First Citizens BancShares’ Financial Performance and Expansion in Regional Banking

Analyzing First Citizens BancShares’ recent financial performance, credit strategy, geographic expansion, and capital deployment within regional banking.

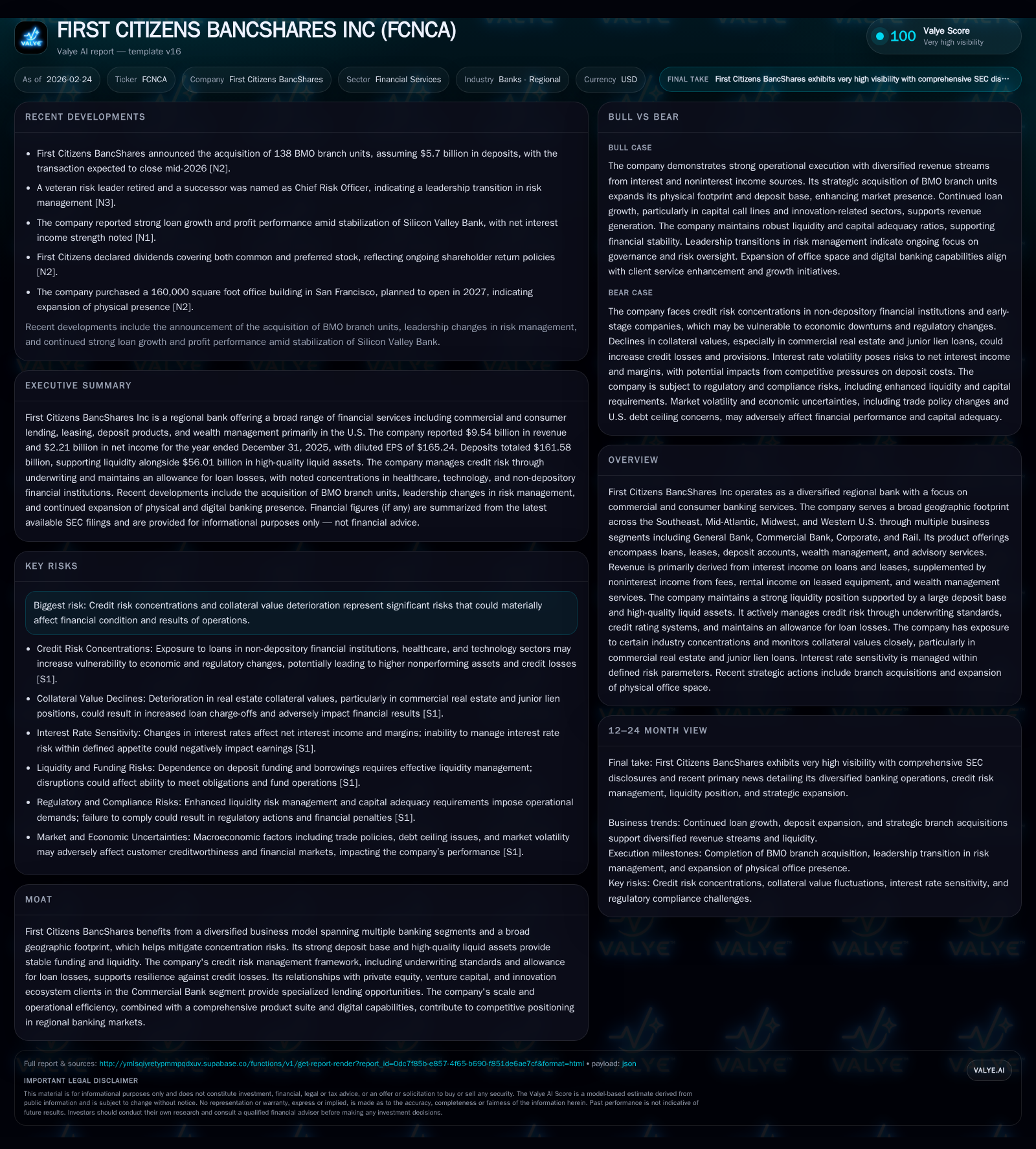

First Citizens BancShares has demonstrated resilient financial performance with a slight revenue decline in 2025, underpinned by robust operating cash flow and solid loan portfolio growth. The company’s disciplined credit risk management, including a comprehensive allowance for loan losses system, supports its stability amid evolving economic conditions. A strategic acquisition of 138 BMO branches, adding $5.7 billion in deposits, extends its geographic reach in key U.S. markets. Capital allocation emphasizes significant share repurchases alongside steady dividend payments, delivering an approximate 10% return on equity. Going forward, growth will hinge on integrating acquisitions, managing regulatory capital requirements, and navigating credit concentrations and competitive pressures.

Historical Financial Performance and Key Growth Drivers

First Citizens BancShares reported revenues of approximately $9.54 billion for fiscal year 2025, marking a modest decline of 2.2% from $9.76 billion in 2024 [F1]. This dip coincided with a sharper contraction in net income of about 20.6%, falling to $2.21 billion from the previous year's $2.78 billion [F1]. Despite top-line softness, operating cash flows exhibited resilience at nearly $2.92 billion in 2025 compared to $2.99 billion in the prior year—a marginal decline reflecting stability in core cash generation from loan repayments and fee income streams [F1]. Capital expenditures surged to $710 million in the same period from $429 million a year earlier, largely attributable to investments supporting branch upgrades and technology platforms [F1].

The revenue performance reflects competitive deposit pricing dynamics influencing net interest margin (NIM) compression despite healthy commercial loan growth concentrated across multiple segments including Corporate banking and General Bank divisions [N3][N4][S23]. Notably, noninterest income sources such as wealth management fees and equipment rental revenues contributed supplementary income cushioning interest income volatility. Deposit base expansion also helped maintain funding stability.

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 9.5 | 2.2 | 2.9 | 710 | -2.2% | -20.6% |

| 2024 | 9.8 | 2.8 | 3.0 | 429 | -75.8% | |

| 2023 | 11.5 | 2.7 | 405 | +944.3% | ||

| 2022 | 1.1 | 2.8 | 155 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($bn) | FCF ($bn) |

|---|---|---|---|

| 2025 | 161 | 3.0 | 2.2 |

| 2024 | 158 | 1.6 | 2.6 |

| 2023 | 117 | 0.0 | 2.3 |

| 2022 | 83 | 1.2 | 2.6 |

Source: SEC companyfacts cache [F1].

Note: Operating income data not available; net income reflects some nonrecurring items in prior years.

Credit Risk Management Framework and Portfolio Quality Insights

Credit risk constitutes a critical area of focus given its direct influence on asset quality and capital adequacy metrics [S1][S4]. First Citizens employs a multilayered credit rating system assessing probability of default (PD), loss given default (LGD), with models calibrated using internal and external historical data complemented by borrower-specific qualitative adjustments [S22]. The company’s provisioning coverage ratio—measuring the allowance for loan and lease losses (ALLL) relative to total loans—is closely monitored amid uncertain macroeconomic conditions impacting borrowers’ repayment capabilities.

Management acknowledges the inherent difficulty in forecasting future credit losses due to variable economic factors including sectoral concentration risks notably in commercial real estate (CRE) and owner-occupied commercial mortgages distributed primarily across California (21%), New York (10%), North Carolina (9%), Texas (7%), and Massachusetts (6%) [S13]. The consumer loan concentration is similarly notable with nearly a third of consumer loans based in California [S13][S16]. Cyclical stress patterns may require incremental provisioning impacting earnings volatility.

Furthermore, collateral value deterioration remains a latent risk particularly amid inflationary pressures and changing property market dynamics [S19]. The company’s ALLL adjustments are subject to regulatory reviews which may necessitate reserve augmentations posing downside earnings risks.

Strategic Branch Acquisition: Expanding Geographic Footprint

In early 2026, First Citizens announced the acquisition of a substantial portfolio of Bank of Montreal (BMO) USA branches comprising 138 locations with deposits approximating $5.7 billion—a transaction expected to close mid-year [N11][N12][S23]. This strategic move broadens FCNCA’s geographical coverage into new markets within Southeast, Mid-Atlantic, Midwest, and Western regions enhancing customer acquisition channels and cross-sell potential.

Branch network expansion through such acquisitions leverages economies of scale benefiting funding cost reduction via increased low-cost deposits predominated by noninterest-bearing and savings segments which together rose by around $6 billion or roughly +10% as per deposit category breakdowns for year-end December 31, 2025 versus prior year [S5][S16]. This scale advantage enhances liquidity buffers allowing more nimble underwriting during tightening credit cycles.

However, integration risks include systems harmonization challenges, cultural alignment within newly acquired units, and the necessity to preserve asset quality through consistent credit policies applied uniformly across legacy and acquired portfolios.

Future Growth Outlook and Potential Constraints

Looking ahead, growth drivers identified include expanding commercial banking relationships especially within private equity-backed clients serviced through Corporate Bank operations alongside technology-enabled lending solutions accentuating agility [N2][S23]. Additionally, wealth management upselling remains a fertile area given demographic tailwinds.

Conversely, headwinds comprise anticipated margin pressure driven by competitive deposit pricing required to attract/retain clients amid higher interest rate environments along with cautious loan demand trends stemming from cautious corporate capex spending [N3][N4]. Regulatory changes related to Basel III Endgame imposing higher capital charges may constrain balance sheet leverage lending capacity pushing banks towards more capital-efficient products or securitizations [S7][S10].

Monitoring indicators include quarterly margin development trends, deposit retention rates post-acquisitions to validate synergies realization versus churn risks, shifts in provisioning levels signaling early warning on emerging credit stress.

Capital Allocation Priorities: Dividends, Buybacks, and Return on Equity

First Citizens BancShares deployed capital aggressively towards shareholder returns with approximately $3 billion executed in share repurchases during fiscal year 2025 under its ongoing repurchase programs initiated mid-2024 continued through 2025; this marks a material step-up from prior years’ repurchase activity that totaled $1.65 billion in FY2024 alone [F1][S20].[N2]

Dividend payments similarly advanced moderately reaching about $161 million up from $158 million indicating cautious yet consistent upward trajectory aligned with payout policy emphasizing sustainability amidst capital accumulation needs [F1].[S20]

Despite headline net income compression in FY2025 affecting absolute profit levels carried through reported equity balance near $22.24 billion results in an approximate return on equity (ROE) near the high single digits (~9.9%), reflecting balanced capital efficiency considering growth investments made alongside conservative reserve postures [F1].[N3]

The interplay between retained earnings fueling organic growth avenues versus distributable cash returned via buybacks conveys deliberate capital stewardship balancing competitive positioning with regulatory capital sufficiency requirements given enhanced prudential standards for institutions exceeding $100B assets threshold like FCNCA [S7][S29].

Digital Capabilities and Operational Efficiency as Competitive Differentiators

Operational excellence backed by digital transformation is pivotal for regional banks competing against both traditional peers and fintech disruptors alike. First Citizens emphasizes governance structures placing cybersecurity as a board-level agenda item with oversight managed through the Technology Committee empowered by specialized cybersecurity officers responsible for threat detection/prevention frameworks grounded in over a decade of domain expertise [S1]. These measures mitigate operational risks including data breaches that could hamper client trust or incur costly regulatory penalties.

Digital platforms enhance underwriting workflows enabling automation that reduces processing time especially for commercial lending while bolstering customer engagement through omnichannel access points blending branch network strength with advanced online/mobile capabilities – crucial differentiators highlighted during recent earnings discussions [N5].[S23]

Such investments contribute indirectly to margin preservation even as external rate pressures squeeze traditional net interest margin components.

Risks Impacting Future Profitability and Credit Loss Resilience

Key risk vectors center on credit concentration vulnerabilities within commercial real estate sectors susceptible to market dislocations amplifying potential charge-off spikes challenging reserve adequacy assumptions embedded within ALLL calculations discussed earlier [S4][S19].[S21] Legal exposures arising from ongoing or future litigation related to past acquisitions or standard business disputes represent contingent liabilities that may influence future expense trajectories although presently managed conservatively through provisions where probable losses can be estimated [S15].[N3]

Regulatory compliance risks also merit attention given evolving consumer protection statutes alongside privacy/data security mandates requiring continuous adaptation possibly elevating operating costs while noncompliance could incur fines or reputational damage disproportionately impactful at regional bank scales relative to larger global players [S6].[S9]

Liquidity risk is satisfactorily managed via diversified funding sources inclusive of direct retail deposits supplemented by Federal Home Loan Bank advances maintaining well-above regulatory-required liquidity coverage ratios (LCRs), yet unexpected withdrawal shocks remain plausible scenarios necessitating contingency planning vigilance as underscored post-Silicon Valley Bank failure industry-wide reassessments highlight heightened deposit sensitivity environment factors causing renewed supervisory scrutiny expectations for stress testing rigor reinforcement at FCNCA scale institutions [N13].[S10]

Disclaimer: This report is offered solely for informational purposes without any recommendation regarding securities purchases or sales or other investment activities involving First Citizens BancShares Inc (FCNCA). It is based on publicly available data as of February 24, 2026 without prediction or projection beyond stated facts or guidance explicitly cited herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments