in production/distribution yet also demands nimble adaptation toward hybrid OTT-linear presence to maintain advertiser appeal.

Growth Drivers: Digital Innovation, Advertising, and Political Cycle Impacts

Key growth catalysts for Fox include leveraging digital expansion—by scaling streaming offerings to capture cord-cutters—and capitalizing on cyclical surges during political campaign seasons when ad expenditures rise sharply [N7][S2]. These dynamics support periodic margin spikes that help offset secular declines in baseline linear ad rates.

Incremental investments target original programming for emerging platforms aligned with consumer trends favoring on-demand content [S2]. Enhancing data capabilities for targeted advertising is another vector whereby Fox tries to strengthen advertiser ROI metrics relative to big-tech competitors.

Live sports content continues to function as a vital driver sustaining higher CPMs due to real-time engagement robustness [S1]. Expansion or renewal of key rights deals will influence revenues materially over mid-term horizons.

These elements impose cost burdens or restrict strategic options.

Digitally native competitors erode audience engagement from traditional broadcasts reducing price realizations; this structural shift pressures margins necessitating continuous efficiency improvements [S9]. The volatile nature of political advertising further adds cyclicality compounding forecasting difficulty.

Further constraints arise from escalating content acquisition costs amid bidding wars for premium sports or entertainment properties that strain operating flexibility [S1]. Concurrently, evolving data privacy regulations may limit targeting precision reducing ad effectiveness.

Key Upcoming Catalysts and Investor Watchpoints

Looking ahead, Q4 fiscal performance will heavily depend on the upcoming U.S. election cycle’s impact on political advertising volumes which historically provide sharp revenue inflections [N2][S2]. Investors should monitor guidance updates during earnings calls for clarity on how digital monetization initiatives progress versus cost structures.

Regulatory developments around media ownership or new FCC rules warrant close attention as outcomes can decisively affect consolidation strategies or station acquisitions/divestitures.

Execution milestones including renewal or expansion of sports broadcast rights agreements will serve as important signposts indicating sustained competitive positioning.

Finally, any shifts in affiliate carriage terms or emerging partnerships in OTT ecosystem could signal directional changes in distribution economics.

Latest Financial Snapshot and Balance Sheet Position

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Current assets | $7.5bn | |

| 2026-03-31 | ||

| Current liabilities | $2.6bn | |

| 2026-03-31 | ||

| Current ratio | 2.9x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value | Date |

|---|---|---|

| Cash & Equivalents | $2.818 Billion | |

| 2026-03-31 | ||

| Current Ratio | 2.9 | |

| 2026-03-31 | ||

| Total Debt | $6.65 Billion | |

| 2025-06-30 |

The reported liquidity profile underscores Fox Corp's capacity to meet short-term obligations comfortably while sustaining investment programs critical for competitive resilience. Although substantial debt exists reflecting financing arrangements for content rights acquisitions or capital expenditures, strong cash reserves ameliorate immediate leverage concerns [F1][S2]. This financial footing enables the firm to maneuver amid sector volatility without compromising operational continuity.

This analysis relies solely on current filings from Fox Corporation's SEC disclosures alongside recent public reporting without conjecture beyond sourced data. It aims to provide an informed assessment of the company's operating posture within its evolving industry framework without investment recommendations or price commentary.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments