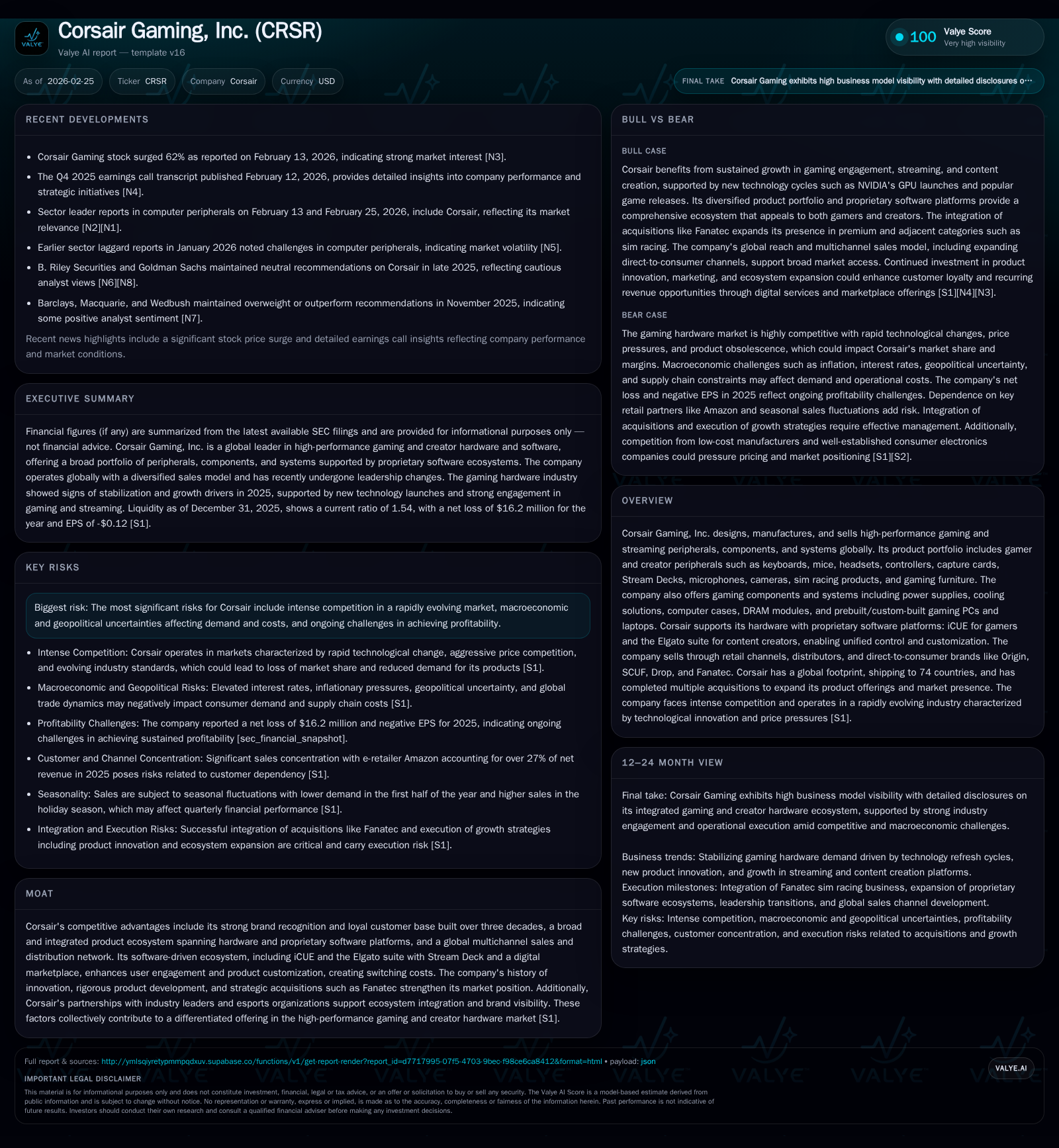

Corsair Gaming’s Turnaround and Expansion Highlights Margin Leverage and Ecosystem Strategy

Corsair Gaming’s 2025 financials mark a significant operating profit recovery amid strategic investments in software platforms and product ecosystem expansion.

Corsair Gaming has transitioned from years of operating losses to a positive operating income in FY2025, driven by robust demand for gaming peripherals and components fueled by technology refresh cycles. The company’s strategic focus on expanding its direct-to-consumer business, integrating proprietary software ecosystems iCUE and Elgato, and selectively acquiring premium brands like Fanatec is central to its growth outlook. Despite posting a net loss due to non-operating factors, strong operating cash flow and capital discipline underscore improving financial health. Market dynamics—including stiff competition, macroeconomic headwinds, and evolving consumer preferences—remain key factors to monitor.

Company Overview

Corsair Gaming, Inc. is a prominent provider of high-performance gaming and digital creator hardware globally. With over three decades in the market, Corsair offers an extensive portfolio including gaming keyboards, mice, headsets, streaming capture cards (Elgato), computer components such as power supplies (PSUs), cooling solutions, DRAM modules, prebuilt/custom-built PCs and laptops, AI workstations, sim racing hardware via Fanatec acquisition, plus high-end peripherals like Stream Decks.

Crucial to Corsair’s product appeal is its dual-software ecosystem: iCUE caters primarily to gamer PC builders enabling unified system monitoring and RGB customization; the Elgato software suite supports creators through workflow automation on Stream Decks and capture tools. These platforms create user lock-in by integrating multiple hardware pieces across gaming and streaming setups [S1][S4][S8][S16].

Historical Performance

From 2022 through 2025, Corsair’s operating income demonstrates notable volatility with large losses in 2022 (-$54.8M) and 2024 (-$49.95M), but a material swing back to a positive $2.08M operating profit in FY2025 [F1]. Net income remains negative across these years but shows marked improvement from -$54.4M (2022) to -$16.2M (2025). Operating cash flows have stayed robust despite earnings volatility: $66.4M (2022), peaking at $89.2M (2023), dipping moderately thereafter but recovering to $50.1M by year-end 2025.

Capital expenditure spending fluctuated significantly with a major spend of $26.3M in 2022 dropping mid-cycle before rising again to $15.4M in 2025 alongside operational scaling [F1]. The firm maintains solid equity capital above $600M during this period.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -16 | 50 | 2 | 15 | +81.0% |

| 2024 | -85 | 36 | -50 | 10 | -3188.8% |

| 2023 | -3 | 89 | 10 | 13 | +95.2% |

| 2022 | -54 | 66 | -55 | 26 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 35 | -2.6 |

| 2024 | 26 | -14.1 |

| 2023 | 76 | -0.4 |

| 2022 | 40 | -8.7 |

Source: SEC companyfacts cache [F1].

Note: Revenue data is not available from provided tags; approximate ROE for FY25 is -2.6%, calculated as net loss over equity [F1]. No recent share repurchase or dividend activity reported since FY2019.

Industry Context

The global gaming industry continues steady growth propelled by broadening participation across PC, console (e.g., Nintendo Switch 2 launch), mobile, and cloud platforms [S24]. High-profile game releases during holiday seasons also drive seasonal spikes in hardware demand which traditionally peak in Q4 [S13]. Technology refresh cycles notably the introduction of NVIDIA's advanced AI-enabled GPUs spurred upgrades among enthusiasts seeking cutting-edge performance and graphics [S25].

The creator economy remains vibrant with streaming platforms like Twitch (averaging 2.5 million concurrent viewers) and YouTube (2+ billion monthly users) increasing demand for professional-grade streaming equipment reinforcing Corsair's peripheral sales [S24].

Business Model & Strategic Drivers

Corsair operates two main segments:

- Gamer & Creator Peripherals: Including keyboards, mice, headsets, Stream Decks for content control automation, Facecam cameras; plus sim racing gear post-Fanatec acquisition.

- Gaming Components & Systems: High-performance power supplies (PSUs), cooling solutions including liquid cooling favored by overclockers due to superior thermal management efficiency (a key component for maximizing CPU/GPU longevity), computer cases optimized for airflow & aesthetics; DRAM modules engineered for high-frequency stability; custom-built desktops/laptops tailored for gamers/AI workloads.

Distribution channels combine global retail partners such as Amazon (~27% revenue share), Best Buy along with direct-to-consumer websites encompassing Corsair's owned brands Origin PC (custom systems), SCUF (controllers), Drop (keyboards & audio), and Fanatec (racing wheels). Direct sales enhance margins while providing valuable customer data allowing rapid iteration of product development based on user feedback [S4][S7][S8].

Key growth strategies include:

- Scaling direct channels alongside retail,

- Expanding proprietary software platforms iCUE & Elgato Marketplace,

- Selective acquisitions targeting adjacent premium categories,

- Strengthening esports partnerships for brand visibility,

- Continuing geographic expansion particularly within Asia Pacific where penetration remains limited relative to Western markets.

Software integrations such as controlling system cooling profiles or executing streaming commands seamlessly across devices contribute substantial switching costs — a competitive moat increasingly important as hardware commoditization intensifies [S6][S15][S21].

Competitive Landscape & Differentiation

The market exhibits aggressive competition not only from specialist gaming hardware companies but also large consumer electronics firms with deeper pockets [S6][S17]. Competitors range from boutique keyboard makers through large-scale manufacturers offering low-cost alternatives primarily sourced from Asia with minimal marketing spend targeting price-conscious buyers.

Corsair’s competitive edge hinges on:

- Leading brand recognition developed over more than three decades,

- Integrated ecosystem unifying hardware+software,

- Innovation-driven product development pipeline tailoring user experience,

- Comprehensive sponsorships within esports & streaming communities fostering loyal brand ambassadors,

- Scale benefits including centralized procurement reducing cost basis particularly notable after full Fanatec integration enabling margin support in sim racing segment.

Recent Developments & Leadership

In July 2025 Thi La assumed CEO responsibilities transitioning from President/COO role while Gordon Mattingly was appointed CFO end of that year signaling renewed leadership focus amid turnaround efforts [N1][S14].

The company opened its first immersive retail experience store in California during 2025 to boost direct customer engagement benefiting both sales conversion rates and brand loyalty development [S7].

Demand trends gained momentum with improved release cadence of marquee games after delays experienced in preceding years heightening hardware refresh interest among consumers [S24]. The debut of Nintendo Switch 2 sparked accessory sales growth especially within Elgato capture devices supporting creator workflows tied to new console content streaming.

Financial Health & Capital Allocation

Corsair’s liquidity profile is stable highlighted by a current ratio near 1.54 reflecting effective working capital management with current assets comfortably exceeding liabilities [F1]. The company secured a renewed credit agreement mid-2025 totaling $225 million featuring revolving credit plus term loans deployed for operational flexibility at favorable terms [S18][S20].

Operating cash flow generation remains strong ($50 million+ FY25) despite net losses attributable partly to financing/non-cash charges indicative of ongoing restructuring or amortization expenses related to acquisitions [F1]. Capital expenditures increased notably year-over-year signaling ramped investment into future product development capacity.

No dividends or share repurchases have been recorded since FY2019 per available data indicating capital preservation during the turnaround phase [F1]. Approximate ROE remains negative but narrowed significantly compared with prior years (-2.6% FY25 versus deeper negatives earlier).

Near-Term Outlook & Risks

While explicit forward guidance is not provided currently publicly available documents emphasize the focus on continued margin improvement through operational discipline paired with scaling higher-margin products including software-driven solutions [N1][S8].

Key factors to monitor include:

- Industry release cycles influencing seasonal demand,

- Further expansion of digital services/platforms potentially unlocking recurring revenue streams,

- Macro uncertainties including inflationary pressures impacting component costs or consumer spend elasticity,

- Intensifying price competition especially from well-capitalized incumbents or low-cost entrants.

Additionally, Corsair faces risks common across hardware manufacturers such as supply chain disruptions given reliance on third-party Asian manufacturing facilities as well as geopolitical tensions influencing trade policies that could affect logistics costs or component availability [S11][S19][S22][S23]. Maintaining innovation cadence without overextending R&D spend will remain critical balancing act.

Conclusion

Corsair Gaming has entered an inflection point reflected by improved operating profitability complemented by strategic investments boosting ecosystem stickiness via proprietary software controls paired with diversified premium peripheral offerings such as sim racing post-Fanatec acquisition. This pivot towards integrating hardware craftsmanship with software platforms aligns well with evolving demands from both competitive gamers seeking performance edge and content creators requiring seamless production workflows. Though net losses persist amidst industry pressures, strong cash flow fundamentals alongside prudent capital management provide financial resilience navigating market uncertainties. Investors should keep an eye on product pipeline execution pace alongside macro demand trends shaping the broader gaming hardware landscape going forward.

Disclaimer: This analysis provides an overview based solely on publicly available information up until February 25, 2026, including SEC filings and news transcripts cited herein; it does not constitute investment advice or recommendations to buy or sell securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments