Rayonier Inc. Shows Resilience with Sustainable Forestry and Rising Net Income

Despite a sharp revenue decline, Rayonier’s earnings and cash flows underscore strength driven by sustainable timber management and evolving land use strategies.

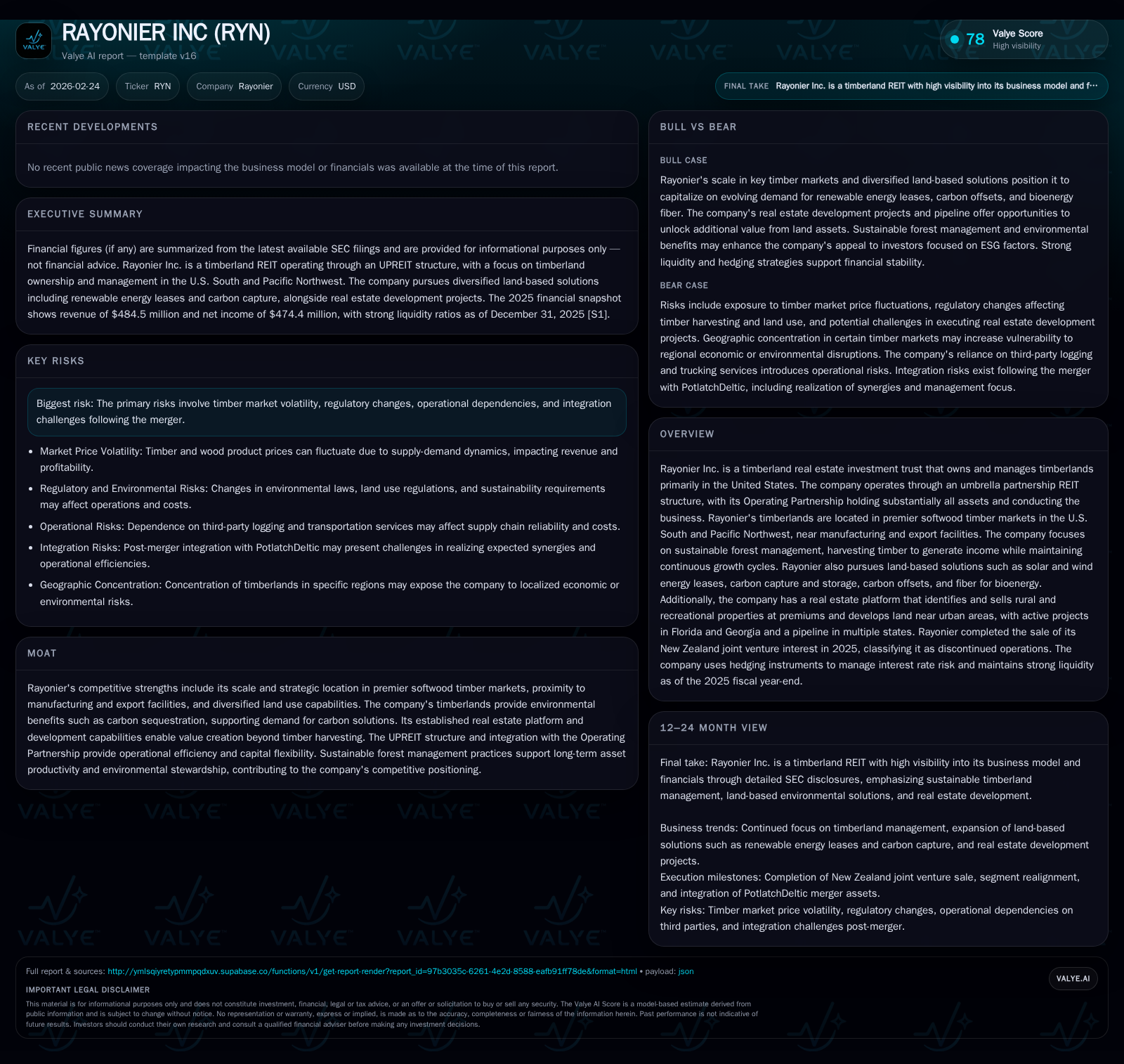

Rayonier Inc. experienced a notable 61.6% drop in revenue in fiscal 2025 compared to 2024, yet its net income grew by 32.1%, reflecting operational resiliency amid timber market cyclicality and portfolio realignment. The company leverages its premier timberland assets through sustainable harvest scheduling and active real estate dispositions, while increasingly capitalizing on carbon solutions and renewable energy leases. Its nimble capital allocation balances steady dividends with opportunistic buybacks and strategic investments. Going forward, market prices, harvest volumes, and carbon revenues are pivotal indicators to follow as Rayonier integrates recent mergers and advances environmental initiatives.

Historical Performance: Revenue Decline Masks Underlying Earnings Strength

Rayonier Inc.’s fiscal year 2025 was marked by a stark revenue contraction of 61.6% year-over-year, dropping from approximately $1.26 billion to $484 million [F1]. This plunge primarily reflects the scheduling of timber harvests influenced by age-class cycling—a common cyclical phenomenon in timberland operations where the volume of harvestable timber fluctuates based on the maturation of stands—and moderate portfolio adjustments post-asset dispositions [S8]. Despite this revenue rollercoaster, net income ascended by a robust 32.1% to $474 million driven by operational efficiencies, favorable non-cash valuation gains related to land assets including leveraged real estate disposals, and a controlled cost base [F1], [S1]. Operating cash flow held steady near $257 million, a mere 1.9% decline from prior-year levels despite top-line pressures, demonstrating strong cash generation resilience (see table below).

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 484 | 474 | 257 | 83 | -61.6% | +32.1% |

| 2024 | 1263 | 359 | 262 | 402 | +19.5% | +107.0% |

| 2023 | 1057 | 173 | 298 | 211 | +16.3% | +62.0% |

| 2022 | 909 | 107 | 269 | 166 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 3 | 21.5 |

| 2024 | 4 | 20.3 |

| 2023 | 4 | 9.3 |

| 2022 | 4 | 5.7 |

Source: SEC companyfacts cache [F1].

Note: Capex data for FY2025 unavailable from provided tags; latest available is FY2022.

This divergence between revenue softness and bottom-line strength highlights Rayonier's capacity to manage volatile harvest-dependent cash flows while monetizing asset values selectively.

Drivers Behind Past Growth: Timber Harvest Cycles and Real Estate Dispositions

Rayonier’s historical top-line growth tracks closely with its timber harvest scheduling calibrated against biological age-class cycles in its forests—timber is harvested when optimal for both growth sustainability and market timing [S8]. The company’s approach purposely targets annual harvests aligned with sustainable yield per segment to preserve long-term stand productivity without depleting inventories.

Supplementing timber sales income are strategic real estate dispositions exploiting the highest and best use (HBU) of certain land parcels—primarily rural and recreational properties selling at premiums above timberland values [S12]. These sales provide portfolio tuning opportunities away from lower-value holdings or those better suited for development-oriented outcomes.

Within this framework, Rayonier’s Southern Timber segment dominates acreage and contributes a steady portion of stumpage revenues due to proximity to major sawmills and export terminals [S6]. The Pacific Northwest segment complements with higher-valued Douglas-fir stands though is smaller in scale.

Shifting Growth Drivers: Emergence of Carbon Solutions and Land-Based Opportunities

Beyond conventional harvesting economics, Rayonier has advanced into emerging land-based solutions aligned with environmental transition themes—solar leases, wind energy contracts on suitable properties, carbon capture & storage agreements leveraging geologic attributes, participation in carbon offset markets via sequestration credits, and fiber provision for bioenergy usage [S12].

This diversification recognizes growing monetization potential of timberlands as natural capital assets delivering ecosystem services beyond wood products alone—secured within an REIT structure beneficial for tax efficiency in qualifying activities [S8]. Leasing arrangements typically require minimal upfront capital from Rayonier but offer recurring alternative income streams enhancing total portfolio returns.

Portfolio Concentration in Premier Softwood Markets: Strategic Importance

Rayonier controls approximately two million acres concentrated principally in the U.S. South (1.69 million acres) and Pacific Northwest (307 thousand acres) regions—both critical supply zones for softwood lumber markets [S20]. This geographic concentration supports operational efficiencies particularly surrounding logistics like cut-and-haul costs optimized near mills or port facilities facilitating export.

Softwood stumpage prices in these markets have historically displayed volatility tied to housing starts cycles but remain among the most liquid globally given export capabilities [N14]. Proximity to manufacturing hubs allows the company to capitalize on regional pricing dynamics while controlling delivery costs—key factors in maintaining competitive operating margins.

Capital Allocation Strategy: Nimble Approach Balancing Dividends, Buybacks, and Investments

Rayonier emphasizes a flexible capital allocation strategy rooted in nimble stewardship that seeks to optimize shareholder value through dividends, buybacks, acquisitions or dispositions based on prevailing market conditions rather than fixed formulas [S4], [S8], [S26]. Maintaining steady dividends aligns with REIT distribution requirements preserving tax advantages while buybacks were scaled down in FY25 following merger-related equity issuance yet still continue modestly as available free cash flow permits (approximately $182 million free cash flow estimated for FY25 after capex) [F1].

Simultaneously, the company invests selectively in infrastructure enhancements around development sites (e.g., Wildlight/Heartwood), acquisitions that concentrate acreage within core markets showing favorable returns prospects, or environmental project development leveraging carbon/leasing upside [S12]. This balanced approach helps sustain healthy returns on equity (~21.5% estimated for FY25 based on net income over equity) while retaining flexibility for tactical moves during cycle troughs or expansions [F1].

Financial Health: Strong Liquidity, Manageable Debt, and Credit Ratings

At year-end FY25, Rayonier reported strong liquidity positions with over $840 million in cash equivalents against current liabilities near $271 million—a current ratio of roughly 3.26x evidencing conservative short-term financial posture [F1], [S5]. The company’s investment-grade debt load is diversified across term loans maturing between 2026–2035 supplemented by revolving credit facilities providing additional capacity [S22], [S27].

Interest rate swaps implement prudential hedging strategies mitigating exposure from floating rates amid rising rate environments common in cyclical commodities sectors like timberland REITs [S18], fostering stable interest expenses over time.

What to Watch Next: Market Prices, Harvest Levels, and Carbon Revenue Trajectory

Looking ahead (analysis), monitored variables will center on softwood stumpage price trends particularly amid housing market fluctuations which drive core demand for lumber products correlated with Rayonier’s southern/Pacific Northwest outputs [N1], [N14]. Adjustments in sustainable harvest volumes responding to evolving age-class profiles can materially impact annual revenue throughput.

Additionally critical are early-stage revenues from carbon sequestration offsets plus solar/wind lease contracts which currently form a small but strategically significant fraction of total cash flow; their scale-up pace could introduce new earnings stability buffers beyond traditional commodity-linked cycles.

The integration progress post-January 2026 PotlatchDeltic merger also bears watching given the enlarged portfolio scales and complexity brought together under the umbrella partnership REIT structure creating synergies but also integration execution risk vectors [S20].

Risks to Monitor: Timber Market Volatility, Regulatory Changes, and Integration Challenges

Key risk exposures include inherent volatility of timber commodity markets driven by macroeconomic cycles affecting stumpage price realizations along with operational dependencies on sustainable yield execution [S8]. Regulatory evolution concerning forestry practices or permitting related to leasing lands for renewable energies or carbon projects may affect business models or timing of new initiatives.

Integration risks following the significant PotlatchDeltic merger represent emergent uncertainties including system harmonization pressures or culture alignment challenges which could transiently impair operational performance or maximum realization of synergy targets.

Disclaimer: This analysis is strictly informational based on publicly available sources as cited up to February 2026; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments