Flowers Foods Rebalances Dividend and Navigates Leadership Turnover Amid Debt Refinancing

Flowers Foods reports a Q1 revenue beat alongside strategic dividend reset and executive changes amid debt refinancing efforts.

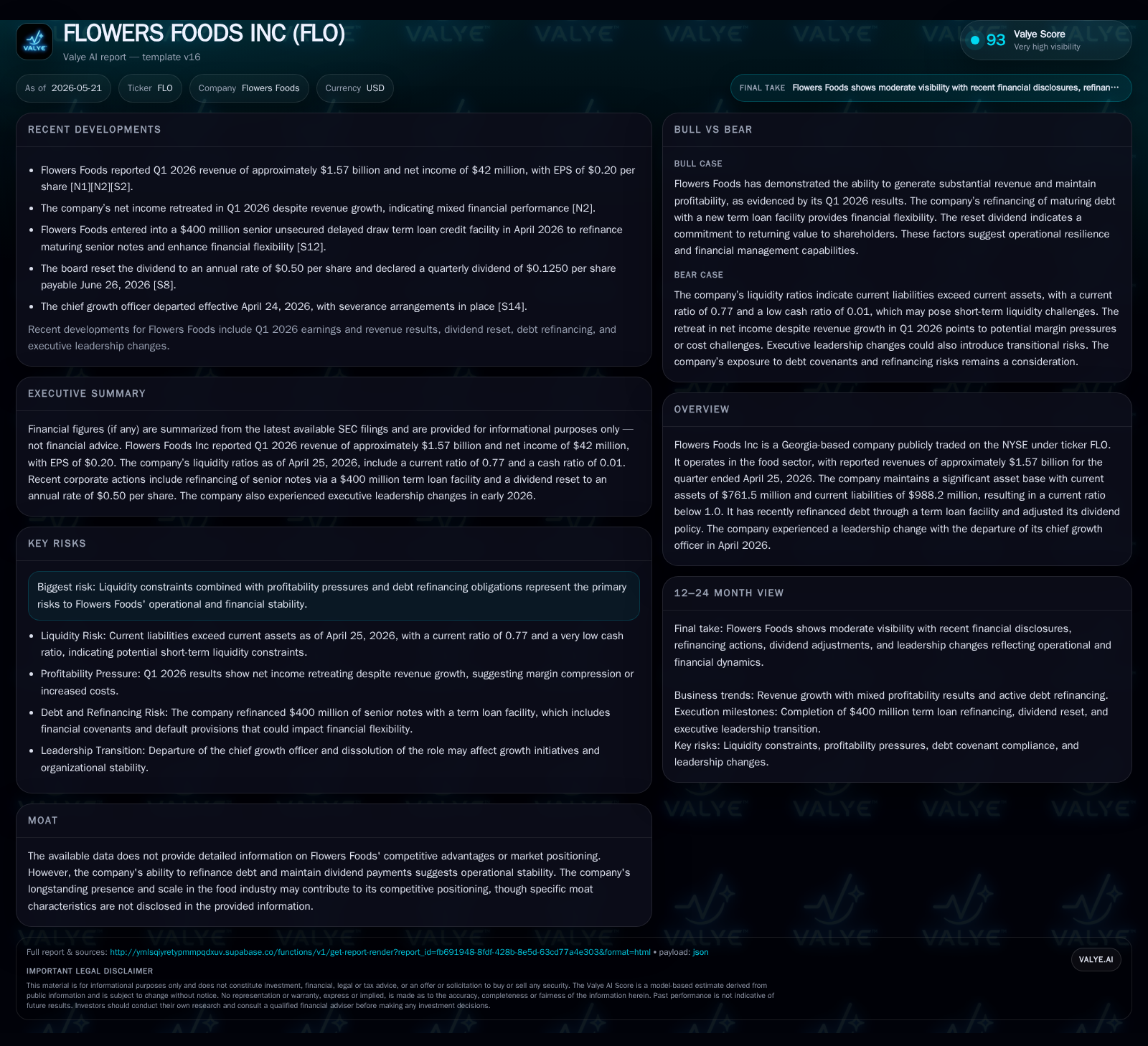

In the latest quarter ended April 25, 2026, Flowers Foods demonstrated operational resilience by exceeding revenue expectations despite ongoing liquidity constraints. The company’s board reset the dividend to an annual rate of $0.50 per share, signaling a cautious capital allocation stance while managing debt refinancing obligations. Concurrently, leadership shifts including the departure of the chief growth officer introduce uncertainties around growth execution. Within the competitive food sector landscape, Flowers Foods leans on product innovation and supply chain efficiencies as key growth drivers amid persistent cost pressures.

Latest Operating Update: Earnings Beat and Corporate Actions

In its May 21, 2026 Form 10-Q filing [S2], Flowers Foods reported quarterly revenues of approximately $1.57 billion—surpassing analyst estimates and showcasing sustained consumer demand for its bakery products. This performance suggests operational resilience despite sector-wide raw material inflation pressures noted in recent industry commentary [N1].

Alongside earnings disclosures in a contemporaneous 8-K filing [S3], the company’s board announced a dividend reset to an annual rate of $0.50 per share from prior levels, accompanied by a quarterly dividend declaration of $0.125 per share payable late June 2026. This strategic move reflects a prudent capital allocation response aimed at preserving liquidity during refinancing efforts.

Adding complexity to near-term outlooks, Flowers experienced the departure of its Chief Growth Officer in April 2026—a critical role responsible for driving innovation and market development initiatives. This transition introduces uncertainty around executing growth strategies that rely on product diversification and geographic footprint expansion.

Finally, the company undertook debt refinancing via a new term loan facility recently completed [S2][S3], seeking to optimize its capital structure during elevated leverage. The revenue generation hinges on volume sales of a broad product range including fresh breads, buns, rolls, snack cakes, and tortillas.

Customers are mainly retailers who pay for these products under negotiated contracts that often constrain pricing adjustments due to competitive pressure and consumer price elasticity. Consequently, revenue dynamics depend heavily on volume throughput combined with modest price increases aligned with inflation trends.

Ensuring consistent product quality and reliable supply chain operations is paramount given consumer expectations for freshness and availability. Production inputs such as wheat flour, corn derivatives, soybean oil, sweeteners, and energy commodities represent significant cost components [S1]. Flowers employs commodity futures hedging to stabilize input cost exposure—especially wheat and natural gas—thereby reducing earnings volatility from market fluctuations

Distribution breadth is a key structural advantage; the company leverages regional bakeries geographically spread to optimize product freshness logistics and reduce transportation costs. Brand loyalty among end consumers creates moderate switching costs that help defend market share in certain segments despite intense competition.

Industry Context: Competitive Positioning and Supply Dynamics

Within the broader food sector encompassing baked goods producers, Flowers Foods competes against similarly scaled firms offering commodity-like bakery items where differentiation beyond price-quality balance is limited. Consumer staple nature of bread products offers somewhat stable demand but sets sales largely prone to macroeconomic conditions affecting discretionary spending.

Pricing power is generally muted given retailer dominance negotiating terms that compress margins; thus supplier players like Flowers pass through input inflation cautiously so as not to erode shelf velocity [N1][S1]. The company’s ability to deploy commodity risk management for key raw materials is critical in managing margin pressures amid volatile agricultural markets [S1].

Regulatory oversight primarily relates to food safety standards and labeling compliance rather than restrictive capacity constraints or tariffs. Operational scale serves as a barrier for smaller competitors lacking expansive distribution networks or hedging sophistication but does not constitute a pronounced moat against other large incumbents.

Operational stability evidenced by successful debt refinancing and maintained dividend payments support the company's creditworthiness relative to peers navigating similar cost challenges [S3]. However, goodwill impairment concerns flagged in annual filings tied to certain portfolios highlight ongoing profitability scrutiny within sub-brands [S1].

Growth Drivers and Expansion Opportunities

Looking forward, Flowers Foods focuses on several growth vectors anchored in both organic expansion and operational efficiency gains:

- Product Innovation: Launching differentiated bakery varieties that meet evolving consumer preferences such as clean-label ingredients or health-conscious formulations may drive incremental volume.[S2]

- Geographic Expansion: Extending footprint into underserved regions leveraging existing bakery infrastructure offers volume scale benefits.[S2]

- Supply Chain Optimization: Enhancing procurement analytics and manufacturing efficiencies can reduce unit costs while mitigating inflation impacts.[S3]

- Pricing Strategy: Balancing measured price increases against competitive pressures will be crucial; measured pricing power preserves margin without substantial volume loss.[N1]

- Capital Allocation Discipline: The recent dividend reduction frees cash flow towards deleveraging or selective investment supporting sustained growth.[S3]

Successful realization of these drivers depends heavily on management execution capability post-Chief Growth Officer departure. Continuity in innovation pipeline development represents both opportunity and risk considering increased leadership demands during financial restructuring phases.

Risks and Challenges Including Liquidity and Market Pressures

Several headwinds cloud Flowers Foods’ outlook:

- Liquidity Constraints: Current liabilities exceeding current assets signal tight working capital necessitating vigilant cash management to avoid operational hiccups or covenant breaches.[S2]

- Debt Refinancing Uncertainties: Although the term loan addresses near-term maturities, refinancing terms—interest rates or covenants—may pressure flexibility amid rising interest rate environments.[S3]

- Input Cost Volatility: Despite hedging programs, unexpected commodity price spikes remain a margin risk given thin pricing leeway.[S1]

- Leadership Transition Risk: Loss of chief growth executive complicates strategic continuity in product development critical for future competitiveness.[S2]

- Consumer Demand Sensitivity: As bread remains a staple with moderate substitute options, any adverse shift in consumption patterns due to economic slowdowns could dampen volume growth.[S1]

- Goodwill Impairment Threats: Underperforming acquired units present risk case if financial targets are missed.[S1]

Overall vigilance around these risks will be essential for stakeholders monitoring operational stability amidst evolving market conditions.

Key Near-Term Milestones and What to Watch Next

Investors should track these upcoming developments closely:

- Subsequent quarterly earnings releases post-April 2026 quarter will reveal whether revenue momentum sustains alongside profitability metrics reflecting cost management efficacy.[S2]

- Progress updates related to debt repayment schedules or covenant compliance disclosures will indicate capital structure health.[S3]

- Leadership succession plans or appointments replacing the Chief Growth Officer will signal continuity strength in strategy execution.[N1]

- Volume trends for core categories such as fresh bread lines will serve as barometers of consumer acceptance amidst inflationary backdrops.

- Further announcements on dividend policy adjustments post-refinancing may also provide insights into cash flow stability.[S3]

Monitoring these indicators will offer practical insights into the company’s trajectory as it balances growth aspirations with financial prudence.

This analysis synthesizes publicly available SEC filings and contemporaneous market news as of May 21, 2026. It aims to present a fact-based operating assessment without investment research views or forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments