Cheniere Energy Partners Executes Growth Amid Capital-Intensive LNG Expansion and Steady Cash Flow

A limited partnership anchored by the Sabine Pass LNG Terminal, delivering long-term contracts and disciplined capital allocation in a dynamic energy market.

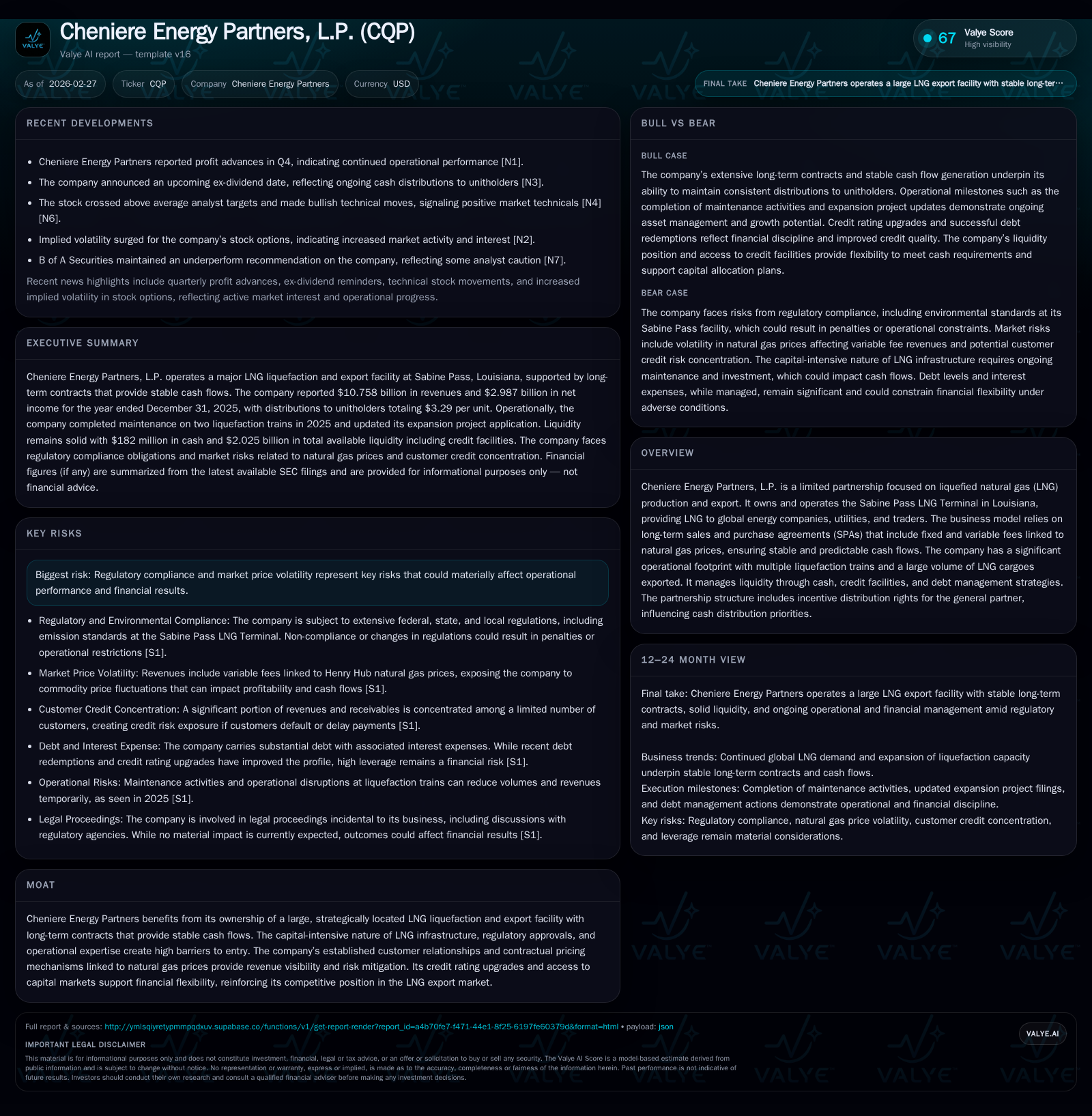

Cheniere Energy Partners, L.P. (CQP) demonstrated strong revenue growth driven by increased LNG sales volumes and pricing linked to long-term SPAs with take-or-pay structures. Despite a complex capital structure with significant debt, the partnership maintains steady operating cash flows and robust free cash flow generation while pursuing disciplined expansion at its strategic Sabine Pass facility. Regulatory compliance and market price risks remain considerations, alongside distribution obligations influenced by incentive distribution rights (IDRs). Growth depends on final investment decisions for liquefaction expansions and capital markets access.

Overview

Cheniere Energy Partners, L.P. (CQP) operates one of the largest liquefied natural gas (LNG) export facilities globally—the Sabine Pass LNG Terminal in Louisiana—which forms the backbone of its business model focused on LNG production and export. The partnership's liquidity and revenue stability are supported by long-term sales and purchase agreements (SPAs), which combine fixed liquefaction fees under take-or-pay contract terms with variable fees linked to natural gas market prices [S14]. Its operational footprint includes multiple liquefaction trains capable of serving global LNG demand.

Historical Performance

Financially, CQP has posted consistent growth in recent years. The latest annual results from FY2025 reveal continued momentum:

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 10.8 | 3.0 | 2.8 | 3.7 | +23.6% | +19.0% |

| 2024 | 8.7 | 2.5 | 3.0 | 3.3 | -9.9% | -41.0% |

| 2023 | 9.7 | 4.3 | 3.1 | 5.0 | -43.8% | +70.3% |

| 2022 | 17.2 | 2.5 | 4.1 | 3.4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($bn) |

|---|---|

| 2025 | 2.6 |

| 2024 | 2.8 |

| 2023 | 2.9 |

| 2022 | 3.7 |

Source: SEC companyfacts cache [F1].

The nearly 24% revenue increase in FY2025 was driven primarily by higher contracted LNG volumes during favorable pricing embedded within SPAs that link part of revenues to natural gas prices [F1], [S14]. Operating income expanded by approximately 13%, reflecting operational leverage despite increased maintenance and site optimization costs signaled by a rise in capital expenditures (+29%) directed mainly at facility improvements rather than new greenfield developments [F1]. Net income increased proportionally.

Operating cash flows decreased slightly (-6.7%) compared to the prior year due to timing differences in cash collections related to cargo sales and working capital dynamics but remained robust at $2.77 billion [F1], [S19]. Free cash flow after capex remains strong near $2.57 billion, enabling sustained distributions to unitholders and debt servicing.

Business Model & Contractual Framework

CQP’s business model relies heavily on long-term SPAs underpinning stable cash flows through take-or-pay provisions combined with fees indexed partly to natural gas prices, providing both downside protection and upside participation in commodity markets [S14]. As of December 31, 2025, the partnership had substantial future revenues under these contracts extending beyond the next decade with significant fixed fees plus variable components, demonstrating extended earnings visibility.

The asset base centers on Sabine Pass, benefiting from established pipeline connectivity from U.S. natural gas supply basins and proximity to Gulf shipping lanes—conditions that create barriers against new entrants given regulatory hurdles and capital intensity inherent in LNG infrastructure development.

Customer exposure is diversified among ten or more counterparties each holding contracts exceeding ten years; no single customer accounts for over one-quarter of revenues or receivables on a trailing basis [S7]. This reduces credit risk concentration but requires ongoing monitoring given energy sector cyclicality.

Capital Structure & Liquidity Position

At December 31, 2025, CQP carried approximately $14.6 billion in senior notes issued across multiple maturity buckets spanning from near term (2026–2030) through longer-dated instruments maturing between 2031–2037 [S4], [S16]. These bonds bear weighted average coupon rates near mid-single digits (~4.73%), reflecting secured/unsecured issuances across the broader Cheniere capital structure.

Credit facilities provide additional liquidity buffers totaling approximately $2 billion available commitments as of year-end; no borrowings were outstanding under these revolvers at that time simplifying short-term liquidity management [S4], [S16]. Debt agreements impose covenants limiting distributions until reserves for debt service are established and coverage ratios met—a prudent framework ensuring balance sheet discipline despite distribution obligations [S15], [S21].

In February 2026 filings, CQP confirmed compliance with all financial covenants governing indebtedness signaling sustainable financial footing amid active redemption activity reducing near-term maturity exposure [S6], [N1].

Distribution Policy & Incentive Distribution Rights (IDRs)

CQP’s partnership agreement mandates quarterly distribution of available cash within guidelines defined by operating surplus less reserves set by the general partner [S1], consistent with typical midstream master limited partnership structures.

The general partner retains a two percent ownership stake plus incentive distribution rights that escalate their share of excess cash distributed beyond initial tiers: starting at two percent participation increasing progressively up to fifty percent once distributions exceed specified thresholds above $0.638 per unit quarterly—which recently occurred given Q4/25 per-unit distributions approaching $0.83—indicating a meaningful allocation shift towards the general partner as total distributions grow alongside cash flow expansion [S1], [S24], [N3].

This alignment incentivizes growth projects but requires monitoring unitholder yield dilution trends when IDR payments accelerate.

Growth Prospects & Expansion Projects

Looking ahead, CQP holds substantial land adjacent to Sabine Pass providing optionality for brownfield capacity expansions leveraging existing infrastructure advantages such as shared pipelines and marine logistics support—critical factors minimizing incremental costs relative to greenfield alternatives [S14].

The SPL Expansion Project envisions phased development encompassing three additional liquefaction trains targeting an aggregate ~20 million tonnes per annum (mtpa) capacity inclusive of debottlenecking enhancements approved conceptually via FERC applications updated mid-2025 reflecting regulatory progress critical before final investment decision (FID) could occur [S14].

Commercial execution depends on securing acceptable contract structures with creditworthy counterparties alongside financing arrangements adequate for large-scale capex outlays—typical uncertainties within LNG infrastructure projects facing evolving global energy demand amid decarbonization pressures.

Risks & Regulatory Environment

Key risks include:

- Regulatory compliance: Subsidiaries resolved formaldehyde emission standard non-compliance flagged by Louisiana Department of Environmental Quality (LDEQ), with EPA confirming turbine compliance during testing periods through late-2025 without material penalties anticipated—ongoing environmental scrutiny remains relevant for fossil fuel operations oversight [S1],

- Market price volatility: Variable fee components tied directly to natural gas benchmarks expose earnings fluctuations dependent on external commodity cycles,

- Counterparty credit risk: Despite long contract terms backed by guarantees or collateral security mechanisms, defaults or deterioration remain inherent risks,

- Legal proceedings: No material litigation currently threatens financial health though ordinary course matters exist consistent with disclosures [S20].

Monitoring & Forward Indicators

Key milestones include:

- Progress toward FID on SPL Expansion Project phases,

- Contract additions or amendments expanding SPA backlog relevant for volume growth projections,

- Updates on regulatory compliance relating to environmental metrics,

- Changes in capital allocation priorities influenced by debt refinancing or distribution policy revisions,

- Variability in quarterly distributable cash flow reflective of commodity price swings or operational efficiencies.

Recent media coverage highlights robust Q4/25 operating results consistent with annual trends suggesting ongoing execution discipline amidst sector volatility ([N1]). Implied volatility spikes observed in stock options indicate market uncertainty around near-term catalysts ([N2]).

Conclusion

Cheniere Energy Partners balances growth ambitions anchored by Sabine Pass’ established LNG export foundation against a capital-intensive cost structure heavily influenced by contracted long-dated customer commitments delivering predictable cash flows enhanced via savvy stewardship of incentive rights schemes for its general partner entity.

Its performance trajectory evidences resilient revenue expansion coupled with high-quality net income margins moderated by regulatory complexities and commodity-linked variability impacting distributable funds flow cycles.

Continued advancement through permitting and financing stages for liquefaction capacity expansions together with prudent liquidity management will be pivotal for sustaining value creation pathways within this strategically pivotal segment of global energy trade.

Disclaimer: This analysis is based solely on information provided from company filings, news reports cited herein, and known industry context as of February 27, 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments