Fenbo Holdings Rebounds from Nasdaq Compliance and Tariff Pressures

After regaining Nasdaq compliance, Fenbo navigates a challenging 2025 marked by tariff-driven revenue declines while leveraging its OEM expertise and manufacturing scale.

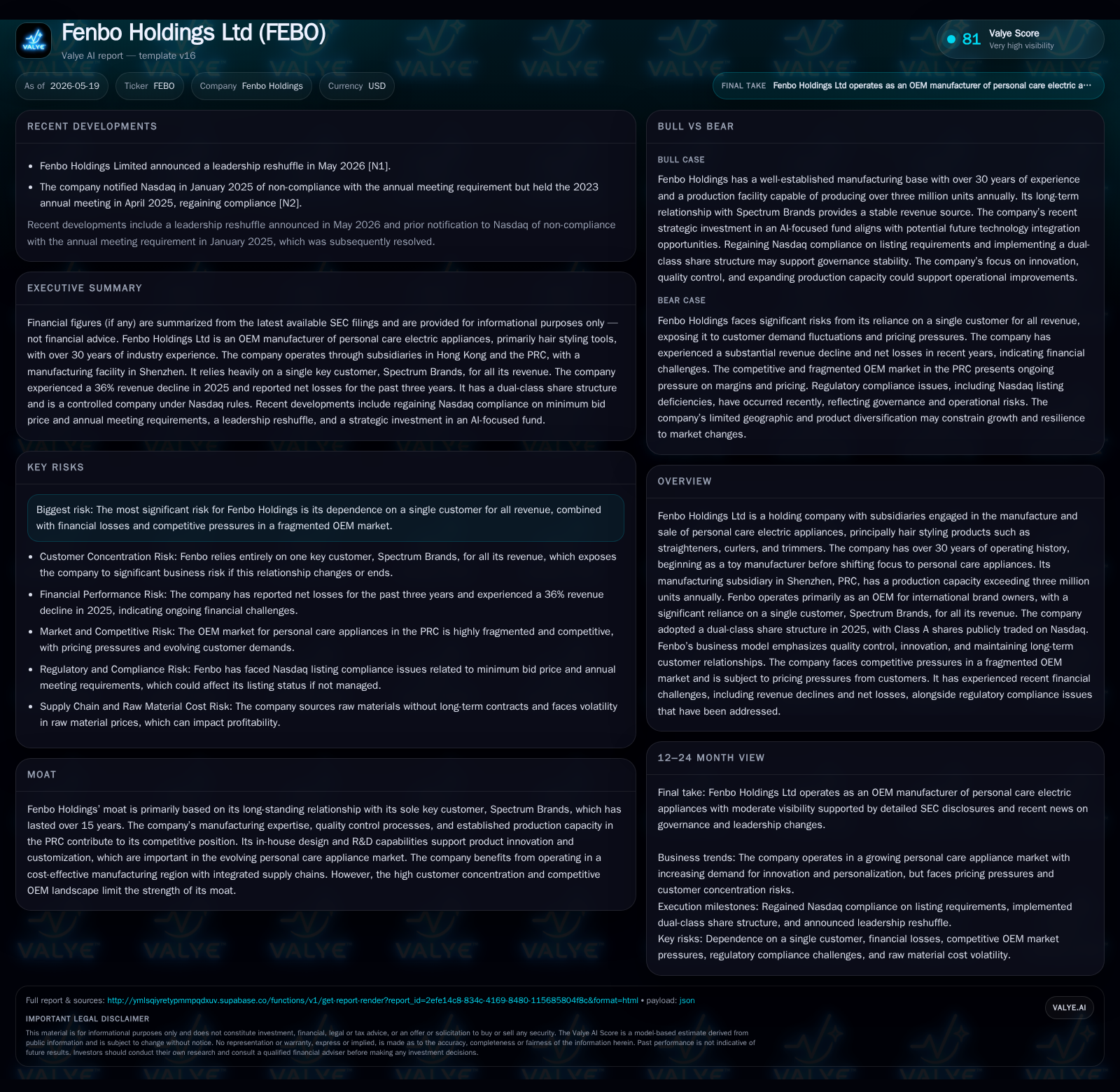

Fenbo Holdings regained compliance with Nasdaq’s minimum bid price in late 2025, stabilizing its listing status. However, the company faced a significant revenue decline of 36% in 2025, primarily due to sustained U.S.-China tariff pressures that dampened order volumes from its sole customer, Spectrum Brands. Operating as an OEM specializing in personal care electrical appliances, Fenbo’s extensive manufacturing capacity and long-standing customer relationship underpin its competitive position despite margin compression. Key risks remain concentrated customer dependence and geopolitical trade uncertainties. Going forward, Fenbo’s growth hinges on navigating trade barriers, sustaining product innovation, and expanding market reach.

Nasdaq Compliance and Latest Quarterly Performance

Fenbo Holdings Limited addressed a critical near-term listing concern when Nasdaq confirmed on December 31, 2025 that the company had regained compliance with the Minimum Bid Price Rule requiring shares to close at or above $1.00 for at least ten consecutive business days [S2]. This regulatory milestone stabilized the company's public market presence after a notification back in September 2025 highlighted non-compliance risks triggered by share price declines.

Despite regulatory success, operational challenges persisted through 2025. The company reported revenues of approximately HK$85 million (US$10.9 million), down roughly 36% from HK$132.9 million in 2024 amid sustained tariffs imposed by U.S.-China trade policies impacting import costs [S1]. These tariffs induced Spectrum Brands — Fenbo’s sole and dominant customer — to reduce purchase volumes and shipment frequencies. Resulting revenue pressure reduced gross profit margins to around 12.9%, down from about 18.7% the previous year. Consequently, Fenbo posted an operating loss of approximately HK$8.6 million (US$1.4 million) for the fiscal year ended December 31, 2025 [S1][F1].

The revenue contraction and margin compression during this period reflect both external headwinds from geopolitical trade friction and internal constraints tied to single-customer dependency.

Business Model and Product Portfolio Overview

Fenbo Holdings operates primarily as an Original Equipment Manufacturer (OEM) producing personal care electric appliances focused on electrical hair styling devices such as straighteners, curlers, and trimmers [S1][F1]. Its customer-centric business model revolves around a long-term partnership exceeding fifteen years with Spectrum Brands, supplying electrical haircare products marketed principally under the Remington brand across Europe, the United States, and Latin America.

The company’s manufacturing subsidiary situated in Shenzhen has an annual production capacity exceeding three million units—a scale that supports volume commitments but also mandates consistent operational efficiency and quality control to maintain client trust [S1]. FPPF handles both manufacturing and in-house R&D capabilities supporting product design innovation necessary for customization as consumer tastes evolve.

Fenbo's revenue mechanics involve fixed-price contracts once orders are confirmed by the sole customer. This creates exposure to raw material cost fluctuations that cannot be immediately passed through, squeezing margins especially amid rising input costs or tariff increments [S1]. The dual-class share structure implemented in September 2025 enhances controlling shareholders’ influence by consolidating voting rights into Class B shares while keeping Class A shares publicly traded under ticker "FEBO" on Nasdaq [S1].

Industry Dynamics and Competitive Positioning

Fenbo competes within a fragmented global OEM landscape for personal care appliances where customers often exert substantial pricing pressure due to product commoditization risks [S1]. Competing suppliers in China benefit from geographic proximity to raw materials yet face challenges differentiating offerings absent proprietary brands or technology advantage. Fenbo's established relationship with Spectrum Brands provides a strategic moat derived from trust built over multiple supply cycles; however, this moat is fragile given total reliance on one major customer

The need for continuous innovation remains critical as consumer preferences shift toward technologically enhanced grooming solutions integrating features like smart temperature controls or cordless designs. Investment in R&D then becomes vital both to meet evolving specs demanded by brand owners like Spectrum Brands and to maintain relevance against peers who may prioritize niche segments or volume discounts.

Supply chain integration centered around Fenbo's PRC-based facilities offers cost advantages but exposes it to geopolitical risks that can directly impact logistics costs and procurement management—factors increasingly significant given ongoing U.S.-China tariff uncertainties.

Growth Opportunities and Innovation Focus

Despite recent headwinds, Fenbo benefits structurally from secular tailwinds in beauty appliance growth driven by increased grooming consciousness across demographic groups—especially Millennials—with rising adoption among men expanding total addressable market size [S1]. The geographic sales footprint includes expansion potential into US and Latin American markets where beauty appliance penetration continues growing.

The company’s ongoing efforts to enhance margin resilience involve optimizing product mix toward higher-value SKUs alongside strengthening engineering capabilities within FPPF’s R&D division to fast-track new product introductions tailored for dynamic fashion trends [S1]. Greater emphasis on sustainable materials or energy-efficient device functions could further differentiate offerings aligned with consumer expectations.

Scaling existing production capacity remains feasible given underutilized throughput relative to maximum output; however, execution hinges on securing reorder volumes from Spectrum Brands or diversifying clientele—a prospect challenged by current concentration but critical for growth beyond volatility periods.

Key Risks: Customer Concentration and Trade Barriers

Fenbo faces pronounced risk stemming from its entire revenue dependence on a single customer group—Spectrum Brands—with no alternative clients contributing meaningful sales currently documented [S1][F1]. This restricts negotiating leverage over pricing or contractual terms adversely affecting margin sustainability.

Additional downside stems from tariff policies between the U.S. and China which have led to reduced procurement orders disrupting revenue visibility into near-future quarters [S1]. Tariffs inflate landed cost structures without corresponding contract repricing flexibility due to fixed-price order commitments once placed.

Raw material price volatility compounds risk owing to limited bargaining power against suppliers offering globally commodity-like components such as plastics and electrical parts [S1]. The company's general administrative costs ratio rose notably during soft demand phases indicating some operating leverage risk.

Moreover, macro-political uncertainties including shifts with new U.S. administrations or Chinese export controls could induce sudden disruptions affecting Fenbo’s operational cadence or logistics expenses.

Upcoming Catalysts and Operational Milestones

Key upcoming factors to monitor include potential easing of trade tensions which would likely restore order frequency from Spectrum Brands prompting volume rebound; internal operational initiatives post-leadership reshuffle announced May 19, 2026 could also drive tighter expense controls or strategic diversification efforts [N1][S2][S1]

Given Fenbo’s recent adoption of a dual-class share structure concentrating control among founders while keeping public float under Nasdaq oversight, corporate governance stability will remain under scrutiny alongside adherence to compliance guidelines.

Investors should track quarterly order bookings as leading indicators of demand recovery plus any announcements regarding diversification beyond spectrum brands or capacity investments signaling strategic shift.

Financial Position and Operating Results Summary

As of December 31, 2025, Fenbo reported an operating loss of approximately US$1.4 million reflecting the adverse impacts of shrinking revenues driven chiefly by tariff-induced procurement pullbacks [F1][S1]. The gross margin declined sharply from nearly 19% in prior years to about 13%, evidencing cost pressures not offset by pricing adjustments due to fixed-price contracts.

Balance sheet liquidity appears sufficient with a current ratio around 2.07 based on US$7.6 million current assets versus US$3.7 million current liabilities providing moderate short-term buffers despite operating losses [F1]. Cash reserves include approximately US$2.4 million enabling working capital support through cyclical troughs.

Interest expenses remain manageable relative to cash flows given modest bank borrowing facilities recently reduced from prior periods reflecting prudent leverage management [S14][F1]. The company does not currently pay dividends directing earnings toward operational needs amid profitability recovery attempts [S7].

Overall financial posture supports ongoing operations through uncertain near-term demand conditions while emphasizing need for growing order streams aligned with tariff landscape improvements or diversification strategies.

This analysis is based solely on reported filings and disclosures up to May 19, 2026 and does not constitute investment advice.

Financial position in context

Current assets of $8mm and current liabilities of $4mm imply a current ratio near 2.07x for 2025-12-31 [F1]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments