Cosmos Health Advances AI Drug Repurposing and Nutraceutical Expansion Despite Margin Pressures

The latest quarterly update highlights operational growth in proprietary brands and innovation pipelines amid tightening financial margins.

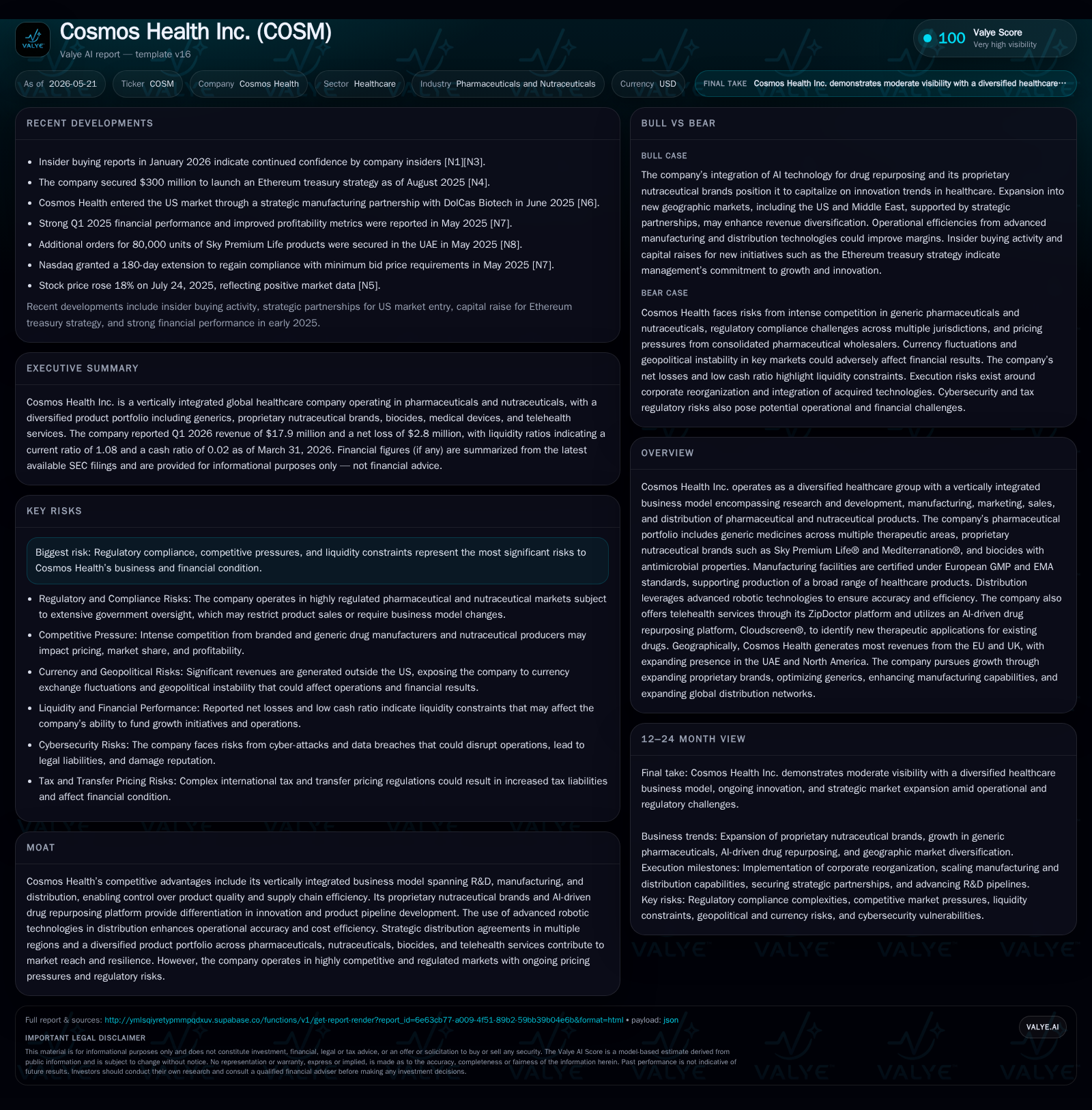

Cosmos Health Inc. continues to expand its presence in pharmaceuticals and nutraceuticals through vertically integrated operations, emphasizing its AI-powered drug repurposing platform Cloudscreen and proprietary nutraceutical lines such as Sky Premium Life®. The company’s latest quarterly filing shows sustained revenue growth coupled with ongoing operating losses driven by investments in R&D and global distribution expansion. Key growth drivers include advancing clinical trials for new product candidates like CCX0722 for obesity, while risks center on regulatory compliance, pricing pressures, and capital requirements for scaling. Market diversification via strategic agreements in the UAE and other regions supports the company's international reach as it prepares for further commercialization milestones.

Recent Operating Update

Cosmos Health's most recent quarterly filing dated May 20, 2026 ([S2]) reflects continued operational advancement across its diversified healthcare segments. The company reported ongoing revenue generation driven by both its portfolio of generic pharmaceuticals and proprietary nutraceutical brands such as Sky Premium Life® and Mediterranation®. While exact revenue figures for Q1 2026 are not separately disclosed, the annual revenue for 2025 reached $65.3 million with a substantial gross profit increase of 83% year-over-year ([S3]). Despite this top-line growth, Cosmos Health continues to operate at an operating loss reflecting sustained investment in research & development, international market penetration efforts, and corporate restructuring aimed at long-term scalability ([F1],[S1]).

Key near-term developments include progress in clinical milestones. The obesity management candidate CCX0722 is finalizing scale-up production ahead of human clinical trials anticipated in the second half of 2026 ([S18]). Oncology drug candidates based on Cloudscreen's AI-driven repurposing platform are progressing preclinical studies with patent applications filed for CNS cancer and hematologic malignancies ([S6],[S16]). These projects exemplify Cosmos Health's strategic shift to leverage innovation as a core growth driver alongside its established generics business.

Business Model

Cosmos Health operates a vertically integrated business model spanning drug research & development, manufacturing under stringent EMA/GMP standards, marketing, sales, and distribution. This structure gives the company direct oversight of product quality control from pipeline conception to consumer delivery ([S1]). Revenue is generated primarily through sales of generic pharmaceutical products to pharmacies and wholesalers within the EU and UK markets—its core sales base—and increasingly through proprietary nutraceutical products marketed globally via distribution partnerships ([S27],[S25]).

The company's pharmaceutical portfolio features generic equivalents across several therapeutic areas sold at cost-effective price points relative to branded medicines. Nutraceutical products focus on preventive health with branded formulations targeting immunity, energy, stress relief, bone/joint health—categories with strong consumer demand trends post-pandemic ([S1],[S9]). Complementing this is Cosmos Health's provision of telehealth services through ZipDoctor and biocide products with antimicrobial applications.

Distinctive in its offering is Cosmos Health’s AI-powered Cloudscreen®, which enables accelerated drug repurposing discovery—identifying novel therapeutic indications for existing compounds—which may lower development risk profiles compared to de novo drugs. This technological asset enriches the company’s innovation pipeline with patent-protected candidates enhancing future revenue potential ([S1],[S6],[S11]).

Revenue mechanics rely heavily on volume-driven sales through broad wholesale networks supplemented by direct-to-consumer online channels (e.g., Amazon UK for nutritional supplements). Pricing dynamics reflect competitive generic drug market pressures balanced against proprietary product pricing power which can command premium margins if brand equity strengthens ([S8],[S27]). Contractual distribution agreements shift operational burdens like logistics and regulatory compliance onto local partners while securing committed purchase volumes.

Industry Structure and Competitive Position

Cosmos Health competes within multiple segments—generic pharmaceuticals, nutraceuticals, biocides, telehealth—which have distinct structural attributes. The generics sector is characterized by intense pricing competition due to consolidation among wholesalers who exert significant purchasing leverage ([S27]). Regulatory complexity is elevated given stringent EU-wide standards combined with country-specific nuances impacting time-to-market.

In nutraceuticals—a rapidly growing $636B+ global market projected to surpass $1.2T within a decade—competition includes numerous branded players emphasizing quality differentiation and retail accessibility ([S1]). Cosmos Health’s dedicated portfolio featuring Sky Premium Life® granted exclusive regional rights enhances competitive positioning by building brand recognition supported by multi-channel distribution.

The AI-based drug repurposing space represents an emerging segment where Cosmos Health occupies a niche frontier combining pharmaceutical innovation with digital health capabilities. While large pharmaceutical companies increasingly invest in repurposing strategies internally or through partnerships, Cosmos Health’s ownership of Cloudscreen grants it unique agility in early-stage pipeline generation ([S6],[S11]).

Operationally, Cosmos Health benefits from vertical integration that mitigates supply chain disruptions—a critical advantage visible during recent global healthcare crises—and robotic automated distribution which drives accuracy and efficiency ([S1]). However, scale remains limited versus major global pharma peers; thus execution effectiveness in expanding geographic footprint remains a key determinant.

Growth Drivers

The company identifies multiple vectors for growth including:

- Geographic Expansion: Recent exclusive distribution agreements covering UAE (via Pharmalink), Kuwait, Jordan plus non-exclusive European territories position Cosmos Health towards significant volume scaling of its nutraceutical brands—orders exceeding 500k units expected in 2026 alone from UAE with multimillion-unit targets over five years ([S25]).

- R&D Innovation: The acquisition of Cloudscreen unlocks proprietary drug repurposing opportunities targeting high-demand CNS cancers, hematologic malignancies validated by patent filings and preclinical data ([S6],[S18]). Advanced clinical development programs such as CCX0722 for obesity poised for Phase trials serve as catalysts for broadening commercial product mix.

- Vertical Integration Enhancements: Optimization of manufacturing plants including contract manufacturing services (CMO/CDMO) provides scalable capacity supporting both internal pipeline products and third-party projects enhancing revenue diversification ([S8]).

- Digital Health Platforms: ZipDoctor telehealth services complement product offerings capturing healthcare delivery modernization trends accelerated during the pandemic.

These initiatives collectively aim to strengthen margins by focusing on proprietary higher-margin offerings alongside foundational generic medicines volumes.

Risks and Growth Constraints

Despite promising operational developments, Cosmos Health faces significant risks:

- Regulatory Compliance: Navigating complex pharmaceutical regulations across multiple jurisdictions requires continual investment; non-compliance or delays can materially impact market access or impose costly penalties ([S9],[S28]). Changes to customs, transfer pricing taxation laws also pose exposure affecting profitability ([S12]).

- Pricing Pressure: Wholesale customer consolidation exerts downward pressure on generic drug prices forcing margin compression unless offset by volume or higher-margin products ([S27]).

- Liquidity Constraints: The company holds limited cash ($514k as of March 31, 2026) against current liabilities exceeding $34 million, resulting in tight near-term liquidity despite a current ratio marginally above 1.0—raising concerns over funding availability to support capital-intensive R&D and geographic expansion ([F1]).

- Execution Risk: Scaling manufacturing capabilities while integrating new product launches demands strong operational discipline; failure could delay revenues or increase costs undermining growth outlook.

- Market Concentration: Although no single customer accounts for >10% revenue presently, reliance on a relatively small number of wholesalers entails counterparty risk should contractual dynamics change ([S30]).

What to Watch Next

Upcoming indicators will be critical gauges of execution progress:

- Completion of CCX0722 production scale-up scheduled before launch into human clinical trials anticipated for late 2026 marks a crucial pipeline milestone ([S18]).

- Early commercial order intake fulfillment cycles under recently signed UAE/Kuwait/Jordan distribution contracts will provide tangible validation of demand projections ([S25]).

- Regulatory approvals or clearances tied to oncology repurposed drugs discovered via Cloudscreen indicate maturity of innovation strategy.

- Further updates regarding liquidity management or potential capital raises will be monitored given currently constrained cash balances.

- Management commentary in subsequent quarters around corporate reorganization benefits or cost optimization initiatives may shed light on path toward sustainable operating profitability.[F1]

Financial Profile Summary

As per the latest available financial data ending March 31, 2026 [F1]: Cosmos Health maintains cash reserves just over $514 thousand but carries substantial current liabilities approximating $34 million yielding a current ratio near 1.08 indicating near-break-even short-term liquidity. The last full fiscal year ended December 31, 2025 reflected $65.3 million in revenues but operating income was negative at approximately -$16.7 million driven by substantial R&D spending incentivized by strategic pipeline investments alongside costs associated with expanding global commercial operations [F1].[N3]

Margins remain compressed but improving gross profit trends suggest opportunity if execution successfully scales higher-margin product sales lines and operational efficiencies materialize from ongoing reorganization efforts [N3]

This analysis synthesizes SEC disclosures up to May 20, 2026 without providing investment advice. It aims to contextualize Cosmos Health Inc.'s evolving healthcare platform through operational updates anchored by regulatory filings highlighting its innovation-led growth trajectory balanced against financial challenges inherent to ambitious expansion strategies.

Financial position in context

As of 2026-03-31, companyfacts shows $514,702 in cash and equivalents [F1]. Current assets of approximately $36.9 million and current liabilities of approximately $34.1 million imply a current ratio near 1.08x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments