Farmhouse Inc. Evolves Through Digital Asset Strategy and Licensing Momentum

Farmhouse Inc. leverages recent convertible note financing to support its pivot from legacy licensing toward a digital asset treasury initiative amid liquidity constraints.

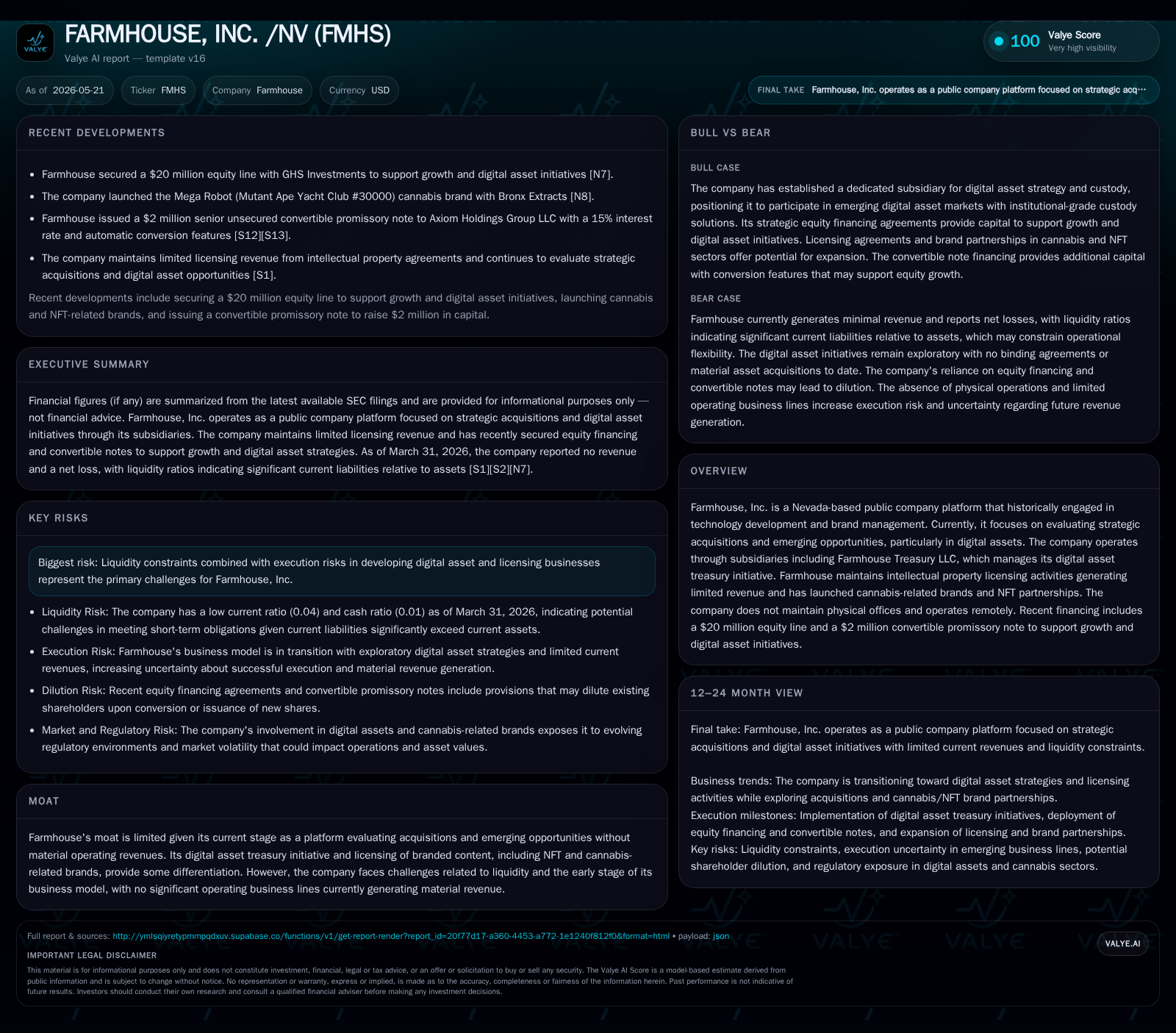

The latest 10-Q filing dated May 20, 2026, reveals Farmhouse Inc.'s strategic transition with a $2.2 million convertible promissory note issuance combining cash and digital asset consideration to advance its Digital Asset Treasury initiative. While the company maintains modest intellectual property licensing revenues, its core growth focus rests on deploying capital through Farmhouse Treasury LLC in an emerging digital asset market. The company faces significant liquidity challenges, reflected by a current ratio of 0.04 as of Q1 2026, underscoring execution risk in its nascent business model. Monitoring the pace of digital asset acquisition and conversion events related to the convertible note will be critical to assessing Farmhouse’s evolution.

Latest Quarter Operating Update: Financing and Strategic Initiatives

Farmhouse Inc.'s May 20, 2026 10-Q [S2] updates stakeholders on a critical financing event completed earlier that month: the issuance of a senior unsecured convertible promissory note (the "Note") with a principal amount of approximately $2.22 million. This issuance followed a Securities Purchase Agreement executed with Axiom Holdings Group LLC. Notably, the consideration comprised an equal split between $1 million in cash proceeds and $1 million in digital asset consideration [S3]. After adjusting for an earlier $100,000 advance payment in March 2026 and deducting legal expenses, net cash received was roughly $884,000.

This capital injection is targeted explicitly at supporting Farmhouse's Digital Asset Treasury (DAT) strategy under Farmhouse Treasury LLC ("FT"), which acts as the operational vehicle overseeing their anti-debasement digital asset framework involving Bitcoin and tokenized or physical gold [S1]. The Note carries a robust 15% annual interest rate but defers interest payments until conversion or maturity—scheduled roughly ten months post-issuance unless converted earlier. Conversion is mandatory upon specific triggers such as equity financing exceeding $5 million gross proceeds or sustained stock price increases suggesting valuation uplifts [S3].

With no material operating revenues reported during this quarter and FT’s initial formation investment being nil as of year-end 2025 [S1], this financing represents a foundational step enabling Farmhouse to transition from an IP licensing holdover toward active participation in digital asset markets.

Business Model Overview: Licensing Legacy and Digital Asset Platform

Farmhouse historically generated limited revenues through intellectual property licensing centered around branded content assets like social media handles and domain names ([S1], [S6]). Revenue recognition follows ASC 606 standards using sales-based royalties timing aligned with licensee sales events—notably generating just $623 in revenue for the fiscal year ending December 31, 2025 [F1]. These activities remain marginal relative to corporate overhead.

Strategically, Farmhouse now operates primarily as a platform evaluating acquisitions alongside nurturing its digital asset treasury initiative hosted under FT—a manager-managed subsidiary solely owned by the parent company [S1]. The DAT initiative embodies an anti-debasement framework seeking stable-value stores such as Bitcoin alongside tokenized gold assets.

The company forgoes traditional physical office footprints, engaging two full-time executives supported by contractors working remotely [S1].[F1] The business model hinges on capital deployment efficiency within digital assets combined with scalable acquisition prospects rather than legacy licensing revenues.

Revenue drivers are immature at this stage; margins are non-existent due to operating losses concentrated on development expenditures rather than commercial scale licensing or asset management fees.

Industry Structure and Competitive Context: Digital Asset and Licensing Markets

Within the nascent digital asset management space, smaller platforms like Farmhouse face steep competitive dynamics against established cryptocurrency investment firms, crypto-native fund managers, and diversified fintech entities offering treasury-like functions for corporations rebalancing cash holdings into alternative assets.

Licensing markets feature predictable yet limited revenue profiles due chiefly to niche branded content IP rights intersecting cannabis-related brands and NFTs—sectors with evolving regulatory regimes and speculative demand patterns. These elements constrain licensing upside but establish minimum cash inflows absent standalone operating lines.

No material peer-scale benchmarks are presented given Farmhouse's embryonic stage; however, barriers include regulatory compliance rigor for public companies managing digital assets and complexity around scalable acquisition integration.

Growth Drivers: Digital Treasury and Acquisition Pipeline

Farmhouse aims to cultivate growth by executing its Digital Asset Treasury initiative via FT. The foundational step is leveraging freshly raised capital (both fiat and digital assets) into portfolio allocations consistent with anti-debasement objectives prioritized around Bitcoin plus tokenized or physical gold holdings [S1], [S3]. This controlled deployment strategy mitigates volatility while positioning Farmhouse for broader participation as digital assets mature.

Concurrent discussions with cryptocurrency financiers point toward eventual partners or financing vehicles facilitating enhanced treasury management capabilities; however, these negotiations remain exploratory without binding commitments [S1]. Acquisitions targeting scalable business models outside legacy licensing further underpin growth aspirations but await formal announcement or closure.

Key performance indicators moving forward comprise milestones in acquiring qualifying digital assets for DT treasury accounts; progress in attracting counterparties to enhance treasury strategy execution; successful draws under the existing $20 million equity line agreement with GHS Investments potentially supplementing capital availability beyond convertible note funds; and measurable incremental improvements in IP licensing revenue if expansions materialize [S3], [S19].

Governance adherence through public company compliance standards embedded within the DAT structure presents an additional competitive edge by fostering transparency rare among early-stage crypto ventures.

Risks and Constraints: Liquidity, Execution, and Market Validation

Liquidity emerges as an acute constraint: Q1 2026 balance sheet snapshots reveal total current assets of approximately $95K offset by ballooning current liabilities near $2.45 million resulting in a punishing current ratio near 0.04—highlighting acute short-term funding stress [F1]. Cash on hand stood at roughly $32K against modest debt obligations just above $55K translating to net debt approximately $23K [F1].

This weak liquidity profile constrains operational flexibility amidst ambitions requiring upfront treasury asset purchases paired with acquisition costs.

Execution risk remains elevated given that none of the planned strategic partnerships or acquisitions have crystallized into definitive contracts despite ongoing dialogues [S1]. Digital asset markets exhibit significant volatility—including potential NFT or cannabis brand demand swings—exposing Farmhouse’s revenue streams to speculative fluctuations.

Additionally, the convertible note’s automatic conversion clauses introduce dilution risks tied to share price movements or equity raises that could unfavorably impact shareholder value absent proportional capital gains [S3], [S4].

Regulatory uncertainty surrounding both crypto-assets governance including custody provider approval statuses further complicates risk assessment.

Outlook and Key Milestones: Monitoring Progress and Capital Deployment

Close attention should focus on several pivotal developments:

- Announcements of successful digital asset procurement or treasury capital deployments evidencing progress from funding to value-creation stages;

- Updates on strategic acquisitions or binding partnership agreements expanding scalable operating businesses;

- Utilization metrics concerning draws under the substantial up-to-$20 million equity line agreement indicating access to supplemental financing;

- Status changes concerning BitGo’s national trust bank application affecting custody assurance credibility;

- Movements relative to convertible note conversion events triggered either by stock price performance thresholds or new equity financings impacting capitalization structure;

- Scaling of IP licensing arrangements beyond negligible revenue baselines signaling expansion feasibility.

These milestones form observable checkpoints for validating Farmhouse’s pivot success from conceptual platform toward operating entity engaging broader market opportunities.

Financial Profile: Balance Sheet Snapshot and Capital Structure

As per the latest filings ([F1], [S2]), Farmhouse retains about $32K in liquid cash equivalents at March quarter-end juxtaposed against total debt near $55K yielding net debt exposures around $23K. Operating income remains negative with no indication of approaching break-even thresholds given limited revenues ($623 recognized over FY25) versus consistent losses exceeding $400K annually preceding Q1 flows [F1].

The recent injection via convertible promissory notes totaling over $2 million represents crucial near-term capital but carries interest accruals payable only upon conversion or maturity alongside potential dilution effects encapsulated within conversion price ceilings [$0.15–0.50/share] bounded by VWAP discounts.[S3] This illustrates resource availability tradeoffs between debt leverage-induced risk versus growth funding essentiality.

It does not constitute investment advice but provides a factual basis for understanding strategic positioning within current known constraints.

Financial position in context

As of 2026-03-31, companyfacts shows $32329 in cash and equivalents and $55000 of total debt [F1]. The same snapshot implies net debt of roughly $22671, keeping balance-sheet context relevant but secondary to the operating story [F1]. Current assets of $95138 and current liabilities of $2mm imply a current ratio near 0.04x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments