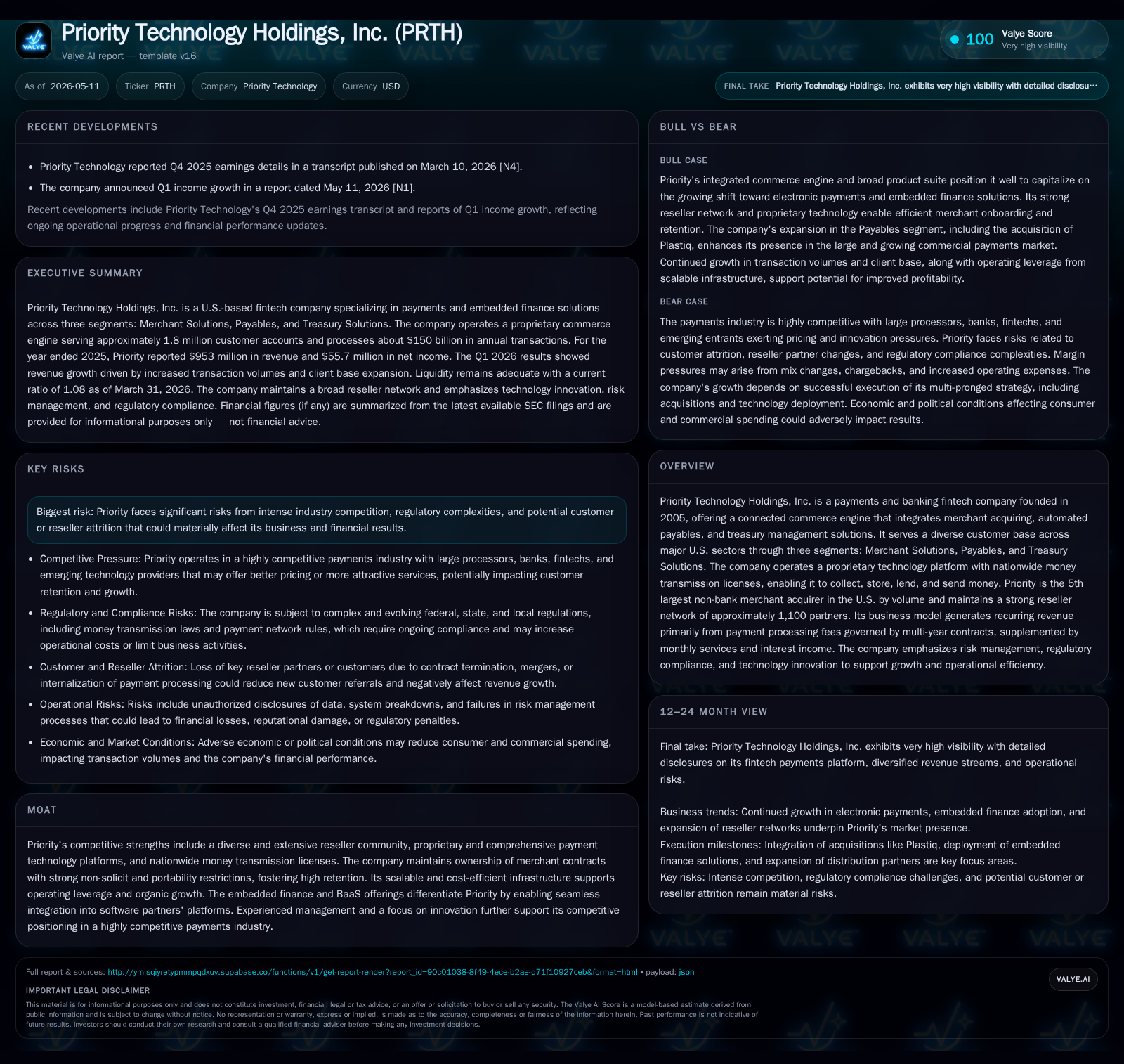

Priority Technology Holdings Extends Lead in U.S. Merchant Acquiring With Strategic Growth and Cloud Migration

Priority’s Q1 2026 results reveal increased investment in growth initiatives and cloud migration amid expanding reseller network and embedded finance integration.

In its latest quarterly filing, Priority Technology Holdings reported a 27.4% rise in selling, general, and administrative expenses primarily driven by professional and legal costs related to its ongoing go-private project, as well as marketing and software investments to accelerate growth and cloud migration. The company remains the fifth largest non-bank merchant acquirer in the U.S., leveraging a proprietary payments platform, a broad reseller community, and nationwide money transmission licenses to deliver integrated merchant acquiring, payables, treasury management, and embedded finance solutions. Growth prospects hinge on organic expansion through reseller partnerships, cloud-based scalability enhancements, and innovative fintech offerings, though risks include intense competition, regulatory complexities, and execution challenges around customer retention.

Q1 2026 Operational Update: Investments in Growth and Technology

Priority Technology Holdings reported meaningful operational developments in its first quarter ended March 31, 2026 [S2]. Selling, general and administrative (SG&A) expenses climbed to $19.2 million from $15.1 million a year earlier—a 27.4% increase driven largely by professional and legal fees tied to the company's active go-private project alongside stepped-up marketing efforts supporting overall growth initiatives and cloud migration expenses. These investments also reflect costs associated with acquired assets integration but were partially offset by lower legal expenses related to its prior secondary share offering.

Despite increased SG&A spend indicating elevated near-term operating costs for strategic transformation initiatives including platform modernization via cloud migration [S2], Priority's core Merchant Solutions segment sustained momentum with revenues up by approximately $10.1 million to $161.8 million from Q1 2025 levels accompanied by adjusted EBITDA growth of $2 million to $27.7 million [S2]. This suggests underlying resilience in payment processing volumes underpinning reinvestment capacity.

Comprehensive Commerce Engine: Payment Processing Plus Embedded Finance

Priority uniquely positions itself beyond traditional payment processors by operating a connected commerce engine purpose-built to collect, store, lend, and send money across three integrated segments: Merchant Solutions (merchant acquiring), Payables (automated bill payments), and Treasury Solutions (cash flow acceleration through treasury management) [S1]. The technology platform supports all prominent payment forms—including card acquiring & issuing, ACH transfers, check processing, and wires—coupled with embedded finance or Banking-as-a-Service (BaaS) products facilitating seamless incorporation into partner software ecosystems.

This holistic approach enables Priority's customers—ranging from SMBs to enterprise-grade independent software vendors (ISVs)—to automate their financial lifecycles under one scalable umbrella with an emphasis on accelerating working capital optimization while maintaining security assurances critical for handling sensitive financial data [S1]. Embedded finance features particularly differentiate Priority by empowering ISV partners with native monetization levers without managing complex payments infrastructure themselves.

Industry Positioning: Fifth Largest Non-Bank Merchant Acquirer in the U.S.

According to the Nilson Report cited in its latest annual filing [S1], Priority ranks fifth among U.S.-based non-bank merchant acquirers measured by transaction volume—a notable achievement given industry's scale concentration around large incumbents after major mergers like Global Payments-Worldpay consolidation. Priority serves approximately 1.8 million customer accounts processing around $150 billion annually across diverse sectors including Retail, Hospitality, Healthcare, Real Estate, Government Contracts, Utilities, Education & Non-Profit entities [S1].

This scale affords Priority operational leverage essential for competing effectively against both entrenched incumbents at the top tier and nimble fintech challengers seeking share in the fast-evolving payments space with superior user experience claims.

Competitive Advantages: Proprietary Platform, Reseller Network, and Licenses

Priority’s proprietary technology platform is architected for scalability and cost efficiency supporting multi-payment rail acceptance—from cards to wires—with extensive automation driving down operating expenses while maintaining flexibility for rapid feature rollout [S1]. Nationwide money transmission licenses legally empower operations across covered jurisdictions without reliance on third-party license holders—a significant barrier for competitors dependent on partnerships.

A cornerstone of Priority's moat involves managing contracts directly with merchants secured under rigorous non-solicitation clauses restricting contract portability; this fosters strong retention among a broad reseller partner network approximating 1,100 members [S1]. The reseller ecosystem acts as both sales distribution channel and customer relationship extension facilitating organic volume growth within existing portfolios supported by agile tools provided to resellers for portfolio management enhancement.

Strategic Growth Drivers: Reseller Expansion, Cloud Migration, and BaaS Integration

The primary levers driving Priority’s growth agenda involve sustained organic expansion through deeper penetration of reseller networks coupled with continuous onboarding of new merchants incentivized via sticky contract structures [S1]. Investments reflected in recent marketing spend enhance lead generation while expanded software expenses underscore technical upgrades including cloud migration designed to increase system availability and reduce latency fostering better user experience [S2].

Acquisitions also supplement organic growth creating product breadth particularly within Treasury Solutions where interest income benefits from larger total account balances post strategic buys such as Sila [S25]. The BaaS/embedded finance vertical creates cross-selling avenues underpinning sustainable fee revenue streams leveraging APIs that integrate natively into partner platforms reducing friction associated with external payment providers [S1].

Risks: Regulation, Competition, and Customer Retention Challenges

Operating within payments ubiquity subjects Priority to intense regulatory scrutiny particularly regarding information security given its custody of sensitive consumer/merchant financial data—cybersecurity threats remain elevated as documented meticulously in annual filings citing multiple risk vectors including sophisticated threats targeting data confidentiality potentially leading to reputational damage or liability exposure despite insurance coverage [S16].

Regulatory complexity amplifies around bank-nonbank partnerships amid enforcement focus on internal controls encompassing risk management frameworks further highlighted by ongoing investigations over prepaid debit card programs [S19]. Competition is fierce across multiple fronts from big-tech players offering integrated super-app ecosystems to challenger fintechs pressing on price compression potential [S1]. Maintaining reseller goodwill is critical; contract provisions notwithstanding attrition risk exists if competitors provide better service or pricing advantages resulting in lost volume or higher sales cost.

Upcoming Catalysts: Go-Private Progress, New Contract Wins, and Platform Enhancements

Short- to medium-term catalysts center on monitoring milestones related to the go-private transaction led by principal shareholder Thomas Priore which may realign company governance while incurring near-term expenses affecting earnings visibility [S13]. Tracking announcements regarding new reseller agreements or expansions within existing portfolios will serve as demand signals supportive of revenue continuity. Cloud migration completions anticipated could concurrently unlock efficiency gains lowering future operational costs while driving enhanced uptime—a customer retention factor crucial for high-volume processing entities [S2]. Product innovation pipelines including enhanced embedded finance capabilities offer upside optionality if adoption accelerates seamlessly across fintech partnership channels.

Financial Overview: Balancing Investment with Strong Liquidity

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $92mm | |

| 2026-03-31 | ||

| Total debt | $1062mm | |

| 2026-03-31 | ||

| Net debt | $970mm | |

| 2026-03-31 | ||

| Current assets | $1585mm | |

| 2026-03-31 | ||

| Current liabilities | $1462mm | |

| 2026-03-31 | ||

| Current ratio | 1.08x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Priority’s liquidity position remains robust post Q1 2026 reporting with cash & equivalents at $92.2 million against total consolidated debt approximating $1.06 billion yielding a net debt position close to $970 million reflective of sector-typical leverage for payment processors deploying capital expansively into technology transformation strategies [F1][S2]. Working capital improved distinctly year-over-year from approximately $62 million to nearly $123 million illustrating strengthened short-term liquidity cushioning operational funding needs amid elevated investment spend.

Revenue visibility benefits from recurring fee structures primarily anchored in multiyear merchant contracts supplemented by monthly services fees plus growing treasury interest income streams generated from consistently rising account balances [S25][S1]. However incremental SG&A costs tied mostly to one-time transactional events like going private suggest near-term earnings dilution while longer-term effects remain contingent on successful execution.

Disclaimer: This analysis is based solely on publicly available information as of May 11th, 2026 including SEC filings referenced herein. It does not constitute investment advice or an offer to buy or sell securities. Investors should perform their own due diligence before making any financial decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments