Expeditors’ Stable Profits and Technology-Driven Customs Growth Offset Trade Volatility

Expeditors International sustains profitability via AI-enhanced customs brokerage and diversified freight services amid shifting global trade dynamics.

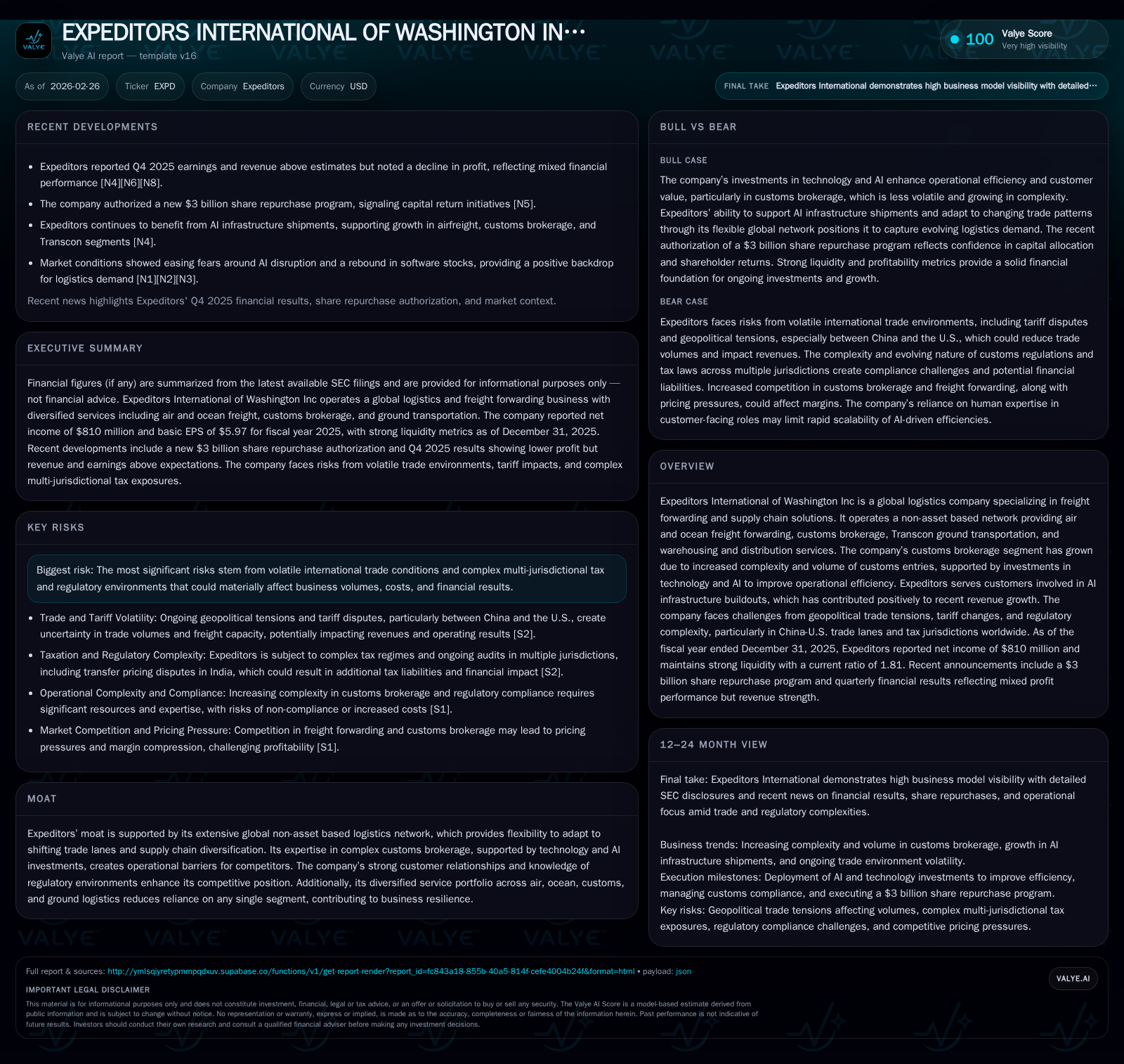

Expeditors International of Washington Inc leverages its expansive non-asset global logistics network and technology investments to deliver consistent profitability and revenue growth. Despite geopolitical trade tensions impacting key China-U.S. lanes, its growing customs brokerage segment—powered by AI and complex regulatory expertise—bolsters resilience. Capital returns remain robust through dividends and significant share repurchases. Going forward, trade uncertainties and tax complexities pose risks, while AI infrastructure shipments and customs process enhancements offer growth avenues.

Historical Financial Performance

Expeditors International has demonstrated modest top-line growth alongside consistent profitability over recent years. Fiscal revenue increased from $1.64 billion in 2016 to roughly $1.90 billion in 2017; more recently, the company reported a 15.8% revenue increase for FY2025 over FY2024, reaching operating income just over $1.05 billion (a slight rise of 1.1%) and net income steady at about $810 million [F1]. This stability reflects Expeditors’ ability to navigate volatile global trade environments exacerbated by tariff actions and geopolitical tensions.

The operating cash flow rose sharply by nearly 40%, crossing the $1 billion mark in FY2025, indicating strong underlying cash generation capacity that supports capital returns and investments [F1]. Meanwhile, capital expenditures rose modestly by about 31%, focusing largely on IT infrastructure upgrades including cybersecurity and AI capabilities.

Historical performance (annual)

| FY | Net ($mm) | CFO ($bn) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 810 | 1.0 | 1053 | 53 | +0.0% |

| 2024 | 810 | 0.7 | 1041 | 40 | +7.6% |

| 2023 | 753 | 1.1 | 940 | 39 | -44.5% |

| 2022 | 1357 | 2.1 | 1824 | 87 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($bn) |

|---|---|---|---|

| 2025 | 207 | 667 | 1.0 |

| 2024 | 204 | 855 | 0.7 |

| 2023 | 202 | 1393 | 1.0 |

| 2022 | 214 | 1582 | 2.0 |

Source: SEC companyfacts cache [F1].

*Approximate based on latest sources; older revenues before restructuring noted in filings [F1]

Business Drivers Behind Past Performance

Expeditors operates a non-asset-based global logistics network offering air/ocean forwarding, customs brokerage, ground transportation (Transcon), and warehousing [S6]. This diverse portfolio shields it from reliance on individual segments prone to volatility.

The customs brokerage business has been a standout contributor to growth, fueled by an increase in volume and complexity of customs entries requiring detailed paperwork—some evolving from simple few line items to hundreds per entry—and corresponding fee increases to offset this labor intensiveness [S8][S14]. Customized customer webinars educating clients on tariff updates bolster trust and help win additional business.

Airfreight volumes have benefited from sustained demand related to emerging sectors like AI infrastructure build-outs—a notable growth driver throughout recent quarters—as well as e-commerce tailwinds supported by policy shifts such as the elimination of de minimis thresholds into the U.S., which led Asian shippers to accelerate shipments prior to tariff changes [S15][S17]. Ocean freight has faced softening rates due to capacity expansions but remains important in Expeditors' mix.

Future Growth Prospects

Looking ahead, Expeditors sees opportunities in leveraging AI-driven productivity enhancements for customs operations and compliance processes while maintaining high-touch customer engagement functions intact [S19]. The company’s technological investments target operational efficiency gains that should increase profitability per transaction as well as scale handling of ‘post-entry’ filings that involve revisions or additional documentation after goods clearance—a potentially substantial new service area.

However, growth is challenged by persistent geopolitical uncertainty—especially ongoing China-U.S. tariff disputes which still account for roughly one-fifth of revenue but are trending lower as customers diversify supply sources to alternative Asia-Asia or nearshore corridors [S5][S6][S14]. The unpredictability of trade volumes induced by tariffs forces periodic capacity fluctuations among carriers that impact freight availability and pricing.

Tax regulatory risk also looms large as Expeditors navigates complex multinational taxation rules intensified by new global minimum tax regimes (OECD Pillar Two). Outcomes from ongoing audits across jurisdictions like India could affect future results significantly though management currently defends its positions aggressively [S10][S11].

What To Watch: Forecasts & Milestones

No formal guidance was provided for FY2026; however, management highlighted continuing customs brokerage expansion driven by rising work per entry volume alongside AI-enabled operational improvements expected to be accretive despite required personnel investments for higher volumes [S14][S17].

Market watchers should monitor:

- Trends in air/ocean freight volumes particularly in key trade lanes affected by tariffs or shifting supply chains;

- Growth trajectory and pricing power within customs brokerage services including uptake of ‘post-entry’ filings;

- Progress on technology adoption specifically AI tools supporting productivity gains;

- Regulatory developments related to international taxation policies;

- Capacity changes among independent air/ocean carriers affecting service levels.

Returns & Capital Allocation

Expeditors maintains a disciplined capital allocation strategy aligned closely with profitability metrics rather than revenue growth alone [S19][S23]. As evidenced in FY2025 data, the firm paid out around $207 million in dividends while buying back $667 million worth of shares—both substantial absolute amounts demonstrating management’s commitment to returning cash to shareholders even during uneven revenue environments (compared with $855 million buybacks in FY2024) [F1][N11][S18].

The broad repurchase authority renewed at $3 billion signals continued shareholder distribution intent going forward [N11]. This is supported by robust free cash flow exceeding approximately $950 million after capex spend (CFO minus capex) for FY2025—a level combining operational strength with moderate capital investment requirements typical for non-asset-based operators [F1].

With an estimated return on equity above 34%, Expeditors exhibits attractive efficiency given limited asset intensity combined with high working capital turnover inherent in forwarding/brokerage functions [F1].

Competitive Moat & Industry Context

Expeditors’ moat centers on its extensive global non-asset network which allows flexibility missing from asset-heavy competitors tied to fixed infrastructure or owned fleets. The company’s deep expertise navigating increasingly labyrinthine customs environments creates operational barriers through knowledge-intensive processes especially as regulations evolve rapidly worldwide.

This is underpinned by sustained technology investments deploying AI not merely for cost cutting but enhancing compliance accuracy and customer value-added services that smaller brokers or regional operators may struggle to replicate at scale [S14][S19]. Additionally, Expeditors benefits from solid long-term relationships with hyperscalers investing aggressively in AI infrastructure—a sector driving specific product line growth like airfreight shipments tailored for high-value technologies.

Still, sensitivity remains high toward macro trade shifts; should pandemic-era or tariff-induced supply chain reorientations slow materially or reverse quickly, underlying volumes might compress significantly.

Risks Summary

Key risks stem from:

- Geopolitical and intergovernmental disputes causing tariff volatility impacting core China lanes heavily embedded in revenues (~22%) [S5];

- Increasingly complex taxation regimes globally imposing financial uncertainties especially around transfer pricing disputes like those ongoing with Indian authorities [S10];

- Elevated investment needs to keep pace technologically while managing human capital intensively amidst rising shipment complexity;

- Carrier capacity fluctuations beyond Expeditors’ control affecting transit times/pricing crucial for customer retention.

Conclusion

Expeditors International holds a nuanced position balancing strong financial discipline against external challenges mainly stemming from geopolitics and regulation complexity. Its advanced customs brokerage platform enhanced via AI investments underwrites stable profit margins even as freight volumes face pressure due to tariffs.

Monitoring developments in customs workload intensity alongside trade lane diversification proves critical going forward given their sizable impact on revenue sources. Meanwhile, ongoing share repurchases underscore management’s confidence in the firm’s strategic positioning amid uncertainty—the hallmark traits of its stewardship style shown consistently over past periods.

Disclaimer: This analysis is intended solely for informational purposes summarizing corporate developments based on publicly available regulatory filings and news reports up to February 26, 2026; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments