Citius Oncology's LYMPHIR Launch and Commercialization Challenged by Funding and Market Dynamics

Citius Oncology progresses with its FDA-approved LYMPHIR therapy for CTCL but faces liquidity pressures that could constrain its commercial ramp.

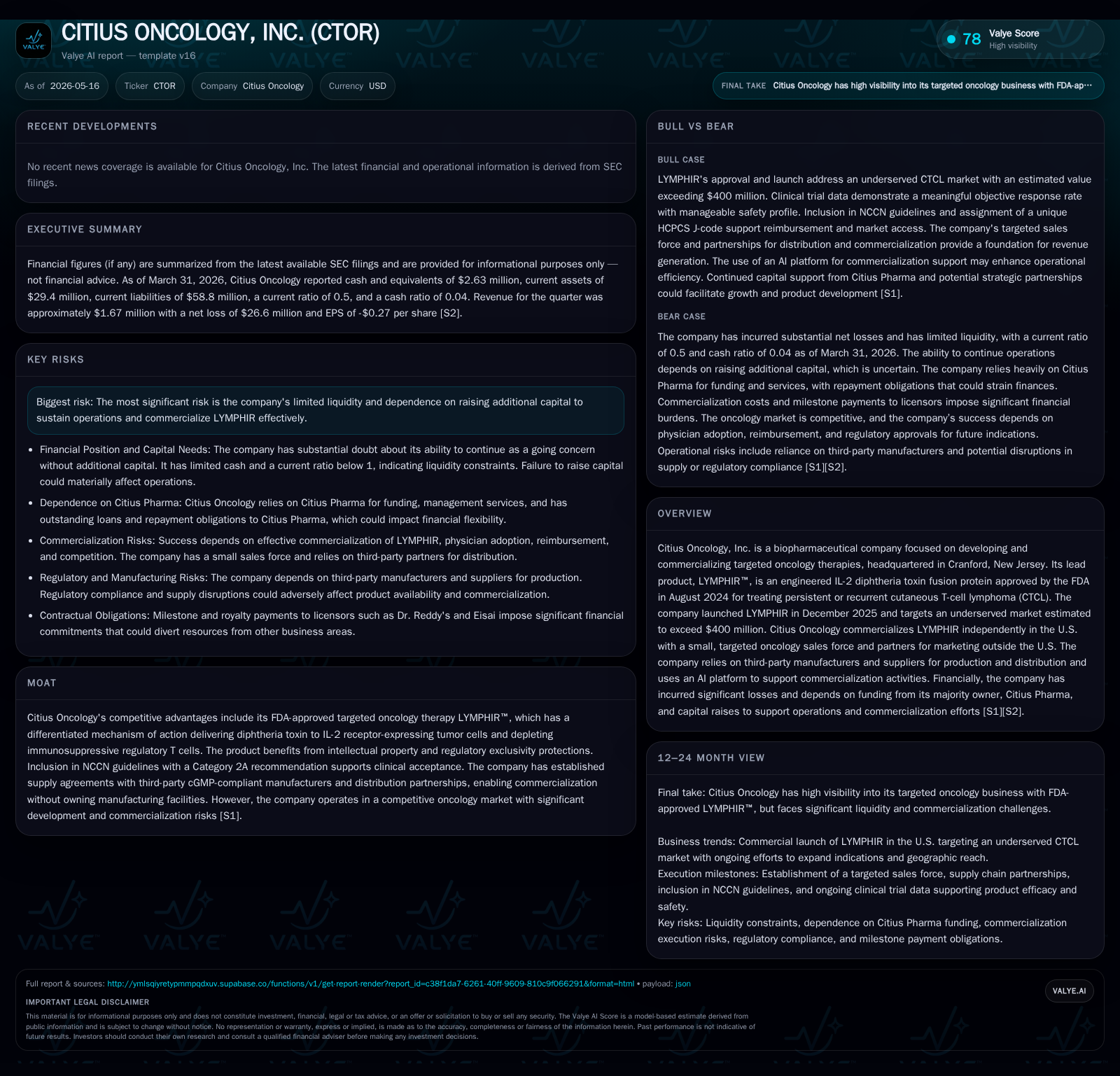

In Q1 2026, Citius Oncology reported initial revenues of approximately $1.67 million from LYMPHIR, its sole FDA-approved oncology therapeutic launched in December 2025. Despite this commercial progress targeting a niche cutaneous T-cell lymphoma market valued over $400 million, the company continues to operate at a substantial loss and maintains a precarious liquidity position. Their business model leverages third-party manufacturing and a focused U.S. sales team supported by AI-driven commercialization tools, yet capital constraints pose execution risks. Sector dynamics favor LYMPHIR’s unique mechanism and NCCN guideline inclusion, but growth hinges on successful market adoption, reimbursement, and further capital infusion.

Recent Quarterly Operating Update and Its Implications

Citius Oncology filed its Q1 2026 Form 10-Q on May 15, 2026 [S2], supplemented by an 8-K earnings release the same day [S3]. The quarter represents the company’s first full quarter following LYMPHIR’s U.S. launch in late December 2025. Revenue recognition from commercial sales reached approximately $1.67 million [F1], marking initial validation of the product's commercial traction within the persistent or recurrent cutaneous T-cell lymphoma (CTCL) segment. While the revenue figure is modest relative to the total estimated addressable market exceeding $400 million [S1], it signals a nascent uptake stage.

Despite this top-line progress, Citius Oncology continues to report significant operating losses consistent with pre-commercial patterns and intensified investment associated with scaling its dedicated sales force and marketing platform [S2]. The company confirms no material updates to risk factors beyond those detailed in its prior annual filing [S2], signaling persistent funding concerns remain paramount.

Meanwhile, operating expenses reflect continued buildup of specialized marketing resources tailored to key oncology referral centers across strategic U.S. geographies, complemented by deployment of an AI-driven platform designed to optimize physician engagement and prescribing behavior [S1]. This dual approach aims to forge durable demand pathways while maintaining lean operational efficiency appropriate for a small biopharma commercialization.

From a near-term outlook perspective, sustaining the early commercial momentum amid constrained liquidity poses critical execution stakes given their cash position of roughly $2.63 million as of March 31, 2026 [F1]. This resource base contrasts sharply with current liabilities nearing $58.8 million translating into a challenging working capital dynamic (current ratio ~0.5) [F1].

Business Model Centered on LYMPHIR and Product Quality

Citius’ business model is extraordinarily focused: it derives all current revenues solely from LYMPHIR™, an engineered IL-2-diphtheria toxin fusion protein designed to target IL-2 receptor-expressing tumor cells selectively while depleting immunosuppressive regulatory T cells [S1]. This unique mechanism differentiates LYMPHIR in the CTCL treatment landscape—a rare subtype within non-Hodgkin lymphomas—to pursue an underserved patient population.

The FDA approval in August 2024 granted regulatory exclusivity that shields competition for a defined period while inclusion in NCCN guidelines as Category 2A endorses clinical acceptance among oncologists [S1]. Citius’ commercialization strategy eschews owning manufacturing infrastructure; instead, it contracts with third-party cGMP-compliant manufacturers ensuring scalable supply chain flexibility without capex intensification [S1].

On the sales front, rather than broad-based pharmaceutical reps, Citius employs a small cadre of specialized oncology sales professionals tasked primarily with outreach to major cancer centers where persistent or recurrent CTCL treatment decisions concentrate [S1]. This targeted approach aligns with market size realities and conserves resource allocation.

Additionally, Citius leverages advanced AI capabilities to supplement human interactions, aiming to optimize messaging frequency, tailor materials dynamically based on prescriber behavior data, and accelerate provider adoption trends. Outside the U.S., distribution partnerships extend reach without necessitating direct global infrastructure—a typical biopharma approach balancing control with scale economies [S1].

Intellectual property protections around LYMPHIR’s composition and methods secure competitive moat conditions alongside regulatory exclusivities afforded by FDA approval pathways [S1]. Yet reliance on a single asset defines both strategic clarity and inherent portfolio risk.

Industry Context and Competitive Dynamics in Targeted Oncology

Within oncology therapeutics, CTCL remains a relatively small yet clinically challenging indication historically underserved by effective treatments; estimates value the U.S.-only addressable market for such therapies exceeding $400 million annually [S1]. Biopharmaceutical development trends prioritize targeted biologics with differentiated mechanisms; LYMPHIR fits squarely into this paradigm via receptor-directed cytotoxicity combined with immune modulation.

Nonetheless, the oncology biopharma sector is intensely competitive. Several entities develop fusion proteins or immunotherapies addressing lymphomas albeit varying by molecular profile or indication scope. Pricing power for novel agents often encounters payor pushback demanding favorable cost-effectiveness outcomes; here reimbursement remains under surveillance pending further volume accrual post-launch as reflected by limited early revenue figures post-Dec-2025 rollout [S1].

Regulatory environments differ markedly outside the United States presenting potential barriers or delays—hence Citius’ partnership approach internationally mitigates these complexities at outsourcing expense tradeoffs. Supply chains for biologic drug substances rely heavily on contract manufacturers capable of strict quality adherence (cGMP compliance), making continued partner performance crucial given lack of internal assembly capacity [S1].

Commercialization risk cycles are prolonged relative to other pharma sectors due to complex clinical decision-making processes governing oncology prescribing combined with intricate reimbursement frameworks entwined with evolving U.S. healthcare reform trajectories [S1].

Growth Drivers Shaping Adoption and Market Penetration

Expansion of LYMPHIR’s commercial footprint depends heavily on several discreet catalysts aligned with physician adoption dynamics and broader market penetration metrics. First, focused sales efforts targeting major cancer centers represent primary levers since prescribers at these institutions determine early-use patterns influencing wider diffusion across regional providers [S1][F1].

Inclusion in NCCN guidelines as Category 2A supports payer recognition which facilitates reimbursement—a critical bottleneck for novel oncology therapies requiring prior authorization or formulary placement negotiation [S1]. The AI-augmented platform employed aims to amplify message personalization enabling cross-channel engagement efficiencies potentially improving conversion rates versus conventional sales models.

Additional growth pathways may stem from clinical pipeline developments including ongoing investigator-sponsored trials evaluating LYMPHIR’s activity in combination regimens for other tumor types such as gynecologic cancers and diffuse large B cell lymphoma (DLBCL) documented through positive Phase 1 topline results announced in early 2026 [S11][S12]. Successful advancement here could enlarge indication breadth thereby extending revenue avenues beyond primary CTCL usage.

International expansion via shipment initiation through European distribution partners marks incremental territorial growth likely contributing royalties though at longer lead times given foreign regulatory approvals required [S16].

Overall organic growth hinges upon measurable increases in prescription counts within existing channel geographies coupled with successful reimbursement workflows; however upfront operating losses suggest that positive cash flow remains distant until substantial market penetration accrues [F1][S2].

Risks and Limitations: Capital Needs and Execution Challenges

Despite clear scientific differentiation underpinning LYMPHIR’s commercial value proposition, Citius Oncology confronts material financial constraints that threaten operational continuity absent further funding events [S1][S2][F1]. The company continues to disclose 'substantial doubt' about its ability to sustain operations beyond March 2026 barring successful capital raises or revenue scaling since accumulated deficits exceed $64 million as reflected through prior filings and current cash flows remain negative [S1][F1].

As of March 31, 2026, cash & equivalents stood at just over $2.63 million backed by total debt recorded previously at approximately $1.72 million creating limited liquidity buffers amid current liabilities surpassing $58 million—yielding a constrained current ratio near 0.5 denoting working capital stress peculiar for an operating business yet typical for small biopharma still ramping [F1].

Recent financing arrangements announced May 2026 provide access to up to $25 million term loans disbursed across three tranches contingent upon net revenue milestones achievement starting immediately—with above-market interest rates north of prime plus fees—and secured pledges including intellectual property liens underlying credit agreements highlight enhanced financing costs reflecting elevated risk perceptions by lenders [S23][S24].

Equity dilution risk looms given voluntary conversion features embedded in notes held by majority owner Citius Pharma increasing potential share count compression effects influencing shareholder equity dynamics though preserving runway if managed prudently [S27].

Additional risks stem from marketplace volatility illustrated by Nasdaq bid price non-compliance notices requiring remedial measures within prescribed deadlines or facing delisting risks—factors that impose reputational pressure impacting investor confidence notwithstanding operational advances during commercialization phase[S17][S28].

Execution challenges also arise from single-product concentration exposing revenues disproportionately to uptake success or competitive encroachment alongside evolving healthcare payment reforms which may introduce unpredictable reimbursement restrictions curtailing demand elasticity even post-guideline endorsement[S1].

Key Upcoming Developments and Milestones to Monitor

Several near-term focal points will offer signals regarding sustainability of the commercialization journey for LYMPHIR:

- Subsequent quarterly earnings releases following Q1 FY26 results expected later in calendar year will provide updated revenue progression insights highlighting whether initial ~$1.67M run rate accelerates meaningfully beyond launch base[S2][S3]

- Achieving scheduled net revenue milestones tied to tranche releases under recent Loan Agreement launching May-July onwards will test commercial execution effectiveness directly impacting available capital capacity[S23]

- Any new regulatory submissions or approvals aiming at label expansions into additional oncology indications would constitute pivotal growth inflection events[S11][S12]

- Updates regarding AI-based platform integration success metrics or partnership expansions overseas may indicate scalability enhancements supporting broader global reach[S16]

- Resolution status around Nasdaq bid price compliance deadlines October 2026 is critical from investor relations standpoint though does not affect trading immediately[S17][S28]

- Additional capital raise initiatives or strategic corporate transactions announced would be essential indicators confirming financial runway stability necessary amid ongoing losses[S24] These milestones collectively shape whether commercial promise converts into sustainable profitability trajectory.

Latest Financial Snapshot: Liquidity and Capital Structure

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $3mm | |

| 2026-03-31 | ||

| Current assets | $29mm | |

| 2026-03-31 | ||

| Current liabilities | $59mm | |

| 2026-03-31 | ||

| Current ratio | 0.5x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

*Latest debt figure differs by vintage date but reflects only known disclosure tiers absent recent amendments explicitly updating totals.[F1]

The snapshot presents a troubling liquidity profile as short-term obligations substantially exceed readily available assets — underscoring acute working capital pressures characteristic of early-stage biopharma commercialization phases carrying high burn rates associated with staffing costs, supply commitments to contract manufacturers flagged in previous disclosures totaling tens of millions in contractual obligations[S18][F1]. Loan facilities signed earlier this year inject much-needed capital albeit accompanied by elevated interest expense burdens normalizing higher-risk credit terms.[S23][S24]

In aggregate these financial contours reaffirm continuing dependence on external capital sources while gradual revenue improvements are unlikely alone sufficient near-term solvency enhancers.

Disclaimer: This analysis is based solely on publicly available SEC filings up to May 16th, 2026 alongside validated numeric data from company facts aggregations referenced herein. It does not constitute investment advice or recommendations but strives only to synthesize operational context relevant for industry understanding.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments