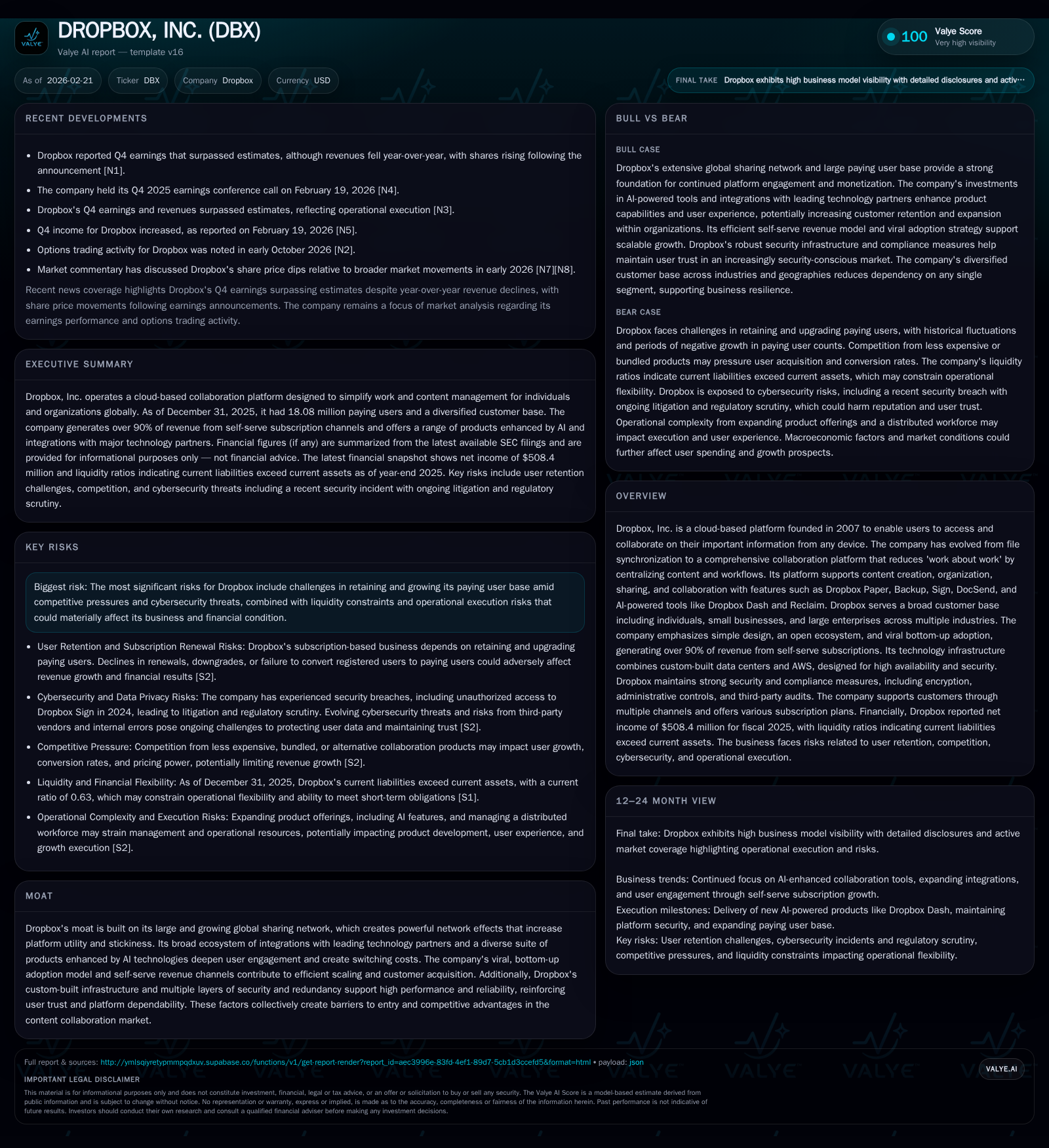

Dropbox’s Transition to Integrated Collaboration Fuels Platform Value Amid Market Pressures

Dropbox evolves from a file-sync pioneer into a collaboration powerhouse, balancing growth challenges with AI integration and capital returns.

Founded as a file synchronization tool in 2007, Dropbox has significantly broadened its platform to offer comprehensive content collaboration reinforced by AI-powered features. Despite recent headwinds signaled by decelerating revenue growth and user retention pressures, the company has leveraged operating leverage to drive profitability gains. Its capital allocation strategy remains heavily buyback-focused amid liquidity constraints and negative equity. Key risks revolve around competitive dynamics, cybersecurity, and the complexities of scaling innovations within a virtual-first workforce model. Monitoring product adoption rates, enterprise penetration beyond bottom-up users, and margin developments will be critical to assessing Dropbox’s trajectory.

Evolution from File Sync to Collaborative Platform: Past Growth Drivers

Dropbox began as a straightforward file synchronization service but has evolved over nearly two decades into an integrated content collaboration platform. This transition is underscored by expanding product functionality—encompassing document creation (Dropbox Paper), backup solutions, e-signatures (Dropbox Sign), secure document sharing (DocSend), and increasingly AI-enhanced tools like Dash and Reclaim [S4][S5]. As of December 31, 2025, Dropbox reported approximately 18.08 million paying users globally alongside roughly 575,000 business teams subscribing to its Business plans [S4].

The company's business model benefits from ‘viral bottom-up adoption,’ where individual users initiate platform usage that subsequently proliferates across organizations organically. Over 90% of Dropbox’s revenue stems from self-serve subscriptions purchased via app or web interfaces—a channel that facilitates efficient scaling with comparatively low acquisition expense [S4][S10].

Examining financial indicators reveals that operating income accelerated notably in recent years. Operating income rose from $181 million in FY2022 to nearly $689 million by FY2025—a compound annual increase supported by expanding paid user bases and product depth despite some revenue headwinds (latest revenue data available is for FY2018) [F1]. This reflects growing quality of earnings derived not merely from volume but also higher-margin subscription tiers and enhanced monetization of new platform features.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 508 | 952 | 689 | 21 | +12.4% |

| 2024 | 452 | 894 | 486 | 23 | -0.3% |

| 2023 | 454 | 784 | 539 | 24 | -18.0% |

| 2022 | 553 | 797 | 181 | 34 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 1714 | 931 | -28.3 |

| 2024 | 1242 | 872 | -60.1 |

| 2023 | 540 | 759 | -273.6 |

| 2022 | 795 | 764 | -178.8 |

Source: SEC companyfacts cache [F1].

Note: Revenue data more recent than FY2018 is not available in provided tags; long-term trend inferred from qualitative disclosures.[F1]

The operating leverage exhibited suggests that investments in infrastructure (including hybrid data center management—custom-built resources combined with AWS cloud services) have been optimized to support growth while controlling costs—a critical factor given pricing pressures and intensifying competition [S4][S10].

Product Innovation and AI Features As Catalysts for Future Expansion

In recent years, Dropbox has intensified focus on embedding AI capabilities to tackle what the company terms "work about work"—the inefficiencies arising from content search delays, application switching, and workflow management overheads [S4][S5]. Products like Dropbox Dash aim to serve as an AI-powered command center linking disparate content sources across the platform ecosystem.

This move aligns with broader industry trends where SaaS providers leverage machine learning techniques for intelligent search and predictive organization. The strategic blend of proprietary development coupled with partnerships—for instance with Microsoft Teams, Slack (Salesforce), Google Workspace—constitutes synergistic ecosystem integrations enhancing user experience and stickiness [S5][S11].

However, the return on investment timeline for AI initiatives is uncertain. Explicit risk disclosures emphasize potentially protracted or delayed benefits of these advanced features along with operational strain arising from added complexity [S1][S7]. Notably, the balance between innovation breadth and maintaining intuitive user interfaces remains delicate; overly complex product configurations could dampen user satisfaction.

User Retention Dynamics and Revenue Model Under Pressure

Dropbox faces significant challenges tied to its subscription-reliant revenue mechanics. While viral bottom-up user adoption fuels initial penetration, maintaining paying user relationships mandates smooth renewal cycles and continued perceived value enhancements [S2]. The company openly states that renewal rates fluctuate substantially due to competition from lower-priced or bundled alternatives, changing customer requirements, macroeconomic impacts on budgets, and occasional dissatisfaction with product features or support levels.

Self-serve model advantages also introduce exposure: low friction signup can equally translate into low commitment levels for renewals or upgrades. There is geographic and cohort variability affecting user behavior—with enterprise IT-led adoption often lagging behind grassroots individual uptake—which could cap near-term expansion velocity if not adequately managed through targeted sales strategies beyond organic growth approaches [S2][S6].

Financial Trajectory: Profitability Gains Amidst Revenue Variability

The latest available data indicates robust profitability improvement: operating income increased by an impressive +41.7% in FY2025 versus FY2024 despite reported year-over-year revenue declines for certain recent quarters ([N1],[N2]). Net income also grew by +12.4%, supported in part by disciplined cost control measures including reduced capital expenditures (-6.7% YoY). Operating cash flow rose +6.5%, yielding an approximate free cash flow of around $931 million after capex expenditures [F1].

Yet underlying these gains is a structural anomaly: Dropbox’s stockholders' equity remains negative at -$1.8 billion as of end-2025 due primarily to amassed share repurchase programs exceeding retained earnings accrued since inception [F1][S9]. This negative equity position contrasts with strong net income figures but reflects financial engineering focused on returning capital rather than balance sheet accumulation.

Maintaining sustainable profitability amid necessary investments in platform innovation—including AI enhancement—and market-driven pricing pressures will be pivotal going forward.

Capital Allocation Strategy: Aggressive Buybacks and Cash Positioning

Dropbox operates a highly return-focused capital allocation strategy dominated by substantial share repurchases: $1.71 billion repurchased during FY2025 alone marks an acceleration versus $1.24 billion in FY2024 and earlier amounts [F1][S14]. These repurchases target boosting shareholder value amidst limited dividend payouts—the company explicitly does not pay dividends nor intends to do so in the foreseeable future due to investment priorities and loan covenants restricting distributions [S14][S12]. Dividends paid data is not available in provided tags.[F1]

Operating cash flows ($952 million in FY2025) sufficiently fund these buybacks alongside moderate capex ($21 million), preserving liquidity expressed as ~$891 million cash & equivalents at year-end—though current liabilities noticeably exceed current assets leading to a current ratio of approximately 0.63 [F1].

This approach underscores confidence in business fundamentals but involves tradeoffs: intensified stock buybacks inflate share price volatility potential while reducing reserves available for opportunistic acquisitions or deeper infrastructure investments required for growth acceleration.

Navigating Operational Risks and Industry Competition

Dropbox confronts several operational hurdles accentuated by its virtual-first workforce model designed for global distributed operations—a structure prone to complexity in coordination impacting timely delivery of products that meet evolving client expectations [S1][S7].

Further complicating execution are cybersecurity exposures inherent in cloud content platforms—with Dropbox investing heavily in encryption layers, network protections, multi-redundant data architectures yet facing non-negligible incident risks affecting customer trust [S7][S16].

Competitive pressures remain acute with players ranging from large tech incumbents bundling storage/collaboration suites (Microsoft OneDrive/Teams, Google Drive/Workspace) to specialized SaaS vendors targeting narrow niches such as e-signature or AI-driven document search (Adobe Sign, DocuSign; Glean, Notion) challenging pricing power and compelling continuous innovation [S6][S11]. Intellectual property litigation represents another source of expense potential despite favorable rulings in recent patent disputes [S20][S18].

What to Watch: Product Adoption, Enterprise Expansion, and Margin Trends

Absent explicit forward guidance beyond qualitative outlines at latest quarterly calls ([N3]), key metrics warrant close observation:

- Uptake rates for AI-enabled premium features like Dropbox Dash/Reclaim impacting average revenue per user,

- Penetration deepening among enterprise customers beyond organic bottom-up expansion,

- Renewal rate stability amid macroeconomic pressures,

- Quarterly oscillations in revenue juxtaposed against ongoing margins reflecting operating leverage effects,

- Impact of Virtual First operational agility on delivery timelines.

Continued success will hinge on execution precision bridging technology innovation with market realities while sustaining efficient scaling through self-service subscription dynamics.

Disclaimer: This analysis is based solely on provided regulatory filings, news reports, and structured financial data without any investment recommendations or forecasts beyond documented disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments