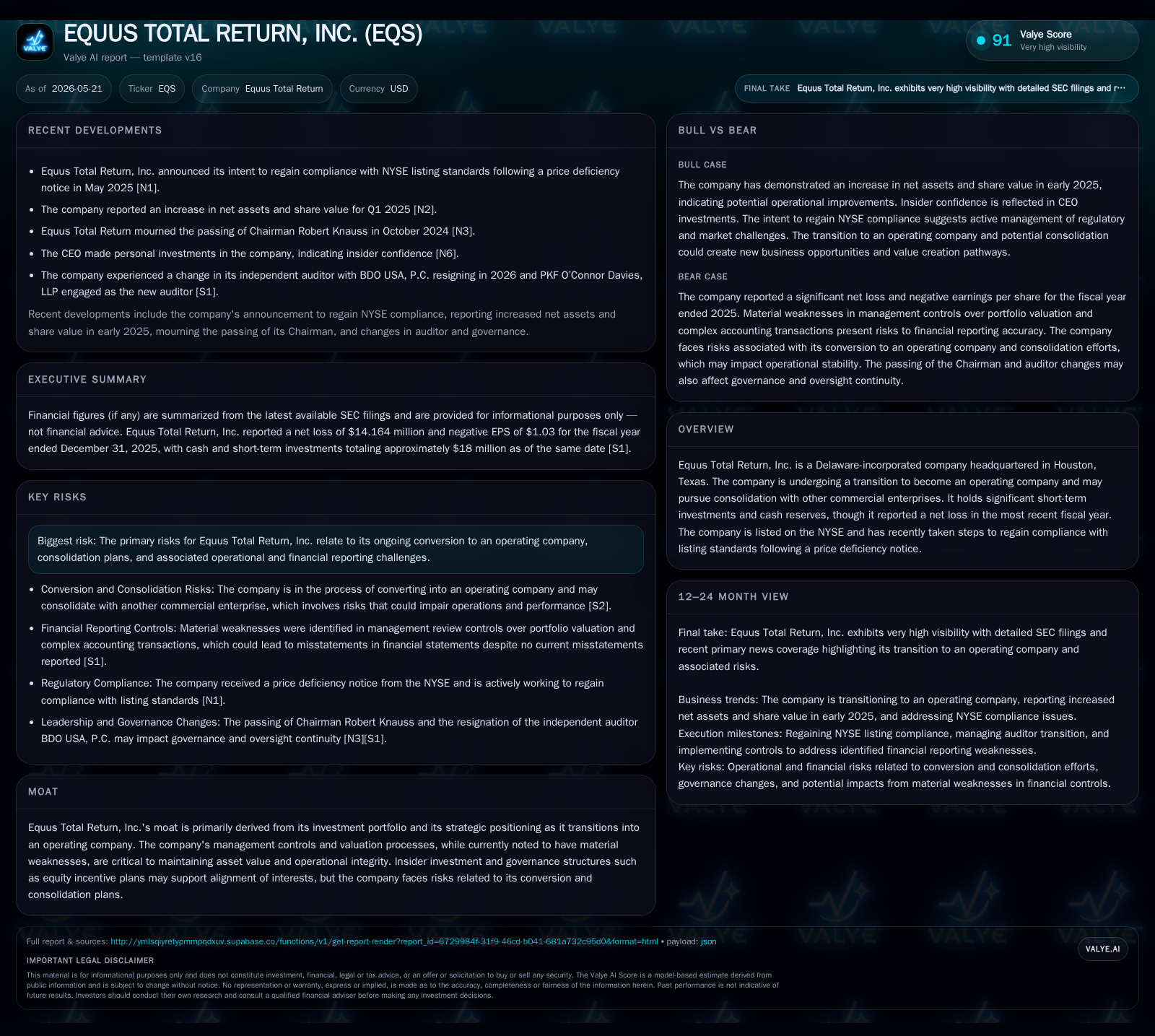

Equus Total Return Initiates Strategic Shift to Operating Company Amid Consolidation Plans

Equus Total Return announces its transition from a business development company to an operating company, outlining consolidation ambitions and operational risks.

In its latest quarterly filing dated May 20, 2026, Equus Total Return, Inc. detailed significant strategic changes as it pursues conversion into an operating company and potential consolidation with commercial enterprises. This marks a shift from its traditional role as a business development company managing debt and equity securities focused on small-to-mid-size companies. The transition entails governance challenges, valuation control weaknesses, and regulatory compliance efforts amid constrained liquidity and ongoing net losses. Monitoring execution of these strategic shifts and risk mitigation will be key to assessing the company's evolving operational viability.

Latest Quarterly Update: Transition and Consolidation Plans Take Center Stage

Equus Total Return’s May 20, 2026 Form 10-Q filing marks a pivotal strategic shift as the company pursues converting from a business development company (BDC) into an operating company [S2]. This transformation represents a fundamental change from its historical focus on investing in small- to mid-market companies via debt and equity securities toward active management within consolidated commercial enterprises. Management highlights inherent risks tied to this restructuring process and the complexities involved in potential consolidation transactions. The filing commits to ongoing disclosure of emerging risks in future SEC reports, acknowledging that additional uncertainties could materially affect operations

Business Model and Investment Approach: From BDC to Operating Company

As detailed in the April 2026 amended annual report (10-K/A), Equus has traditionally operated as a closed-end management investment company electing BDC status under the Investment Company Act of 1940. Its investment strategy targeted privately held or smaller publicly traded companies with total enterprise values typically between $5 million and $75 million. Investment holdings mainly consist of income-producing debt securities—bonds, subordinated debt, convertible debt combined with warrants—alongside common and preferred equity. Warrants serve as instruments for potential capital appreciation through underlying investees' growth.

This model balanced current income generation with long-term capital gains via negotiated direct deals with companies pursuing growth through acquisitions, leveraged buyouts, recapitalizations, or special situations [S1]

A significant change occurred in Q4 2024 when Equus elected not to maintain regulated investment company (RIC) tax status. This ended pass-through tax benefits typical for BDCs qualifying as RICs but provided greater operational flexibility aligned with planned consolidation initiatives.

The evolving business model now emphasizes active operational management within consolidated entities rather than solely managing an investment portfolio. This introduces new revenue mechanisms potentially driven by operating income instead of only interest or dividend income from securities holdings [S1], [S2].

Governance and Valuation Controls during Transition Risks

Recent filings disclose governance challenges accompanying this strategic pivot. Independent auditor reports identified material weaknesses related to management's review controls over portfolio valuations—particularly regarding accuracy of third-party data used for fair value estimates on illiquid securities such as privately held debt and warrants. Controls over measurement and assessment of complex accounting transactions also require improvement.

Although these deficiencies have not resulted in financial misstatements to date, they pose risks to valuation precision affecting reported net asset value and income recognition.

Management introduced new equity incentive plans aimed at aligning interests during this transformation; however, the shift heightens the importance of strong governance oversight to mitigate conflicts of interest, particularly involving affiliated party transactions requiring independent director or SEC approvals [S1], [S2].

Industry Context: Positioning Within the Business Development Company Landscape

Historically, Equus operated within the BDC sector focusing on small-cap private market investments characterized by illiquidity and elevated risk-return profiles relative to larger public peers.

Operating constraints include regulatory requirements such as minimum eligible portfolio asset thresholds (70%), leverage limits mandated by the 1940 Act, and tax qualification conditions. The relinquishment of RIC tax status reflects a tradeoff favoring strategic repositioning over traditional BDC regulatory preferences.

Like many BDC peers investing in private lower-middle market firms, Equus faces valuation opacity challenges due to limited external market data for illiquid holdings. This complicates earnings predictability and investor transparency [S1].

The sector generally balances income yield strategies via secured debt instruments against longer-term capital gains embedded in equity-linked securities or warrants tied to investees' performance.

Growth Drivers: Opportunities From Strategic Shifts and Asset Realignment

Equus's broad investment flexibility across enterprise value ranges supports dynamic transaction structures aimed at maximizing shareholder returns during this transition phase [S2], [S1].

Risks and Constraints: Execution Challenges and Reporting Weaknesses

The transformation entails several risks:

- Complexities in converting legal status while ensuring compliance with SEC rules differentiating operating companies from BDCs;

- Valuation uncertainty for illiquid private investments increases earnings volatility and financial statement risk;

- Material weaknesses in valuation-related internal controls may delay reliable reporting or undermine investor confidence;

- Regulatory pressures including NYSE listing compliance following prior price deficiency notices recalibrate risk profiles;

- Operational integration risks related to consolidating commercial businesses differing fundamentally from portfolio management activities.

These factors present substantial execution challenges impacting near-to-medium term stability [S1], [S2].

What To Watch: Upcoming Milestones and Regulatory Filings

Investors should monitor:

- Updates on conversion progress detailed in future quarterly SEC filings including disclosures on newly identified or mitigated risks;

- Effectiveness of governance improvements assessed through auditor reports under new independent accountant PKF O’Connor Davies LLP after prior auditor resignation in April 2026;

- Announcements regarding consolidation partners or definitive transaction agreements clarifying post-transition operational scope;

- Resolution status of internal control deficiencies affecting valuation accuracy critical for credible financial disclosures;

- Regulatory responses related to listing compliance remediation or tax election impacts on capital structure [S3], [S2].

Financial Snapshot: Supporting Metrics Reflecting Current Position

For fiscal year ended December 31, 2025, Equus reported a net loss of approximately $14.16 million reflecting challenges in portfolio valuation adjustments combined with costs related to transition efforts [F1]

The modest asset base underscores reliance on successful execution of strategic initiatives alongside governance enhancements to stabilize financial footing amid ongoing operational changes.

This analysis is based exclusively on public SEC filings by Equus Total Return, Inc., including the latest quarterly report filed May 20, 2026. It avoids speculative extrapolation or investment research views.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments