Emerald Holding Secures Financing for Merger While Driving Steady Growth in Live Events

Emerald Holding reports solid organic revenue growth and robust cash flow while announcing merger financing backed by Apollo-affiliated funds.

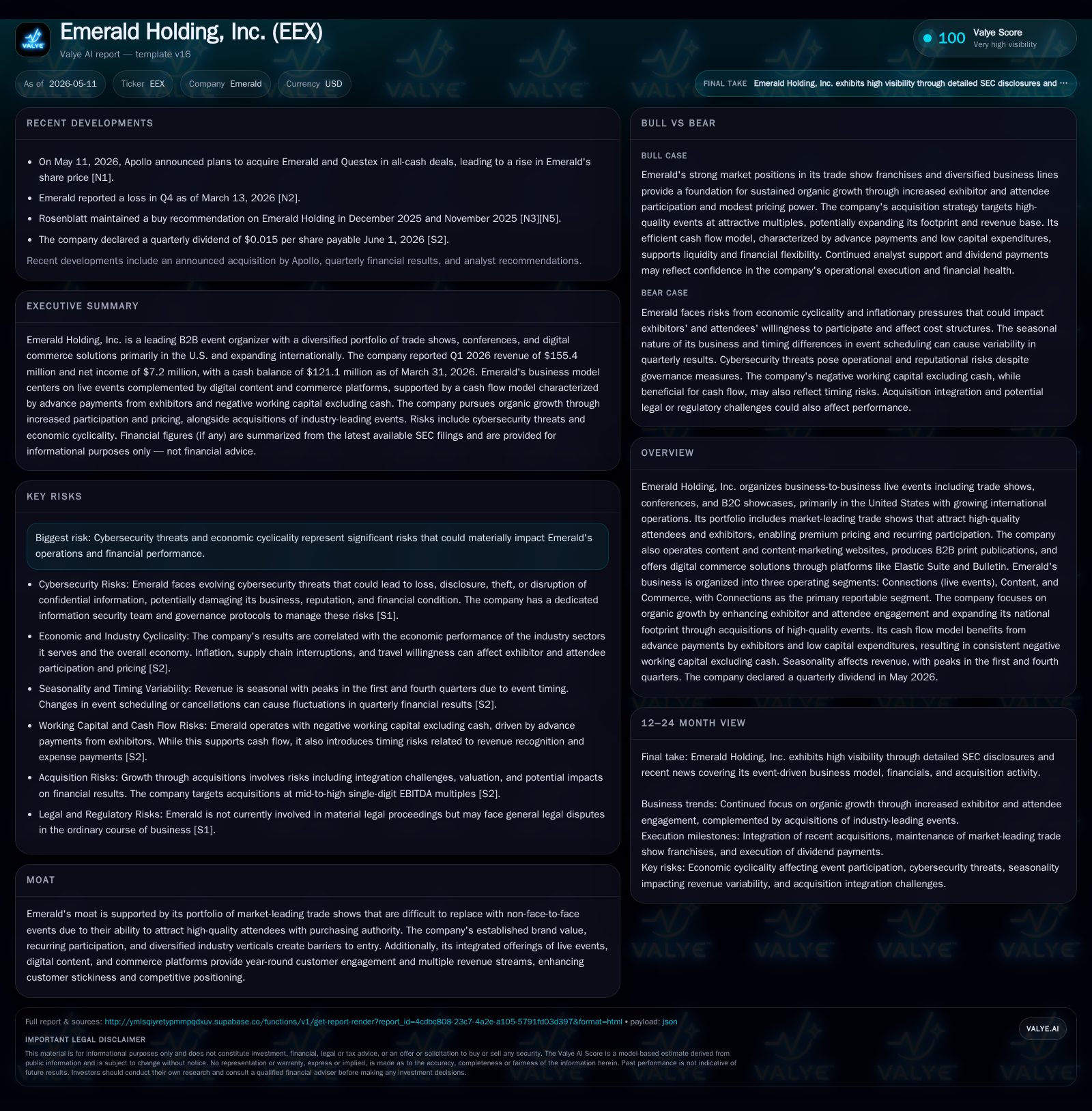

In its latest quarter ending March 31, 2026, Emerald Holding, Inc. demonstrated steady organic growth in its core live events business alongside improved free cash flow generation, despite increased acquisition-related expenses that modestly impacted margins. The company concurrently announced a merger agreement with secured equity and debt financing commitments sufficient to cover merger consideration and debt repayment, marking a pivotal near-term event. Emerald’s integrated model, spanning live trade shows, digital content, and commerce solutions, sustains participant engagement and premium pricing power. The merger promises potential synergies and strategic expansion but brings execution and integration risks amid macroeconomic cyclicality. Going forward, monitoring event attendance recovery post-pandemic and merger closing milestones will be crucial.

Quarterly Operating Update Highlights

Emerald Holding's first quarter of fiscal 2026 closes on a note of steady core performance combined with transformative ownership developments. According to the May 11, 2026 Form 10-Q [S2], total revenues for the quarter reached $155.4 million with organic revenue increasing 1.1% year-over-year to $151.8 million [S4]. This organic growth reflects modest demand gains within live events against a backdrop of ongoing industry normalization post-pandemic.

Adjusted EBITDA dipped slightly to $52.7 million from $53.6 million the prior year period—a decline primarily driven by rising selling, general & administrative (SG&A) expenses including $3-4 million in acquisition-related transaction and integration costs plus contingent consideration adjustments [S20]. Despite margin pressure, free cash flow nearly doubled to $26.9 million reflecting Emerald’s effective working capital dynamics supported by prepayments from exhibitors collected well in advance of events [S4][S27].

An important corporate milestone transpired concurrently—a merger agreement executed on May 9, 2026 with Emma Buyer LLC (an Apollo funds-affiliated holding company), supported by committed equity and debt financing adequate for all merger consideration plus transaction-related expenses [S3]. This sponsorship provides immediate clarity around capital structure overhaul and introduces potential scale-related synergies.

The board also declared a dividend of $0.015 per share payable June 1, underscoring confidence in near-term cash flow stability despite integration burdens [S2]. Taken together, these results highlight a resilient operational base augmented by significant structural change pending merger close.

Core Business Model and Revenue Dynamics

Emerald Holding operates primarily within the business-to-business live events sphere through its flagship Connections segment encompassing market-leading trade shows across diversified industry verticals [S1]. These franchises are typically among the largest or sole major shows in their domains with strong brand recognition that attracts high-quality attendees possessing purchasing authority.

Revenue is mainly driven by exhibitors who contract exhibit space well ahead of events—often paying deposits as early as twelve months beforehand—with final payments due shortly before event staging [S1][S27]. This mechanism generates dependable deferred revenues creating negative working capital excluding cash balances; essentially, Emerald receives substantial cash upfront preceding related expenditures providing an efficient self-funding model.

Complementing Connections are Content platforms delivering specialized B2B marketing websites and print publications aligned with event sectors along with Commerce solutions such as Elastic Suite facilitating digital merchandising for manufacturers and retailers [S1]. Together these elements create year-round engagement channels enabling cross-sell opportunities beyond episodic event schedules.

This multi-channel ecosystem increases customer stickiness as exhibitors leverage integrated experiences encompassing physical presence and digital touchpoints enhancing lead generation and brand building efforts – a differentiation against competitors reliant solely on either virtual offerings or traditional trade show formats.

Industry Positioning and Competitive Advantages

Within the fragmented live event industry undergoing digital disruption and economic cyclicality, Emerald stands out owing to its portfolio of established franchise events recognized as "must-attend" venues for procurement decision-makers [S1][N1]. The face-to-face interaction element remains highly valued especially in sectors requiring complex sourcing decisions where physical evaluation or networking is critical.

Competitive moats are further reinforced by: (i) sustained high-quality attendee pools granting exhibitors immediate access to purchasing influencers; (ii) recurring annual or multiple editions that create habitual participation; (iii) sector diversification insulating against concentration risk; and (iv) complementary content-commerce offerings securing continuous engagement throughout the year [S1][N1].

While virtual events have gained traction during pandemic interruptions, firms like Emerald benefit from limited substitution due to persistent demand for tactile demonstrations, relationship-building peer networks, and trend discovery activities intrinsic to live formats [S1]. Additionally, Emerald’s investment in technology-driven data analytics enhances exhibitor ROI measurement adding incremental value beyond traditional event services.

Key Growth Drivers and Expansion Opportunities

Organic growth has been stable but incremental as Emerald continues refining exhibitor/attendee experiences via enhanced digital tools that heighten engagement quality leading to increased renewal rates [S2]. Expansion strategies include broadening geographic footprint through acquisition of high-quality regional shows filling gaps in national coverage—particularly underrepresented verticals—and bolstering international operations notably within the U.K., thereby unlocking new revenue pools [S2][S3].

Furthermore, digital platform monetization presents scalable upside through Elastic Suite’s role as a bridge between physical exhibitions and continuous commerce transactions supporting manufacturers’ shifting distribution models [S1]. Multi-edition franchises released throughout the year provide rhythmically spaced revenue milestones improving predictability compared to one-off annual events.

Cross-selling among Connections clients into Content subscriptions or Commerce tools supports deeper wallet share extraction while fostering annualized relationships beyond episodic booth sales [S2]. Such synergy potential is likely an underpinning assumption embedded within Apollo’s financing commitments aiming at realizing operational efficiencies post-merger [S3].

Risks and Potential Headwinds

Cybersecurity remains a material risk given Emerald’s custody of sensitive attendee/exhibitor data which could suffer breaches causing reputational damage or regulatory losses; however robust governance protocols described indicate active Board oversight via the Audit Committee coupled with experienced IT leadership deploying layered security programs inclusive of external consultant benchmarking [S1].

Economic cyclicality imparts volatility risk since exhibition budgets are often discretionary line items susceptible to macroeconomic downturns reducing attendee numbers or exhibitor spend impacting revenues directly [S2][S1]. The pending merger introduces execution risks including distraction from core operations during integration phases alongside incremental acquisition-related SG&A pressures evident already in reported quarters which could temporarily blunt margin expansion [S2][S20].

Currency fluctuations related to international expansions expose financial reporting variability though currently appear manageable given limited foreign operations relative to the overall portfolio [S25]. Additionally, dependence on large marquee shows concentrates risk if single-event disruptions occur.

Upcoming Catalysts: Milestones and Capital Markets Impact

Near-term developments will revolve around timely completion of the Apollo-backed merger—expected over upcoming quarters—which will reshape ownership structure with private equity stewardship potentially accelerating strategic investments or cost rationalizations [S3][N1]. Monitoring regulatory approvals required for deal closing is essential for timing visibility.

Operationally key calendar events such as performance of flagship trade shows during peak seasonal periods will serve as barometers for demand recovery trajectories or cyclic headwinds influencing forward bookings trends critical to revenue projections [S2]. Dividend declarations suggest continued shareholder returns prior to transaction consents reflecting management comfort with cash flow sustainability [S2].

Post-close balance sheet optimization through refinancing will be important given current net debt approximating $433.6 million (total debt roughly estimated at $554.7 million less cash reserves of $121.1 million as of end-March 2026) requiring efficient capital management under new ownership constraints [F1][S3].

Latest Financial Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $121mm | |

| 2026-03-31 | ||

| Current assets | $277mm | |

| 2026-03-31 | ||

| Current liabilities | $304mm | |

| 2026-03-31 | ||

| Current ratio | 0.91x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Latest Quarter |

|---|---|

| Cash & Equivalents | $121.1M |

| Adjusted EBITDA | $52.7M |

| Free Cash Flow | $26.9M |

| Organic Revenue | $151.8M |

Liquidity remains solid with sufficient cash reserves supporting operational needs amidst integration spend pressures noted in SG&A lines which contained acquisition-related fees totaling approximately $3–4 million this quarter including contingent consideration remeasurements [S20][F1]. Adjusted EBITDA contraction was marginal (-1.7%), whereas cash flow improvements underscore effective working capital management tied closely to advance exhibitor payments characteristic of the trade show business model enhancing conversion efficiency into free cash flow metrics used internally for dividend coverage and debt servicing validation.

Disclaimer: This analysis is based exclusively on publicly available SEC filings dated through May 11, 2026, supplemental news sources cited herein, and XBRL company facts as specified. It does not constitute investment advice or recommendations nor does it include non-public information about Emerald Holding Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments